FX Daily Strategy: Asia, March 20th

Some downside risks for GBP on BoE meeting

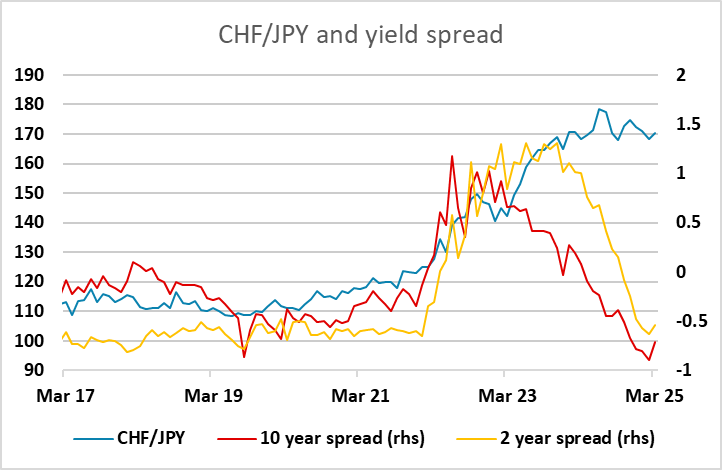

CHF/JPY could slip lower on SNB cut

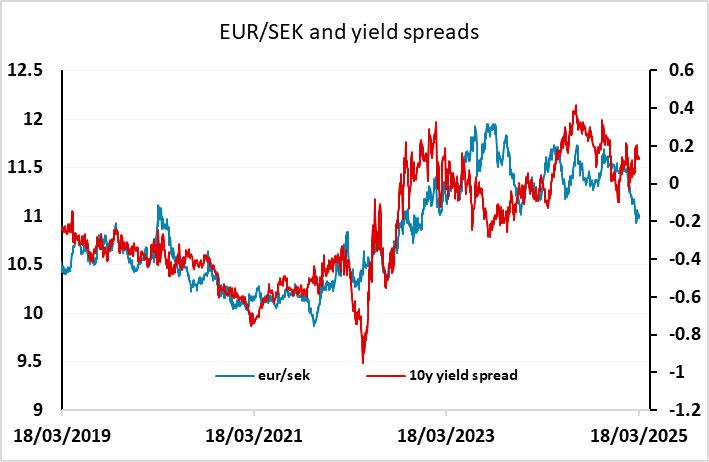

SEK likely unmoved by Riksbank but some weakness could be seen versus EUR and NOK

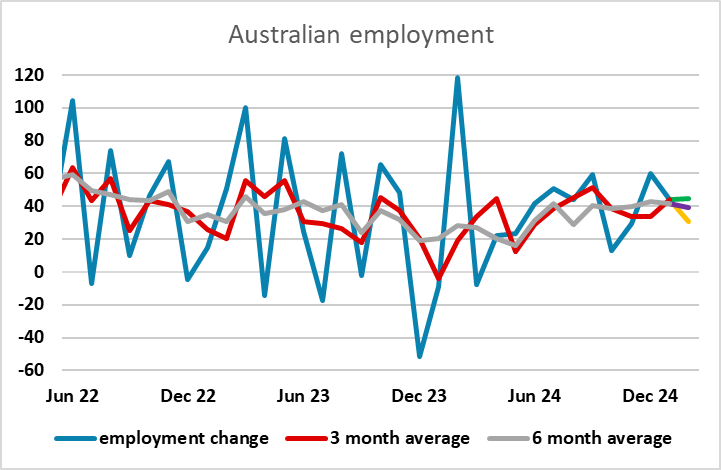

AUD more driven by regional risk sentiment than domestic employment data

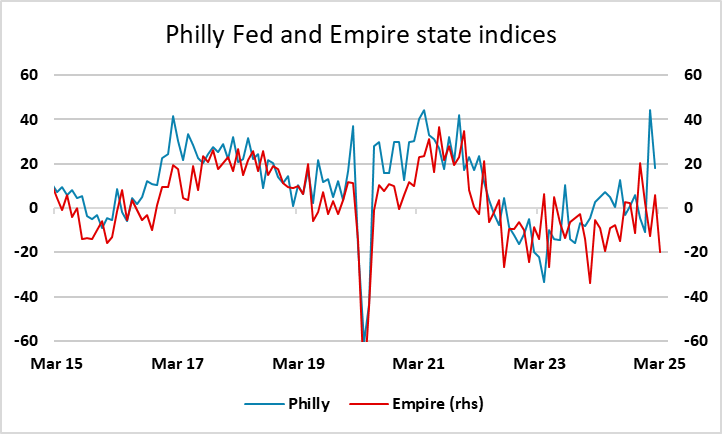

Philly Fed could hurt the USD if it echoes Empire manufacturing weakness

Some downside risks for GBP on BoE meeting

CHF/JPY could slip lower on SNB cut

SEK likely unmoved by Riksbank but some weakness could be seen versus EUR and NOK

AUD more driven by regional risk sentiment than domestic employment data

Philly Fed could hurt the USD if it echoes Empire manufacturing weakness

Thursday sees monetary policy decisions from the Bank of England, SNB and the Riksbank, as well as UK and Australian labour market data and the Philly Fed survey and jobless claims data in the US.

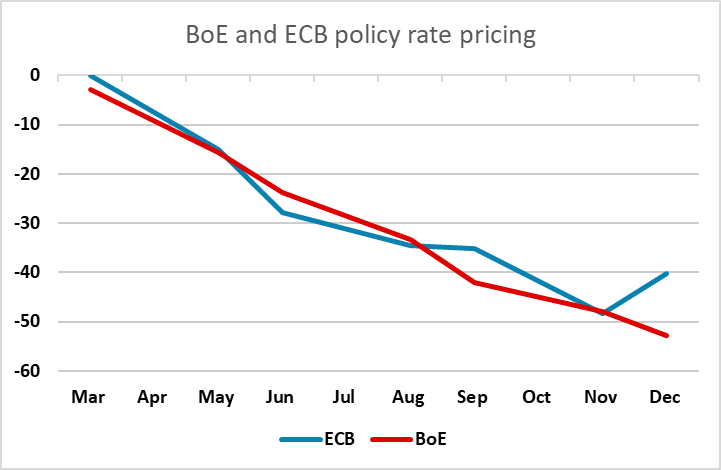

We expect stable UK policy (Bank Rate still at 4.5%) at the March meeting, and there is no significant risk of a move priced into the market. The MPC majority envisages rate cuts not faster than every quarter this year and a little further into 2026. But given what we think is a failing real economy backdrop, which growing global trade tensions may only accentuate, BoE easing may yet come faster and further as the BoE reassesses its optimism about growth and upgrades its estimate of the extent of slack – particularly in the labor market. The latest UK labour market data is due ahead of the decision, and while it may not affect the immediate vote, it could influence the tone of the statement. We expect to see more weakness in employment but the market will be focused mostly on the average earnings data, which may show some small softening but still looks too high to justify significant cuts.

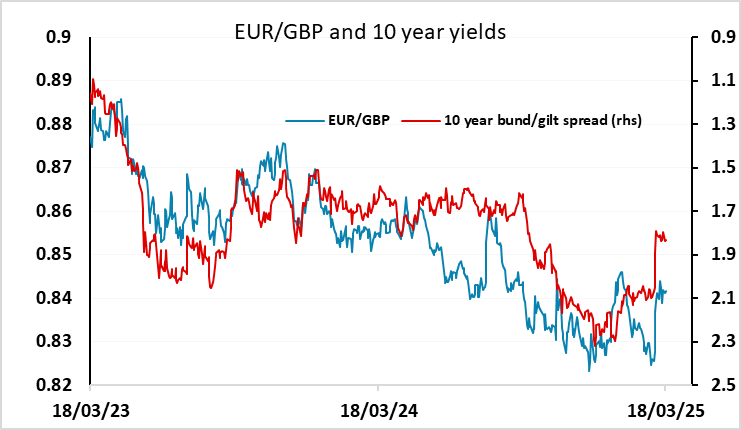

As it stands, the market is only pricing in a further 50bps of easing this year, thus missing out one quarter of cuts. While there are some concerns about higher short term inflation, this is being driven by administered energy prices and we still see core inflation weakening. The BoE will probably not be particularly forthcoming about future policy at this meeting, hampered as others are by the uncertainty surrounding US policy. But risks for UK yields look to be to the downside given the current modest easing priced into the market, and risks for EUR/GBP should consequently be on the upside.

The market is pricing around a 75% chance of a 25bp cut from the SNB, and we also see a cut as highly probable. This suggests a knee jerk modest negative CHF reaction to the announcement, but with a cut mostly expected the reaction is unlikely to be large, especially since the CHF is not particularly interest rate sensitive. However, a cut would take the Swiss policy rate below the Japanese policy rate for the first time since August 2022. In general, EUR/CHF tends to move with risk perceptions more than rate spreads, so a rate cut won’t change a great deal on that front. But CHF/JPY is less risk sensitive, with both currencies being seen as safe havens. It already looks far too high based on yield spreads as all spreads beyond the very front end now favour the JPY. A policy rate cut from the SNB would complete the set and further challenge the case for the current high level of CHF/JPY.

No action is expected from the Riksbank, and it would be surprising if there was anything to change the very neutral policy outlook currently in the market. We see some scope for the SEK to soften against both the EUR and the NOK as recent euphoria about increased European growth prospects and a Ukraine peace deal fade.

The Australian employment report is also unlikely to move the market significantly. The picture has been quite stable in recent months, and the AUD is being driven more by regional equity market sentiment than domestic data developments. On the US data, there is some downside risks for the USD if the Philly Fed echoes the recent weakness of the Empire manufacturing survey, particularly if the initial claims data shows any rise.