FX Weekly Strategy: March 10th-14th

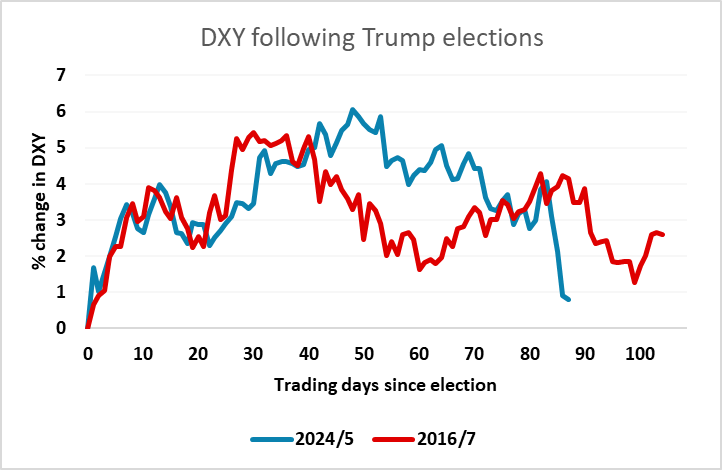

USD has reversed post-election gains

USD downside still favoured as tariff related concerns unlikely to disappear

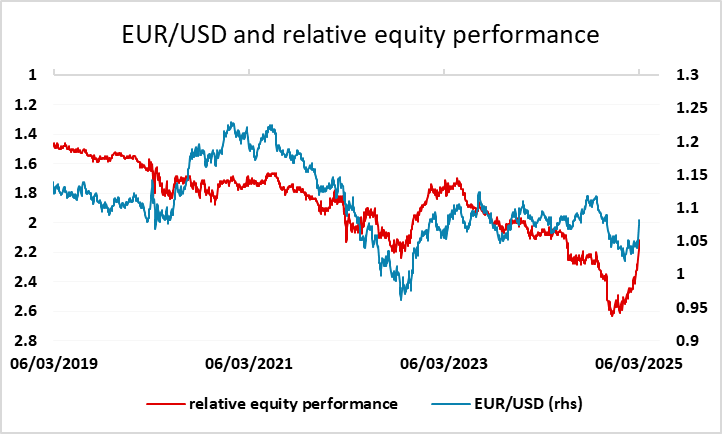

EUR upside more limited as equity gains may stall

JPY continues to look to have the most upside potential

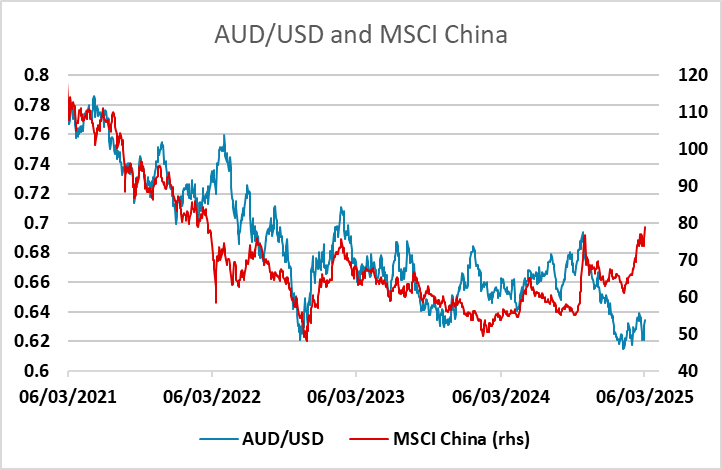

AUD can play some catch up

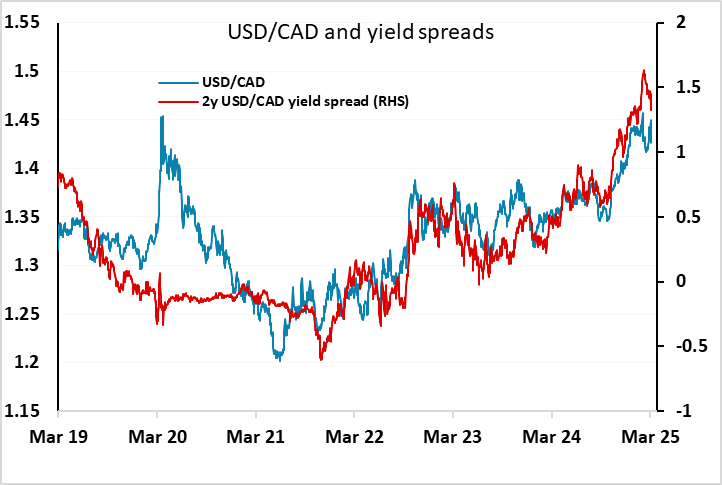

CAD may suffer from BoC rate cut

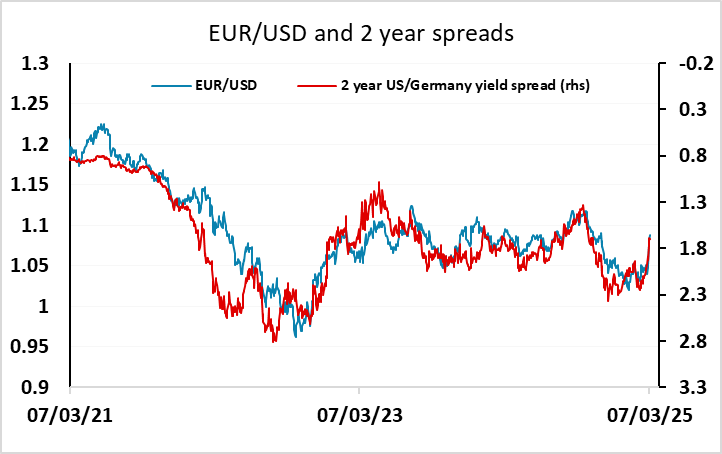

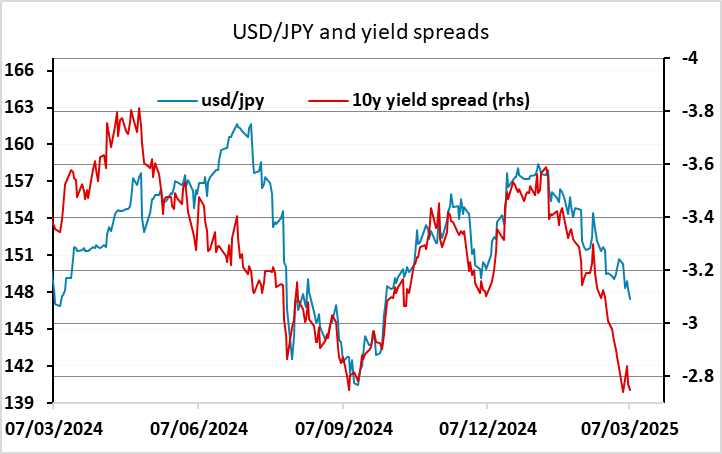

USD weakness has been then theme for the last week, and the USD is now essentially back to where it was before the US election. The expectation of significantly easier fiscal policy involving large tax cuts has all but disappeared as Congress looks unlikely to pass any major additional cuts, while tariff increases look like being significantly contractionary both directly via higher prices and the implied budget tightening and indirectly via the effect on confidence. At the same time, the EUR has benefited from expectations of increased fiscal spending – mainly from Germany - on defence and infrastructure, driving EUR yields higher, and Japanese yields have also continued to move up helped by some hawkish comments from the BoJ. Yield spreads fully support the move down in the USD that we have seen, and in the case of the JPY there is clear scope for further declines, even just looking at the most recent correlations with nominal yield spreads.

It is hard to see anything that happens this week turning negative USD sentiment around. Even if the US CPI data comes in on the high side of expectations, it is no longer clear that the Fed sees short term CPI strength as a reason for tightening if it is accompanied by weakening demand. The market expectation of higher prices due to tariffs hasn’t led to an increase in US rate expectations, but rather has tended to push US yields lower on the view that higher tariffs will lead to weaker real demand. While there have been a few pieces of softer data, USD weakness isn’t really based on the current data but on fears for the future, and to some extent on the preference of the Trump administration for a weaker USD.

So we would expect USD weakness to continue to extend in the coming week. The JPY still looks like the currency with the most potential for gains based on current yield spreads, but the JPY will only tend to outperform significantly if equity markets are looking fragile. The EUR outperformed in the last week because of the boost to European equity markets from the expected European government spending increases, but with European yields also rising, it is now unclear that there is a lot more upside for in European equities, at least until there is some more evidence of growth recovery. We would therefore tend to favour JPY strength on the crosses as well as against the USD, especially if this weeks labour cash earnings data shows any strength.

This far, the AUD has underperformed as the EUR and JPY have made gains against the USD, but it continues to look cheap relative to yield spreads and if equity markets remain steady, particularly in Asia, there is scope for the AUD to play catch up. The 0.64 area has proved to be strong resistance so far, but a break of this could open the upside for more substantial gains.

Event wise, other than US CPI, the BoC meeting is the main event. The market is pricing a 25bp rate cut as around a 75% chance, and the introduction of the 25% tariff suggests to us that the BoC are very likely to cut again, as they have waned that the tariff increases will lead to recession. While the retaliatory tariff increases form Canada will tend to push up Canadian inflation, the BoC are likely to look through this to the demand issues created by the US tariff increases. The CAD has so far proved very resilient in spite of the tariffs, but a rate cut this week could see USD/CAD move back above 1.44.

Data and events for the week ahead

USA

US data focus will be on inflation, with February CPI due on Wednesday and February PPI on Thursday. We expect both to see gains of 0.3% overall and 0.3% ex food and energy, consistent with inflationary pressures remaining above the Fed’s target. Other data that will be closely watched for signs of weakness are February’s NFIB small business survey on Tuesday and initial claims on Thursday. Friday sees the preliminary March Michigan CSI, where inflation expectations will attract the most attention. Fed speakers will be quiet ahead of the March 19 meeting.

Canada

The Bank of Canada meets on Wednesday and despite recent Canadian data having showed signs of regaining momentum in response to BoC easing, we believe the threat posed by US tariffs will justify a further easing, by 25bps to 2.75%. January building permits are due on Thursday. Friday sees January manufacturing and wholesale sales, for which preliminary estimates are for gains of 2.0% and 1.8% respectively.

UK

More BoE insight may come after the Bank publishes its regular inflation attitudes survey on Friday. But economic weakness must remain an issue for the MPC given survey weaknesses, albeit something that GDP data may fail to highlight (Fri). After upside surprises in December, the odds are increasing that current quarter GDP will be decidedly positive as opposed to the weak(ish) picture we perceive. Regardless, and despite a clear bounce in retail sales for the month we think, that corrections in other parts of services and continued weakness in industry will cause a small m/m drop in January of around 0.1% m/m. But upside risks stem not just from the sales data, but also cold weather boosting already below-par utility output RICS housing survey data may add to that weak picture, echoing the sharp fall seen in construction PMI data of late.

Eurozone

A middling weak with a few second-order ECB comments and the latest central bank watchers’ conference (Wed) where a host of Council members will appear. There is January German industrial production (Mon) which may show a small recovery but possibly not enough for the EZ counterpart having have an even softer undertone (Thu).

Rest of Western Europe

There are a few key events in Sweden, but Monday sees the monthly industrial production and orders data and monthly GDP indicator, the question being whether the latter’s much more solid tone of ate persists or not. Details to the second successive CPI upside surprise appear Thursday. Norway has high-profile CPI numbers (Mon). For Norway, we see CPI-ATE y/y staying at 2.8%, this being a notch above the Norges Bank’s forecast.

Japan

Labor cash earning on Monday will be more eye catching than GDP on Tuesday as it will be a critical factor on when we see another BoJ hike. We do not expect the huge jump of 4.8% in Dec 2024 to be repeated but wages are likely to grow around the 3% ballpark. If there is another big beat, we could likely see a hike right after the spring wage negotiation. Q4 GDP On Tuesday will likely remain soft but stay in the growth territory.

Australia

Business Confidence, Consumer Confidence on Tuesday but Consumer Inflation expectations would be more important relatively, though neither will be market moving.

NZ

PMIs on Friday and some tier 2/3 data scattered throughout the week.