FX Daily Strategy: N America, February 13th

Some USD downside risks on US CPI…

…although the outlook is complicated by continuing US equity market strength

GBP firmer after labour market data

Some USD downside risks on US CPI…

…although the outlook is complicated by continuing US equity market strength

GBP firmer after labour market data

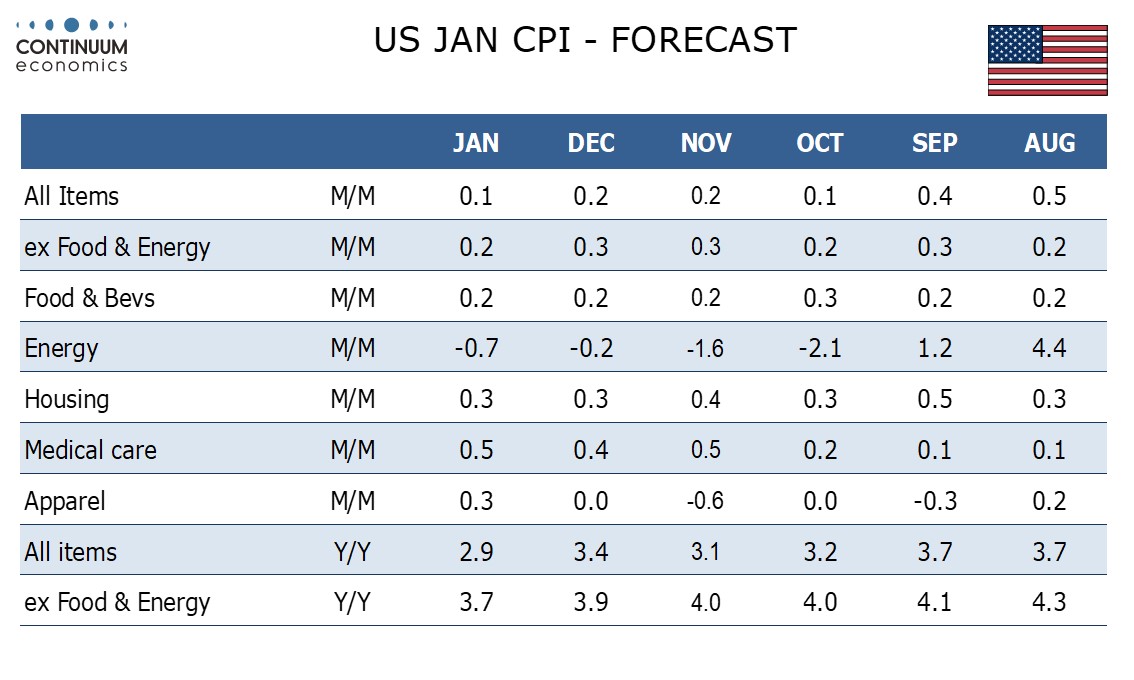

US CPI will be the main focus on Tuesday after what has been a very quiet period for data in the last week or so. We expect January CPI to increase by 0.1% overall and 0.2% ex food and energy, with our forecasts before rounding being 0.13% overall and 0.23% ex food and energy. Still, the ex food and energy rate would then be slower than the 0.3% gains seen in November and December ,and below the market consensus of 0.2% and 0.3% respectively. The risks should therefore be on the downside for US yields and the USD.

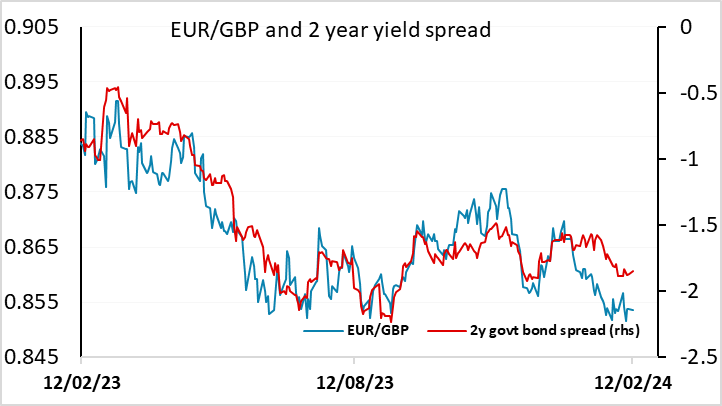

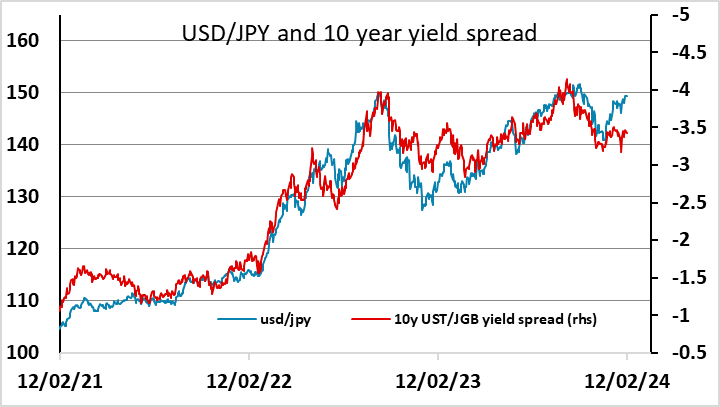

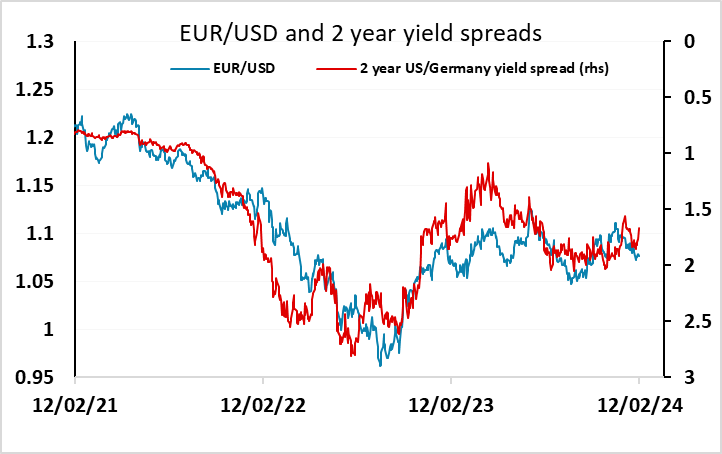

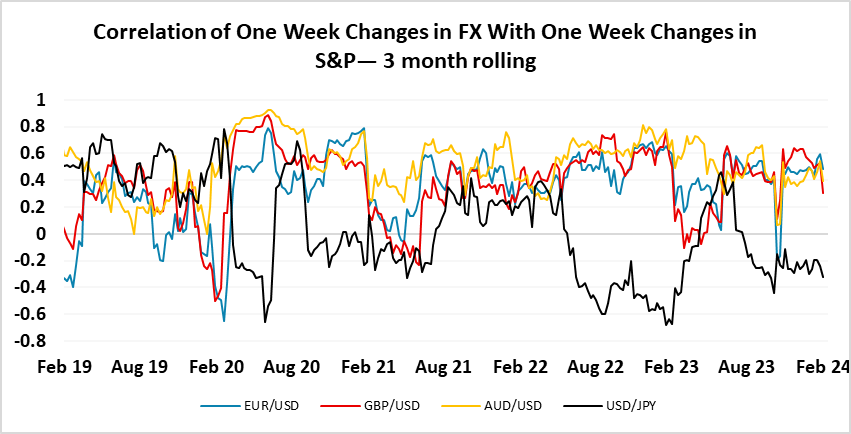

However, while the last few years have seen the FX market being dominated by movements in yield spreads, the correlation with yield spreads has faded at the beginning of this year in many currency pairs. It’s most notable in USD/JPY, which has remained well bid despite only very modest gains in US yields over Japan so far this year. However, it’s also the case that EUR/USD failed to gain on Monday despite a narrowing one the 2 year Germany spread with the US, which has been a reasonable guide to EUR/USD in the last few years.

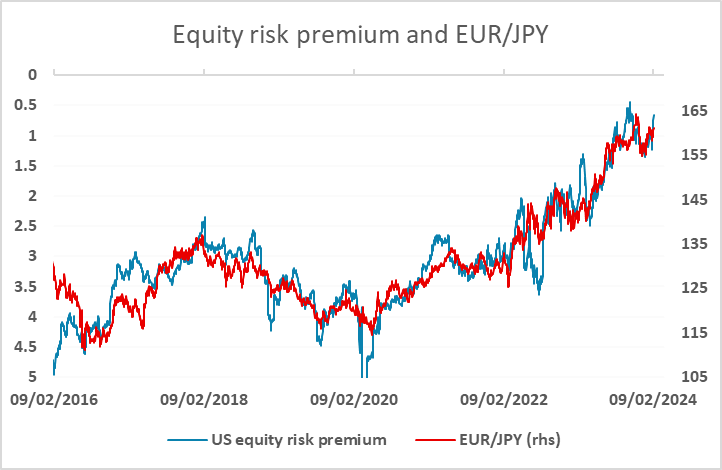

A lot of this disconnect looks to be related to equity market performance, particularly the strength of the US equity market. There is a strong historic correlation with JPY weakness and declines in equity risk premia, and the JPY has fallen back on the crosses as equity strength against a background of steady yields has led to lower risk premia this year. However, the USD has historically tended to be negatively correlated to equity market strength against the riskier currencies, and even against the JPY. This has continued in broad terms, but the USD has also tended to benefit from US equity market outperformance.

This makes the implications of the US CPI data harder to assess for the FX market. If there is a weak number that has a positive impact on US equities, both absolutely and relatively, it may moderate any negative yield spread implications for the USD, but would tend to be more favourable for the riskier currencies if equities were positively impacted by the data. Nevertheless, we do see some USD downside risks on the data as it is too early to conclude that the market is prepared to ignore US yield spread moves.

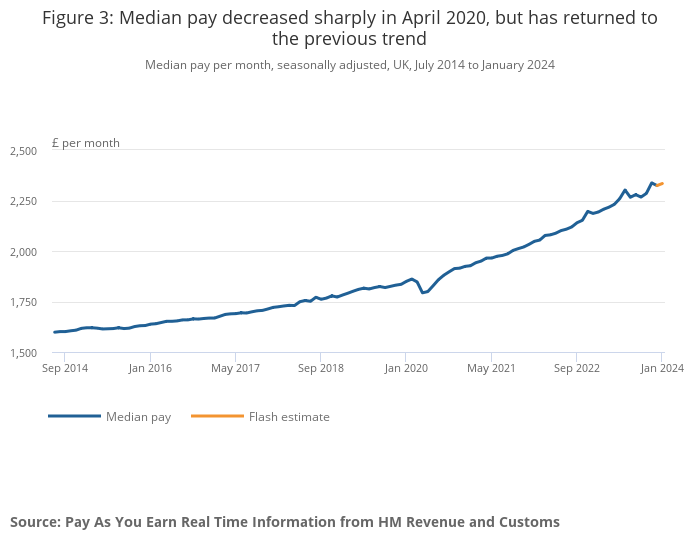

UK labour market data was on the strong side of expectations, with earnings on the high side of expectations at 6.2% y/y ex-bonuses and 5.8% y/y including bonuses, and the unemployment rate falling sharply to 3.8%. The decline in the unemployment rate is due in part to the decline in economic activity, but employment also rose, albeit in line with market expectations at 72k in the 3 months to December. However, the more up to data HMRC data was also on the strong side, with payrolled employment up 48k in January and revised to a gain of 31k in December after initially being reported as having declined by 24k. Earnings growth on the HMRC measure was also up slightly in January to 6.4% y/y from 6.3% in December. Having said this, the level of median monthly pay, while up slightly from December is essentially unchanged from November, so appears to be stabilising in the last few months.

All in all, the data is consistent with a stabilisation in earnings and employment, but isn’t showing significant weakness at this stage. The level of earnings growth will still be seen as too high by the hawks on the MPC, although the strength of the y/y measure conceals stabilisation in recent months. There is nothing in the numbers to indicate any urgency for a rate cut, and there shouldn’t be any significant impact on expectations of BoE policy.

GBP has initially reacted slightly positively as the data was modestly above market consensus, with EUR/GBP around 15 pips lower. But we don’t see much scope for a widening of yield spreads in GBP’s favour, and with EUR/GBP already trading below the level suggested by current yield spreads, we would expect support at the 0.85 level to hold near term, though a mild downside bias is likely to endure.