FX Daily Strategy: N America, May 23rd

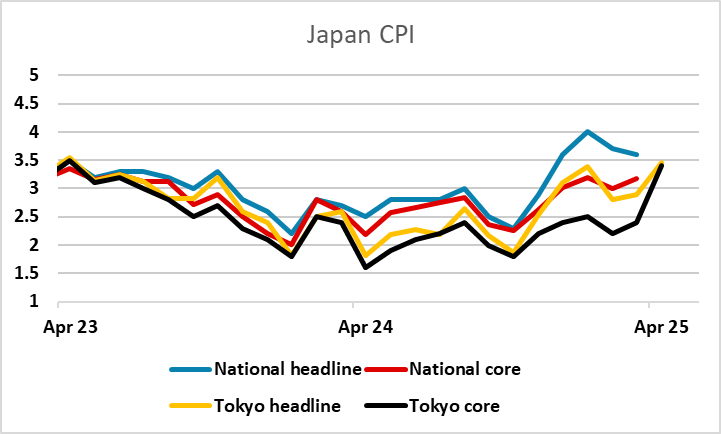

JPY to stay well supported by rising CPI

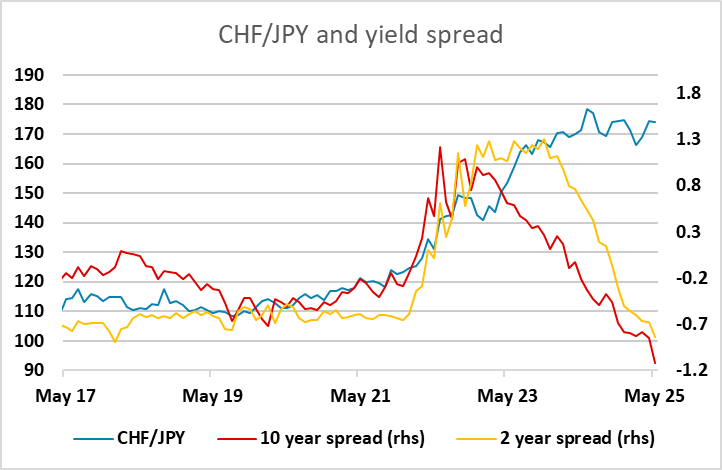

CHF/JPY remains the clearest value trade

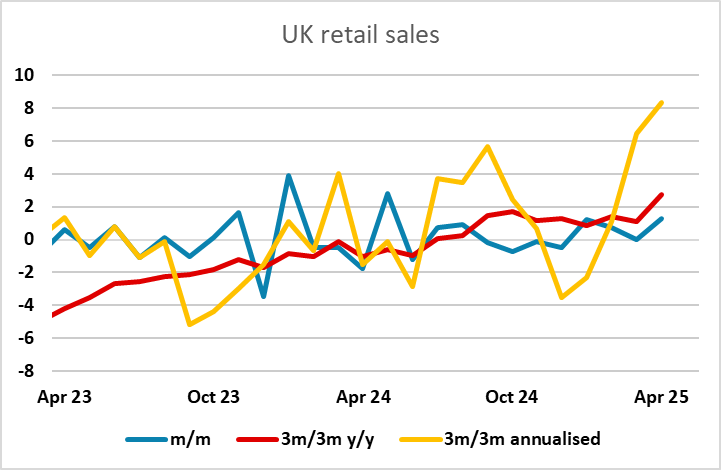

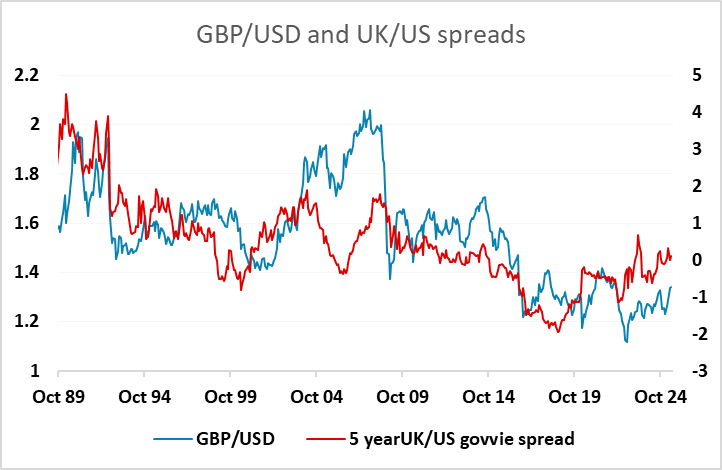

GBP may gain on retail sales but hard to see sustained break lower in EUR/GBP

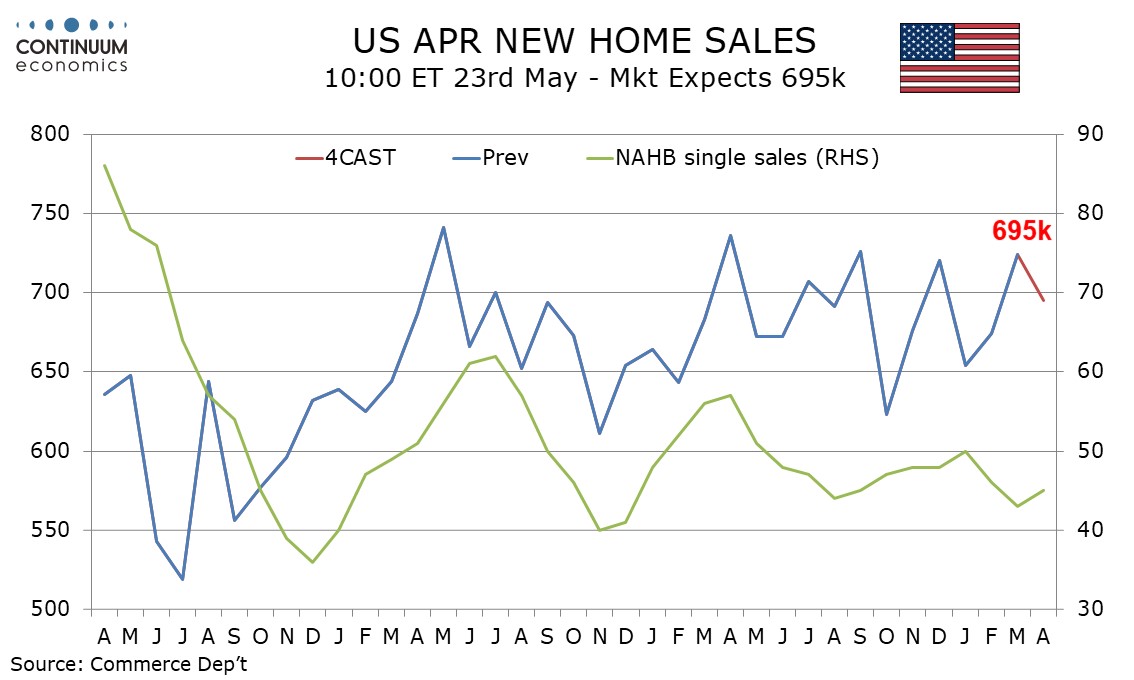

USD likely to be resilient on home sales data

JPY to stay well supported by rising CPI

CHF/JPY remains the clearest value trade

GBP may gain on retail sales but hard to see sustained break lower in EUR/GBP

USD likely to be resilient on home sales data

The Japan April National Headline CPI remains elevated at 3.6% y/y, ex fresh food at 3.5% y/y while ex fresh food % energy come in at 3% y/y. The BoJ is stuck now with rising inflationary pressure and U.S.-Japan trade complication, putting them in a difficult spot. It is likely the BoJ will not move until there is more clarity in the trade front.

As it stands, the market is only pricing 15bps of BoJ tightening this year, but this could rise quickly if the US or world economy shows post-tariff resilience. To some extent, this means the JPY is in a win/win situation. A weak US/global economy would undermine risk sentiment and tend to favour the JPY, but any strength in the global economy would likely trigger a BoJ rate hike, while other majors continue to cut rates. Japanese longer term yields have already risen substantially and the JPY looks attractive across the board, but from a yield spread perspective, CHF/JPY remains the clearest value play, especially since the CHF has similar risk characteristics to the JPY.

Europe kicked of with a set of significantly stronger than expected numbers. UK retail sales showed another sharp rise in April, and although March was revised down slightly, and the strength of April sales was seen as partly due to weather, the underlying trend seems to have improved significantly in recent months. Nevertheless, GBP is not much changed, with the market possibly seeing the weather effects as reducing the significance of the data.

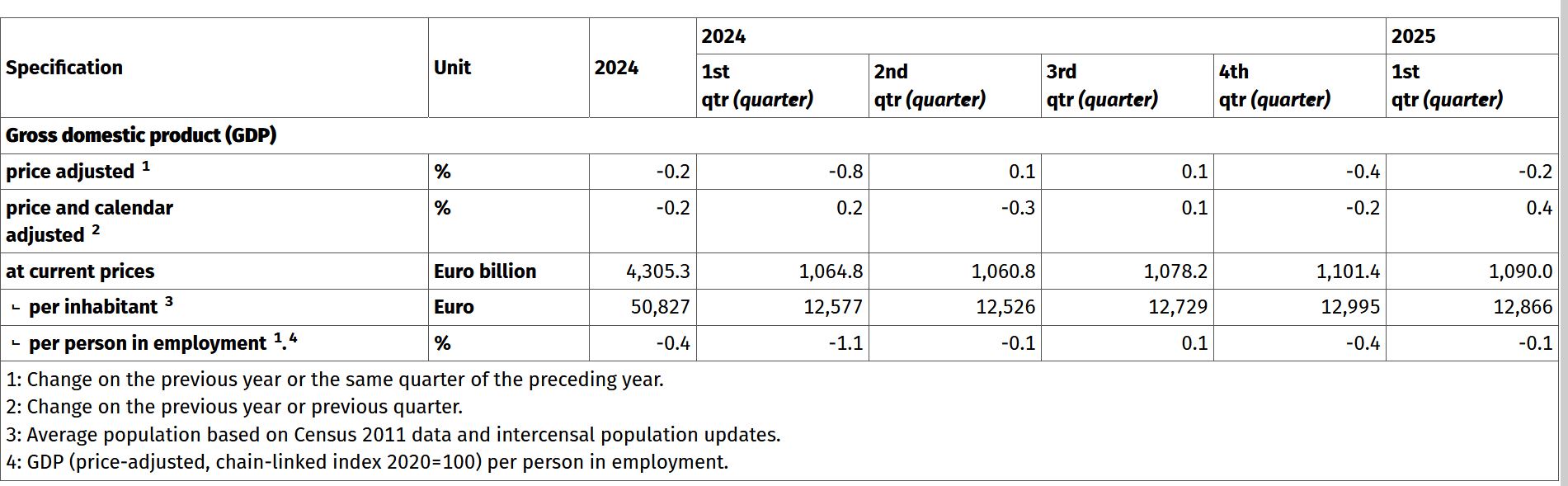

At the same time, we have had a surprising upward revision in the German GDP data to show a 0.4% q/q rise in Q1 from a previously reported 0.2%. This was due to surprisingly strong March data on manufacturing and exports. There is, however, a suspicion that this may relate to the US tariff introduction and the consequent rush to push exports into the US.

So there are caveats and uncertainties in both the UK retail sales and German GDP data, but despite this they should be supportive for European currencies and risk. There hasn’t been any significant initial reaction in FX markets, with EUR/USD and GBP/USD if anything dipping slightly, but the data should ensure there are buyers on the dip and we would favour the upside in both GBP/USD and EUR/USD today.

In the US, we expect an April new home sales level of 695k, which would be a 4.0% decline if March’s surprisingly strong 7.4% increase to 724k is unrevised. March’s level was near the tip of the recent range but underlying trend continues to have little direction, suggesting a dip in April is likely. Some housing sector surveys, such as the NAHB’s and MBA’s, showed modest improvements in April, but the NAHB index slipped in May and April existing home sales unexpectedly fell. We doubt the FX market will take a great deal of interest in these numbers, as the trend is choppy, but the housing sector will be important to watch in the coming months as the rise in longer term US yields could be damaging.