FX Daily Strategy: N America, March 6th

ECB to cut rates again

Limited scope for the ECB to provide much guidance given fiscal policy uncertainty

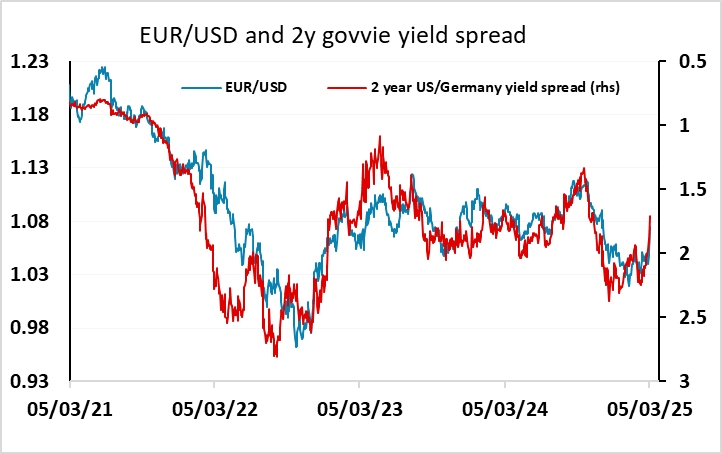

Risk may be towards a lower EUR after the sharp gains of recent days

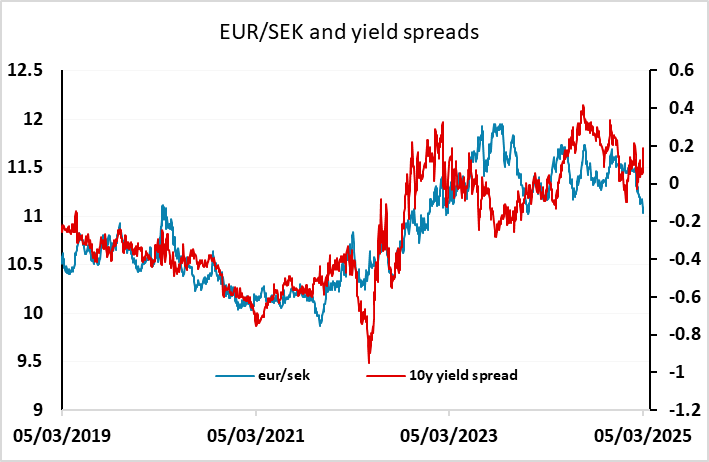

SEK strength bolstered by CPI data but is starting to look overdone

ECB to cut rates again

Limited scope for the ECB to provide much guidance given fiscal policy uncertainty

Risk may be towards a lower EUR after the sharp gains of recent days

SEK strength bolstered by CPI data but is starting to look overdone

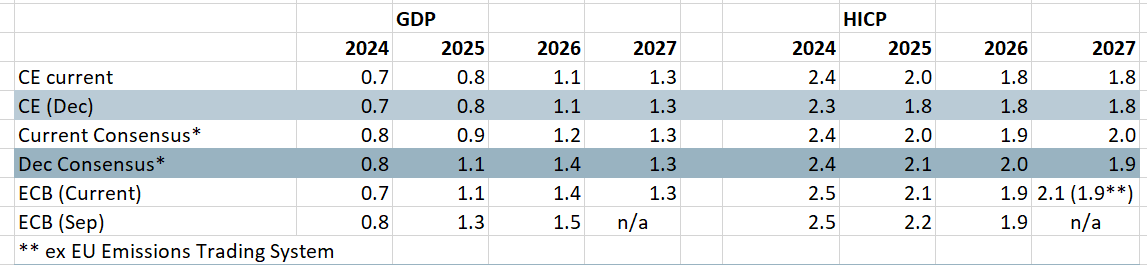

The ECB meeting will be the main focus on Thursday. As has been the case at most recent Council meetings, the ECB verdict is less important that the rhetoric. A sixth 25 bp discount rate is widely expected, to 2.5%, but how wide the door is left open for further cuts may depend on how near to neutral policy the Council feels they are. Last time around, the ECB stressed monetary policy remained restrictive albeit with differences on the degree and the debate on this issue may be more intense this time around. It is unclear also how vocal the Council wishes to advertise any shift as it may wish to keep options for further easing in April should US tariffs materialise as has been flagged.

ECB Likely to Remain Above Consensus?

Source: ECB, Bloomberg, CE

As for growth risks, little was made of the weaker real economy last time, and before the latest news of the likely boost to German defence and infrastructure spending, some downward revision to growth forecasts seemed likely. Now this is less clear, and even though the ECB won’t want to assume too much about spending decisions that are yet to be finalised, they will probably leave their growth assumptions alone for now. The likely reluctance of the ECB to commit to anything without a clearer read on the fiscal policy picture means it will be hard to draw too many conclusions from the decision.

As it stands, the market is pricing 69bps of easing by the end of the year, including 25bps at this meeting, and December is seen as the low point for the policy rate. The April meeting is currently priced as representing a 50-50 chance of a rate cut, but the next cut is fully priced in by June. The large moves higher in EUR yields in the last few days have not yet moves front end yields above the highs seen in November and January, and we doubt that he ECB will provide a reason to extend the gains given the uncertainties around policy, as well as the fragile current momentum of the economy. The risks may therefore be slightly to the downside for yields and the EUR, but we wouldn’t expect a sharp reaction, with the market’s perception of European fiscal policy still the dominant factor for now.

Swedish CPI

Source: Continuum Economics

EUR/SEK has extended its recent decline in early trade after the flash February CPI data came in stronger than expected at 0.9% m/m, 2.9% y/y for the targeted CPI measure. The data further reduces the chance of any more easing from the Riksbank, with the inflation numbers now clearly showing a pick up in recent months on a seasonally adjusted basis.

EUR/SEK has been declining steadily in then last couple of weeks, helped by a more positive take on the European economy and the stronger than expected 0.8% gain in Q4 Swedish GDP data that indicated that the Swedish economy is on an upward path. The SEK often benefits in periods of optimism about European growth, and is also favoured by hopes of a peace deal in Ukraine. But recent gains have exceeded the moves in yield spreads which it typically follows, and progress below 11 is likely to be more difficult.

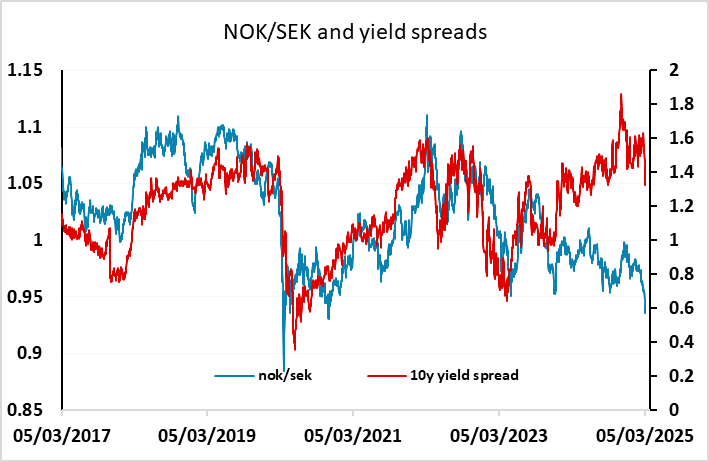

NOK/SEK continues to move lower and is testing the May 2020 low of 0.9260 which is the lowest level seen since the early 1990s excluding the immediate pandemic spike in March 2020. NOK/SEK disconnected from yield spread moves in 2024 and the NOK is now also suffering from worries about lower oil and gas prices. But it is nevertheless hard to see the case for such a low level in NOK/SEK, and longer term players will see current levels as a buying opportunity.