FX Weekly Strategy: March 17th-21st

SNB likely to be the only central bank to move rates this week

Some upside risks to the USD form the Fed…

…but downside risks to GBP from the BOE

BoJ to wait for more evidence on wages

USD should hold its own unless there is clearer evidence of growth weakness

There are four central bank interest rate decisions this week, with the Fed, the BoE, the BoJ and the SNB all meeting. The first three are all very unlikely to act, with unchanged policy seen as better than a 90% chance for all three. Nevertheless, guidance will as usual be important.

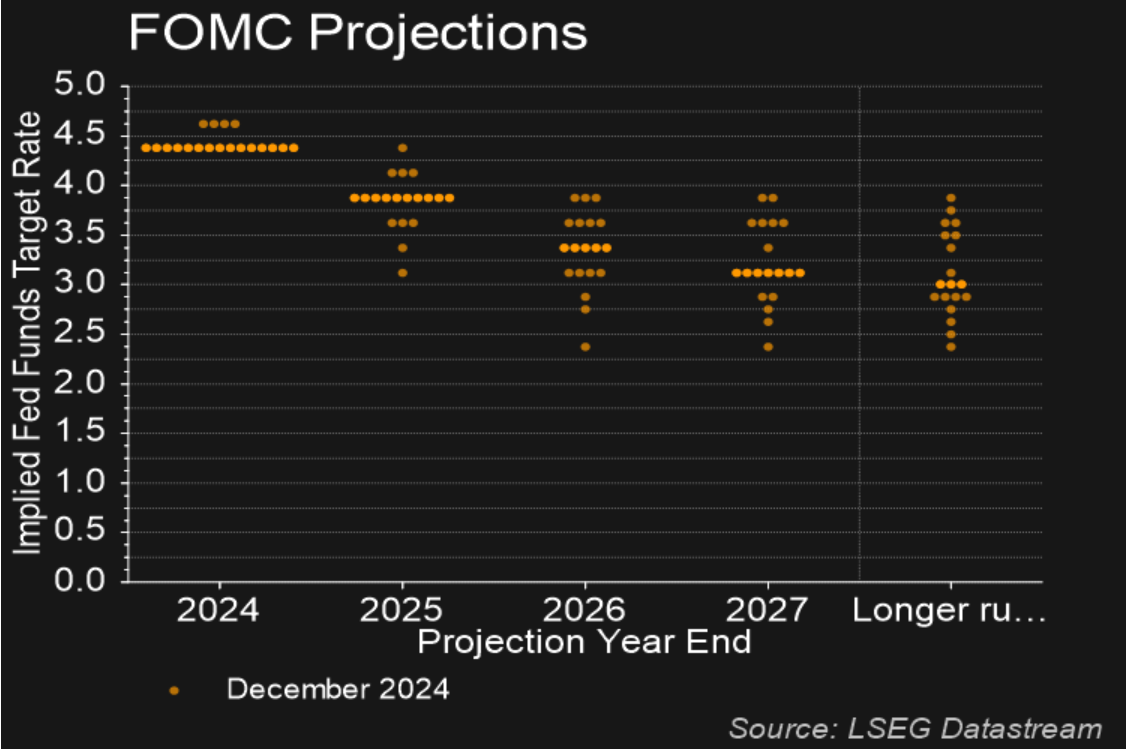

Fed dot plot from December

For the Fed, the focus will be on the new set of dots, but we don’t anticipate much change from January, as there is still huge uncertainty about Trump’s tariff policies. There is, however, certainly rising concern that tariffs will trigger a renewed rise in inflation, but one that will not be accompanied by rising incomes and consequently will slow real growth. The Fed reaction to this is unclear at this stage, but Powell’s recent comments don’t suggest they are likely to drastically change course. Even so, the risks may be that some of the more hawkish members show increased concern about the inflationary threat. Since there are a further three rate cuts priced into the market for the next year, and only two more were indicated by the January dots, the risks may be towards a higher short term rate profile. But it isn’t clear that this will be particularly USD supportive if it is seen as underlining growth and the equity market. Nevertheless, for now the risks look to be slightly on the USD upside form the FOMC.

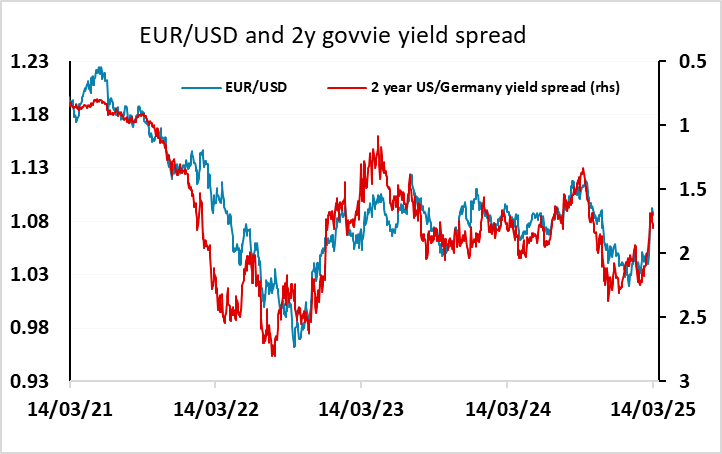

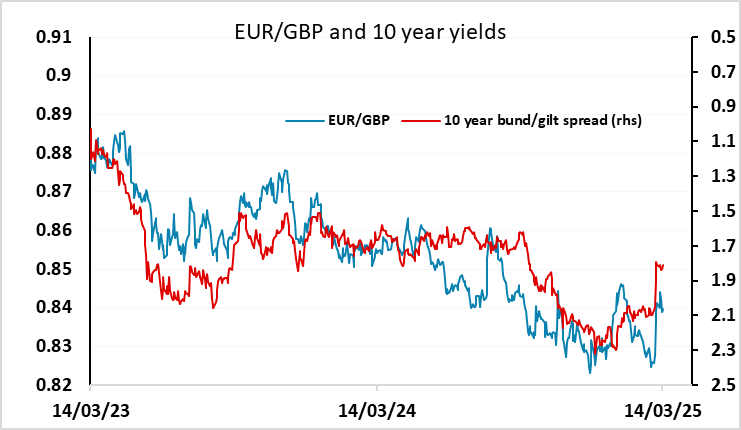

The BoE MPC are also not expected to cut rates, and are also unlikely to significantly change the guidance from February. But with only two more rate cuts priced in for this year, the risks may be towards lower UK front end rates, and the Bank may suggest a rate cut per quarter. GBP could therefore be at risk against both the EUR and the USD, with expectations of ECB easing having been scaled back since the announcement of new defence and infrastructure spending from Germany.

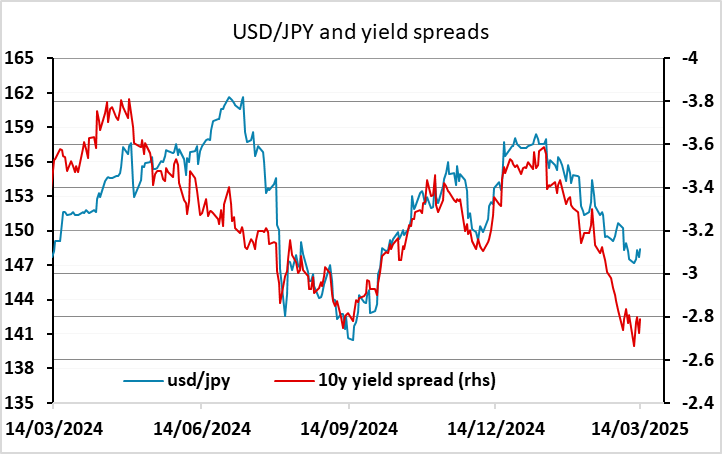

The BoJ are also unlikely to act this week, as they will still want to see the results of the spring wage negotiations. However, the latest reports suggests that there will be wage increases of 5%+, exceeding even last year’s, and if so this should secure a BoJ rate cut at the next meeting in May. Of course, the BoJ under Ueda has had a reputation for surprising the market, so a hike this time isn’t impossible, but the recent comments from Finance Minister Kato, suggesting that the recent JPY rise has been too one-sided, may encourage the BoJ to wait until May. But we would still expect hawkish comments from Ueda, and with only 4bps of tightening priced in for the May meeting, JPY risks should be on the upside.

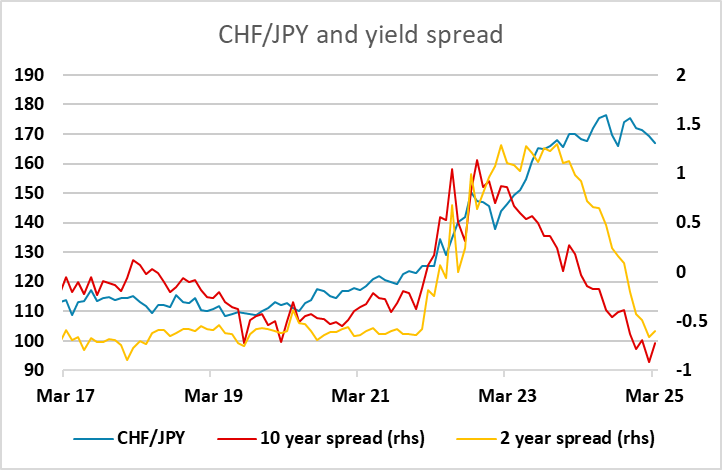

The SNB are the only one of the central banks expected to move rates this week, with the market pricing in around a 75% chance of a further 25bp cut. This is justified by inflation having dipped back below 1%, and we see little reason for the SNB to hold off. The risks should therefore be on the downside for the CHF, which has also come under pressure from the better performance of the European equity markets of late due to the combination of hopes of increased spending and an end to the Ukraine war. CHF/JPY continues to look to have the clearest potential to decline, with Japanese yields already above CHF yields and CHF/JPY still some 50% above the level seen pre-pandemic. The 165.30 low from last September looks to be a key level, with a break potentially leading to further sharp losses.

Apart from the central bank meetings, there will be interest in the US retail sales data, Canadian CPI, and UK and Australian labour market data. But the current data is generally being seen as slightly old news because of the new policy initiatives on both sides of the Atlantic. The market is more likely to react to news on tariffs than any data, although surveys could have an impact. The US University of Michigan survey last week showed worrying weakness in confidence and rising inflation expectations, so there may be more interest than usual in the Empire manufacturing and Philly Fed surveys. We still see USD weakness over the course of the year, but if the Fed is wary of rate cuts recent weakness may not extend further until or unless we have evidence of weakening growth.

Data and events for the week ahead

USA

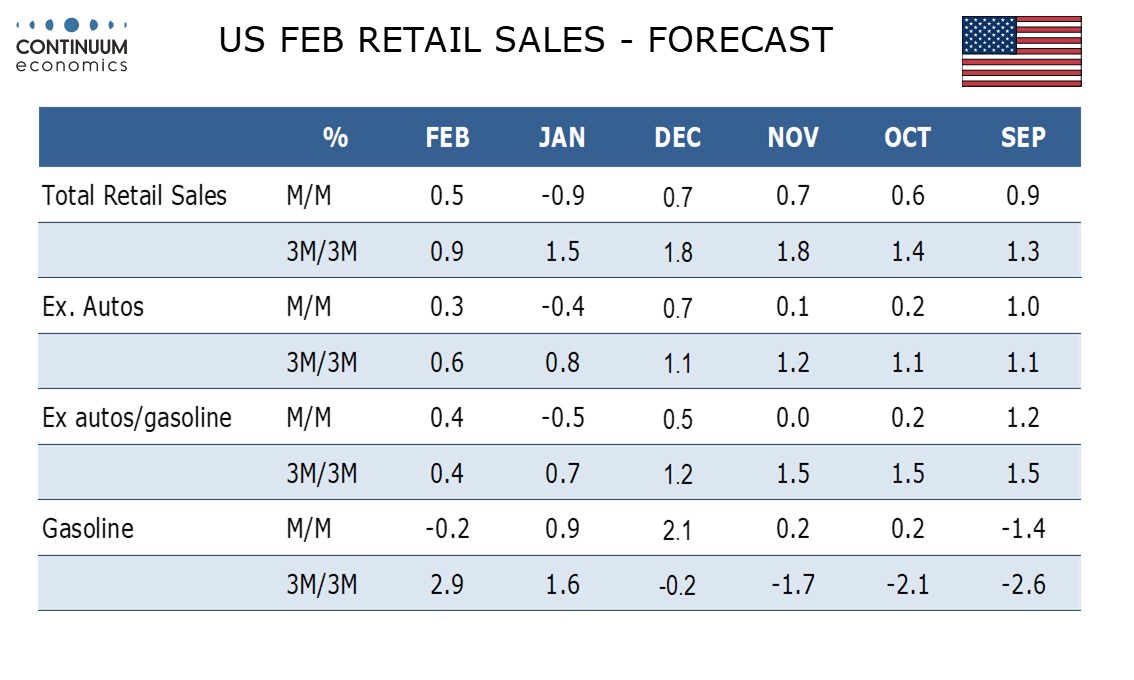

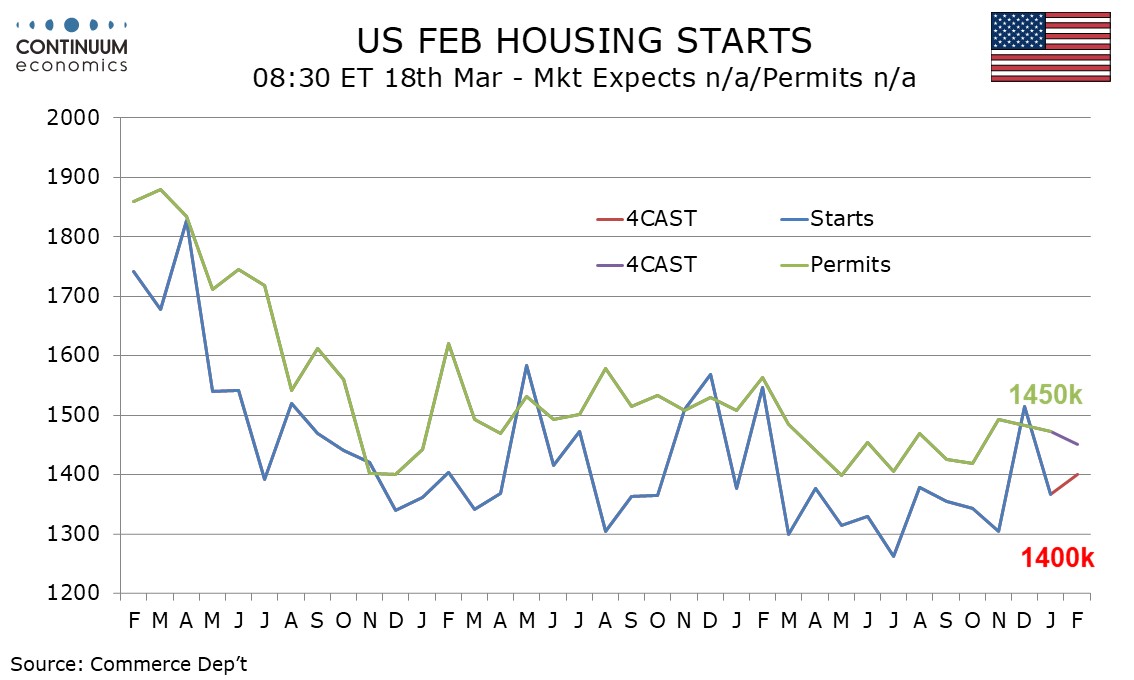

A busy week in the US will start with Monday’s February retail sales release, where we expect a 0.5% increase, 0.4% ex autos, neither fully reversing declines seen in January. March’s Empire State manufacturing survey will be released with the retail sales report. January business inventories, where existing data suggests a rise of 0.3%, and March’s NAHB homebuilders’ survey will follow. On Tuesday we expect February housing starts to rise by 2.5% to 1400k but permits to fall by 1.6% to 1450k. We also expect February industrial production to rise by 0.4%, with a 0.5% increase in manufacturing.

Wednesday sees the FOMC meet, and no change in rates is likely and forward guidance will be limited given extreme uncertainty, particularly over the impact of tariffs. Eyes will be on the dots, but we do not expect them to change much from January. Quantitative tightening may however be trimmed, to reduce risks associated with a potential upcoming stand-off over the debt ceiling.

Thursday sees weekly initial claims, March’s Philly Fed manufacturing survey and the Q4 current account, where we expect the deficit to rise to a record $325bn from $310.9bn. February existing home sales follow, where we expect a fall of 3.2% to 3.95m, as well as February’s leading indicator. There is no significant data due on Friday but Fed’s Williams is due to speak.

Canada

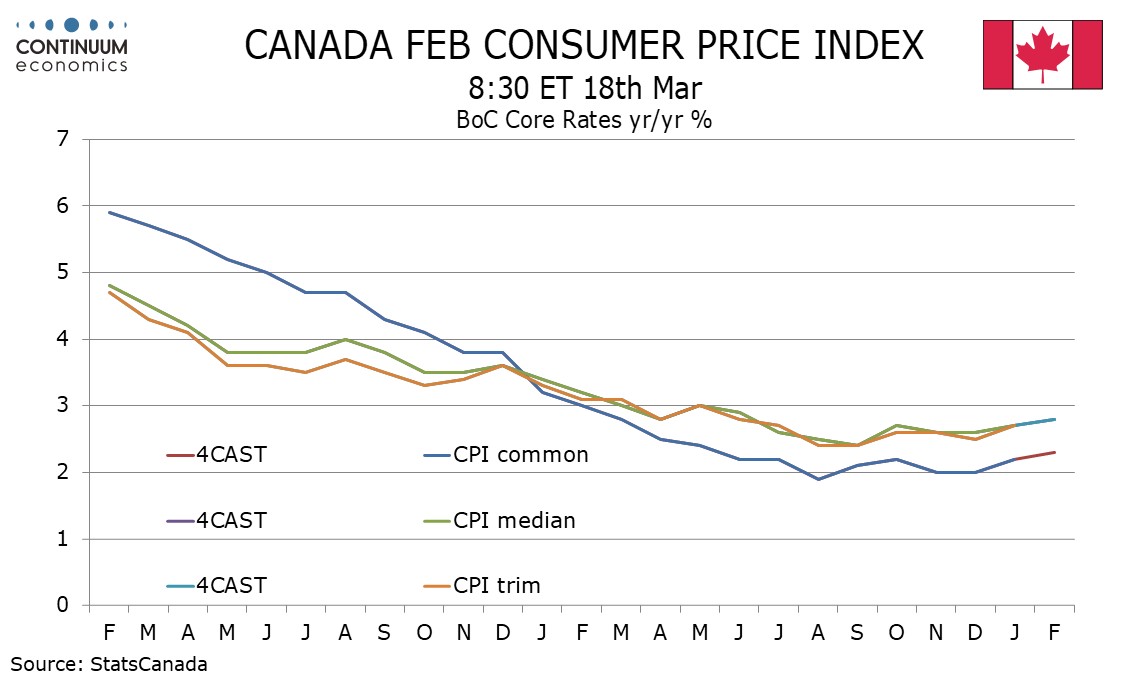

In Canada, Monday sees February housing starts and existing home sales data. The most important release of the week is likely to be February CPI on Tuesday, where we expect a rise to 2.1% yr/yr from 1.9% with firmer data from the BoC’s core rates too. Thursday sees February’s IPPI and RMPI. Friday sees January retail sales, for which the preliminary estimates was for a 0.4% decline.

UK

The BoE enters centre-stage this Thursday with its next verdict but may get some negative insight into the economy from CBI survey data beforehand |(Tue). But the implied MPC divisions that still allowed January’s cut probably reflected increased uncertainty enough for the BoE to have altered its rhetoric somewhat to stress the need for policy to be framed carefully as well as gradually. This very much points to stable policy (Bank Rate still at 4.5%) at this looming March 20 meeting, with it increasingly likely that the MPC majority envisages rate cuts not faster than every quarter this year and a little further into 2026.

But it is a little ironic than that the next MPC decision will arrive the same day as the next set of labor market numbers, the apparent wage resilience having perturbed some MPC members – NB; the BoE will have advance access to these numbers. But this data release, now encompassing updates not just from the long-standing ONS but also real time figures from the HMRC (which we suggest are more authoritative data), show that employment is continuing to contract and this may be the case even with average earnings data likely to show little change.

Friday sees public borrowing numbers, the latter still likely to show borrowing in the first eleven months of 2024-25 is running both (further) above the year-before and above the monthly profile consistent with the OBR’s October forecast.

Eurozone

The week sees little in terms of data although German ZEW figure (Tue) will provide more interest than usual as it will assess the growing tariff worries but also the clear German recent fiscal initiatives. The latter may filter into consumer thinking thereby affecting the EZ consumer confidence update (Fri). EZ construction data (Thu) may add to signs that the economy was weak at the start of 2025. Indeed, on Friday, INSEE business survey data may suggest a continued weak start to 2025 – at least in France. Otherwise, final HICP data may confirm weaker services inflation (Wed)

Rest of Western Europe

There are key events this week, all at least to us confined to Thursday. In Sweden, having delivered in January, the widely-expected sixth successive rate cut, the Riksbank adhered to the assessment made in December that the easing cycle has drawn to an end with the policy rate (down to 2.25%) having dropped 1.75 ppt in eight months. Especially given the recent upside CPI surprises, this very much points to no move at the looming decision and with a stable policy outlook likely to be reinforced by updated projections that may continue to point to above-consensus growth this year and next.

In Switzerland, we see a further SNB rate cut of 25 bp at this month’s quarterly assessment taking the policy rate to 0.25%, the lowest since Sep 2022, ie when the Board moved away from negative rates. A return to negative rates is a risk that the SNB has itself noted but we think that policy will instead be put on hold after the envisaged further cut this month. In Norway, the Norges Bank releases its influential Regional Survey

Japan

The BoJ meeting will be on Wednesday when we expect no change to interest rate as they will likely wait for more confirmation from the spring wage negotiation. It is also unlikely for the BoJ to change forward guidance with little new impetus. Trade balance will also be released on the same day and should continue to point to good export despite JPY strengthens relatively. National CPI on Friday would be more important as we should be seeing a moderation from the 4% in January, if not it may suggest the BoJ will even hike earlier than we thought, currently first hike forecast in May,

Australia

We only have the labor data for Australia next week on Thursday. The labor market has been surprising solid for the past year despite wage growth is not proportionate. However, another strong beat may deter the RBA to ease further soon.

NZ

We will have the NZ GDP on Thursday. It would be interesting to see if the NZ escapes recession. Trade Balance will be released on Friday but both impact in the FX market is likely to be knee-jerk, given the clear easing path from the RBNZ.