FX Daily Strategy: APAC, May 14th

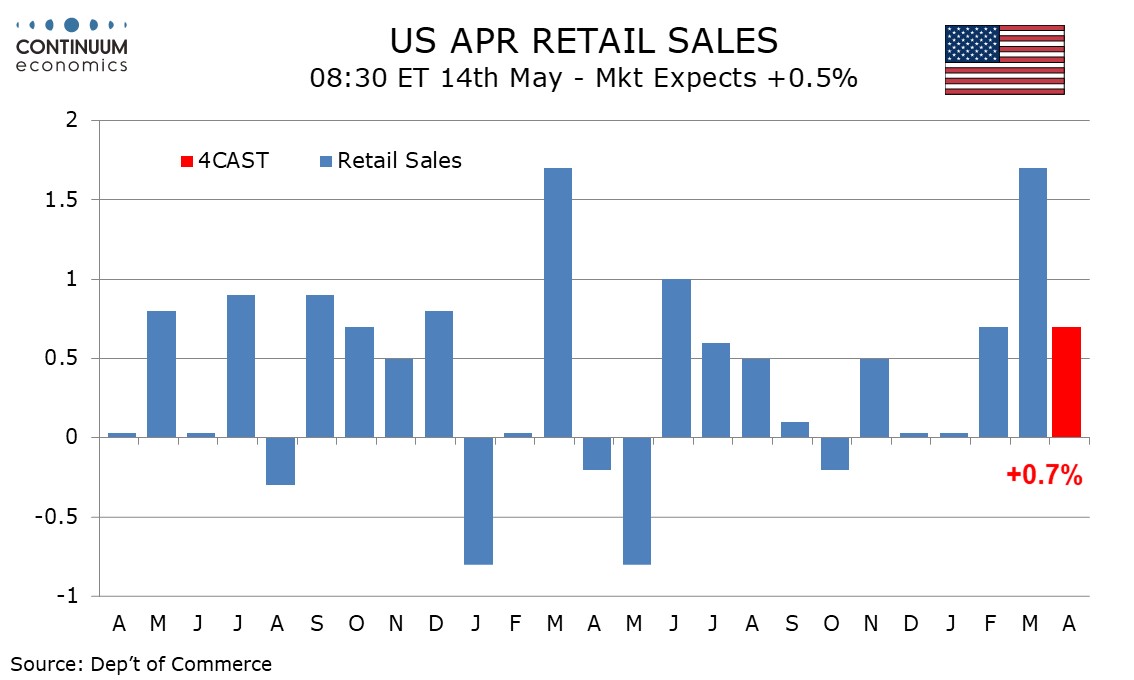

US retail sales to underscore comparative US resilience

Dollar juggles macro divergence meets reaction function divergence?

UK waits to see if PM challenge unfolds and how the machinations play out for likely winner

One of the pervading themes at present is a market that can’t quite decide what driver to grab onto: an unrelenting AI cycle as a source of US outperformance, or conversely a source of ongoing risk-on and build-out commodity cycle upswing and dollar weakness; the very same vertical moves amid an unresolved supply crisis as a source of imminent complacency, risk shakeout and so dollar safety bid; a relative impact story of US K-shaped economy resilient against European weakness as a source of inconvenient dollar bid; or a narrative of relative central bank reaction functions and potential political capture as a source of divergent near-term rate impacts, regardless of the macro trends.

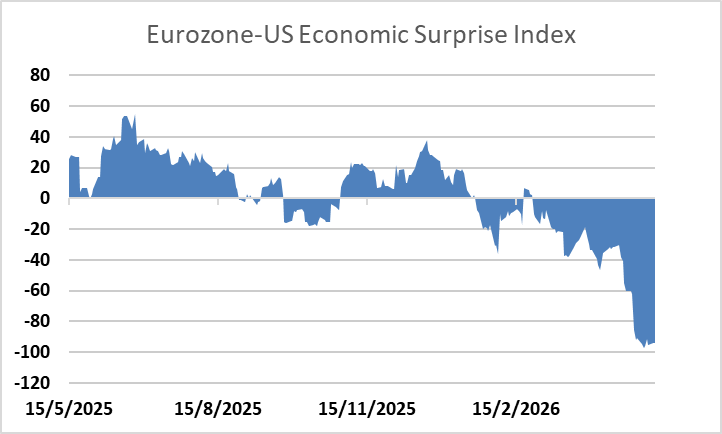

That’s perhaps no better illustrated that in the recent economic surprise trends where the extent of Eurozone relative deterioration seen to date compared to the US is all too apparent. That would, in other times, be driving the euro weaker versus the dollar and against consensus.

We could still see that play out in due course (see Eurozone: In Dire Straits? ) leading to some relative central bank repricing down the track. Central bank news flow could keep that scenario more speculative than concrete for now though. The message out the ECB is, as Bundesbank’s Nagel commented Wednesday, ‘no one enjoys raising interest rates when growth is under severe strain’, but ‘hikes are increasingly likely if inflation expectations remain elevated’ and if the Iran crisis is not resolved by next month. Lagarde and Lane are due to speak this week and will be watched for further comments on hike risks.

The next test of this comparative divergence comes with US retail sales data. We expect April retail sales to increase by 0.7% overall with a rise of 0.9% ex autos, albeit only 0.5% ex autos and gasoline, the latter a marginal slowing from two straight 0.6% increases. Tax cuts and higher tax refunds are providing some support to consumers and keeping the consumer resilient to headwinds.

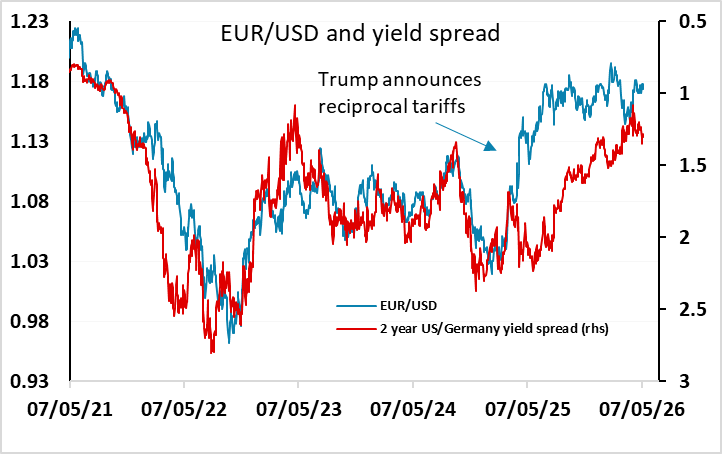

Looking at the European price action, both EUR/USD (1.17-) and cable (1.35) have been toying but not giving up on the immediate support areas that might signal more of a dollar bounce.

The UK has its own unfolding story of course, with attention today on whether Streeting follows through on the media reports that he could be on the verge of resigning as soon as Thursday and setting off a leadership challenge. We’ve discussed the machinations elsewhere but this remains quite a three-dimensional scenario for the market: the sooner the challenge, the more likely that either the challenge fails or Starmer is replaced by another centrist (Ed Miliband has emerged as the probably left candidate in this scenario and he would be a strange choice given his lack of voter appeal); the further out it is the more time for Burnham to engineer coming into contention. More broadly though, the market does need some perspective on just how market-negative policies under Burnham would truly be, and how undesirable that scenario really is if his greater popularity did see off a populist Reform challenge further down the road. Those determined to short the pound on this basis also need to think seriously about against what (all is far from rosy in France for example). Which is one of the reasons why, for all the recent building speculative build-up, GBP/AUD is testing the Dec23 lows and working its way down in the 10-year range.

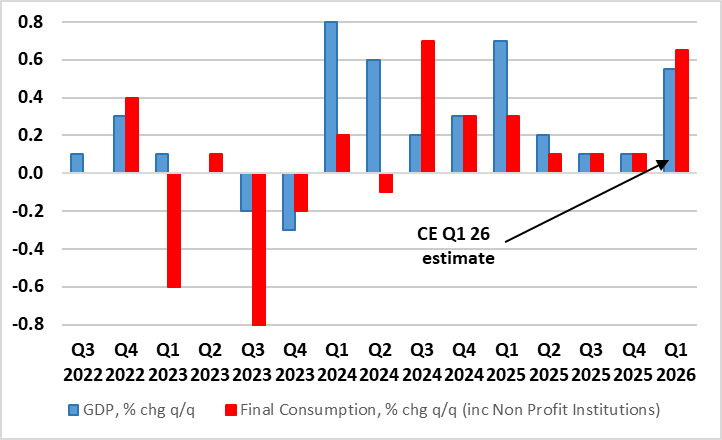

On the data front, the UK does sees March GDP which sets the backdrop to the current uncertainty. We see a correction of around -0.2% to -0.3%, which would leave Q1 up by 0.5%-0.6% q/q, but then likely giving way to a flat Q2 or a fresh dip.

As well as the ongoing Iran situation, the other event risk is the ongoing US-China meet, with the Thursday-Friday Beijing Summit. On the agenda is on delivering some agreements around some import agreements, extending the precious earths agreement, and pushing US tech interest, but as ever any Trump setpiece event provides ample opportunity for unexpected comments.