FX Daily Strategy: APAC, December 12th

UK GDP may recovery after September dip

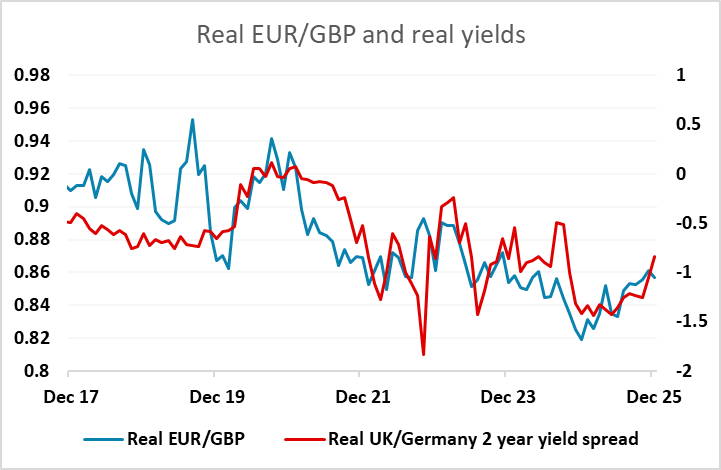

GBP downside favoured longer term, but little near term risk

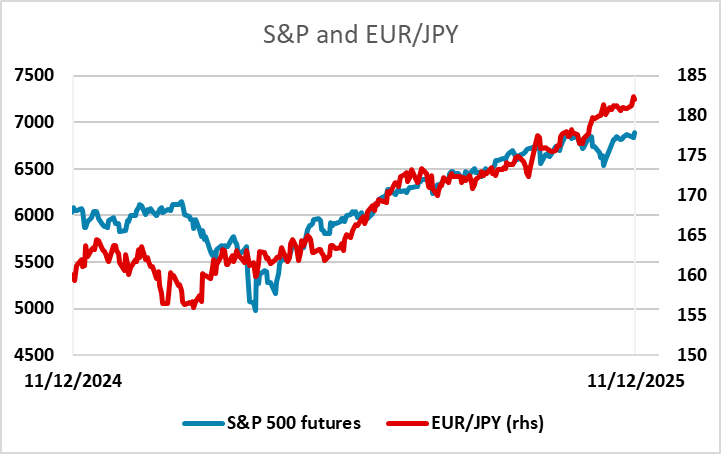

JPY could benefit from tech jitters

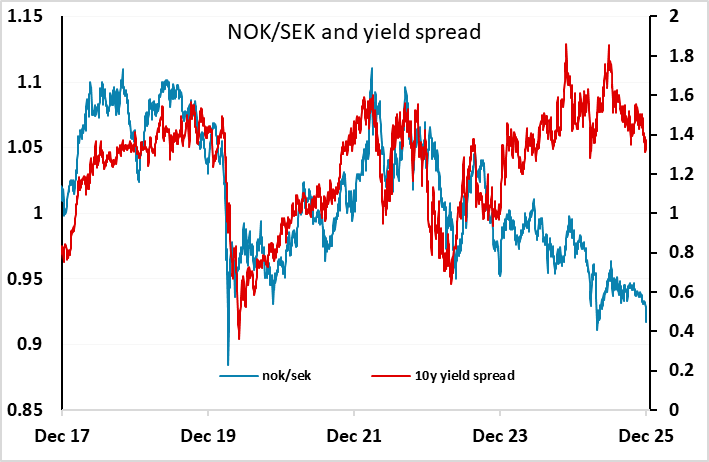

NOK/SEK dip towards year’s lows looks hard to extend

UK GDP may recovery after September dip

GBP downside favoured longer term, but little near term risk

JPY could benefit from tech jitters

NOK/SEK dip towards year’s lows looks hard to extend

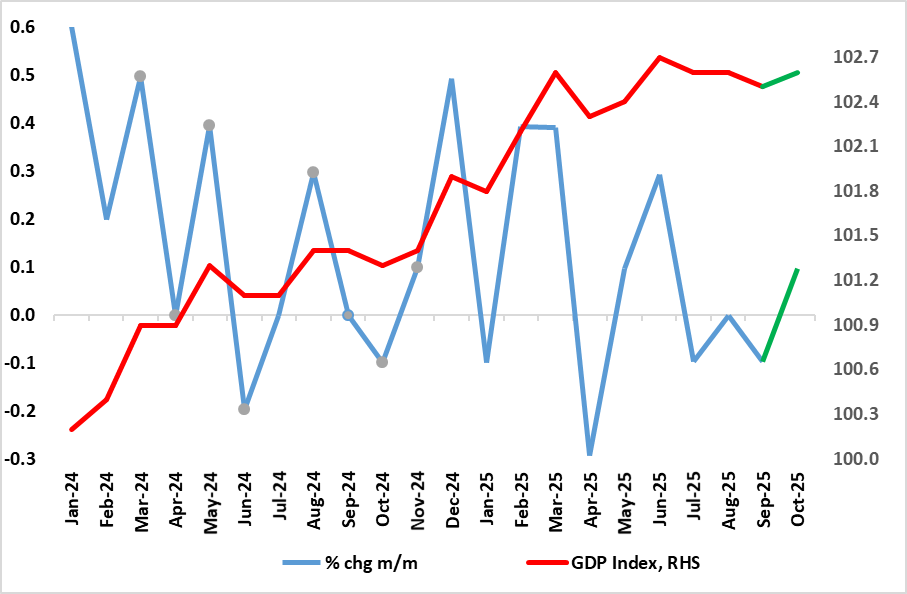

Solid UK GDP Growth Ebbing?

Source: ONS, CE

Friday sees UK October GDP. Some recovery should be in store for the current quarter as the September numbers were hit (temporarily) by the cyber-attack at JLR vehicle manufacturing and by weather swings. But amid less friendly weather patterns and what have already been weak retail sales numbers, as well as only a slow recovery on the vehicle side, we see only a 0.1% m/m rise for October. While it only has a small weight, construction output could be a negative after the construction PMI hit a record low (outside the pandemic) in October.

Our GDP forecast is in line with the consensus so there is unlikely to be much GBP reaction. EUR/GBP remains fairly steady in the mid-0.87s, and while we do expect to see a BoE rate cut next week, this is nearly fully priced in and isn’t likely to trigger a test of the year’s highs above 0.8860. While we do expect medium term GBP weakness as UK real yields gradually converge with the Eurozone, the convergence does look likely to be gradual, especially since the UK Budget proved much less contractionary than expected, and actually provides a mild net fiscal boost in the front year.

Otherwise, there isn’t a great deal on the calendar, but equity markets will be a focus with the US tech sector a little on the back foot after the Oracle dip this week on AI concerns after their latest earnings. If nerves continue this should favour the JPY on the crosses, with the JPY managing some modest gains on the crosses through Thursday after initially failing a test towards the all time EUR/JPY high of 1.8265 seen on Tuesday. There remains a lot of potential for JPY gains across the board if the equity correction is sharp.

The other notable move on Thursday was another decline in NOK/SEK towards the lows of the year. The rationale is unclear. Lower oil and gas prices may be a factor, but there is little in yield spreads to justify the move, and NOK weakness remains something of a mystery. However, if we do see any general risk sell-off, the NOK will tend to suffer due to low liquidity, so there are risks of a test of the year’s low. But other than the pandemic, 0.90 has been the historic low for NOK/SEK, so it’s hard to see the case for a break without something more fundamental occurring.