FX Daily Strategy: Asia, April 29th

BoE Divided Again But Unmoved

Real Economy Buckling Already for ECB

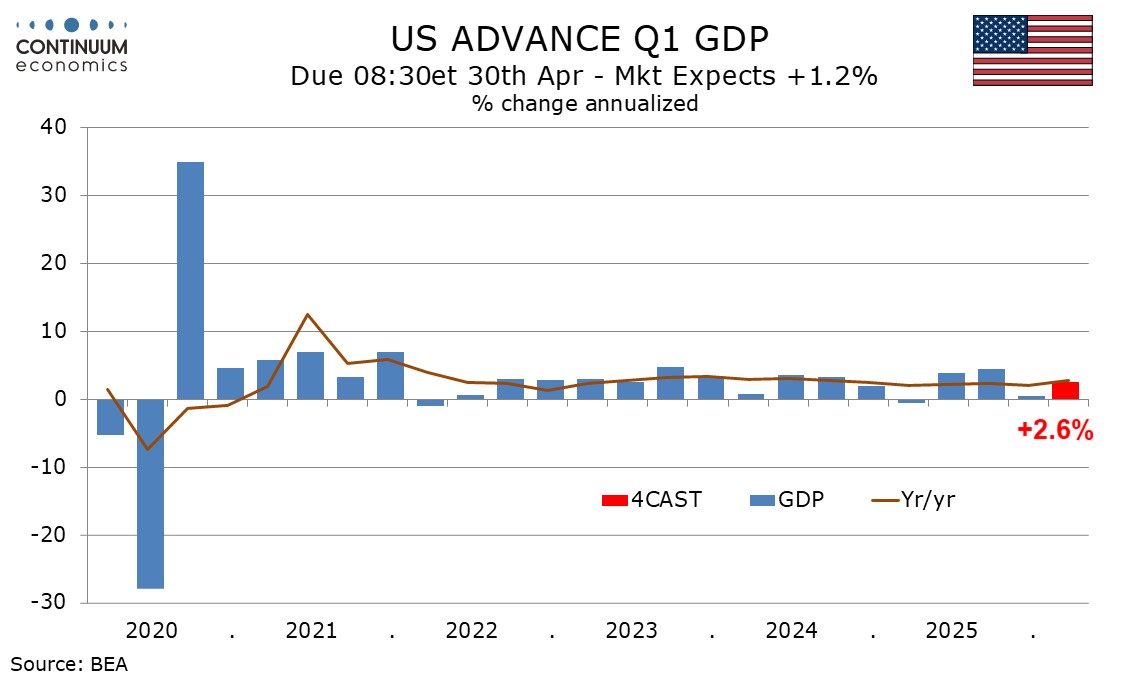

Government Spending to lead bounce for U.S. Q1 GDP

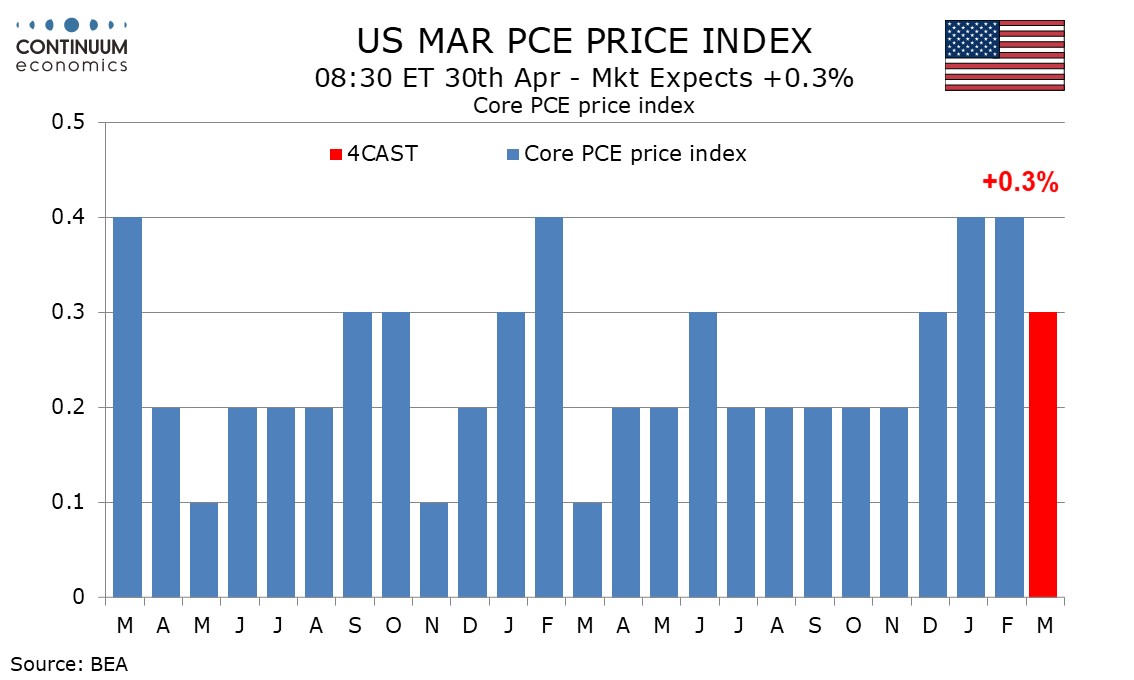

U.S. March Core PCE Prices to outperform core CPI

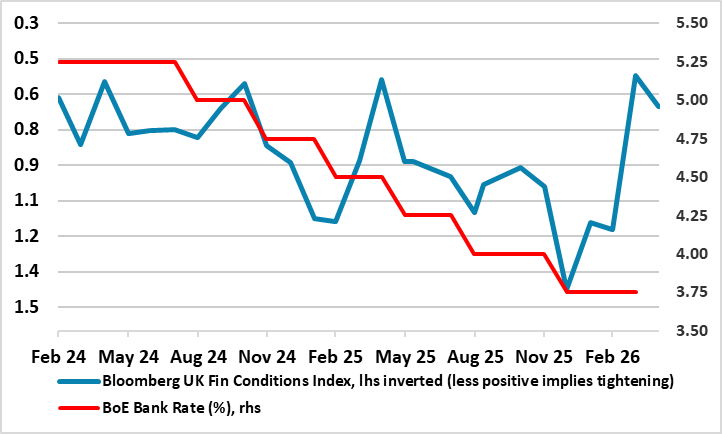

Figure : Bank Rate and Financial Conditions Diverging (% and level)

Very clearly, the BoE kept rates on hold with the MPC unanimous last month and the same decision is expected this time around but with probable fresh dissent, with up to 2-3 members opting for an immediate hike. These splits will be even more evident in the individual MPC member statements (as expected) where more diverging views may again act to confuse markets seeking a clearer communication from the BoE. But the MPC overall will retain a more neutral stance, being ‘ready to act as necessary to ensure that CPI inflation remains on track to meet the 2% target in the medium term’. The minutes may again suggest that this is symmetric that policy may have to be more or less restrictive depending on the economic impact, albeit with the alternative scenario based more towards inflation persistence. However, Governor Bailey may repeat is assertion that downside and upside risks exist together. What is notable and as the updated projections may show, is that this energy shock is justifiably viewed as being different to that of 2022, occurring at a point when the economy is operating with a margin of spare capacity. We think this very much reduces the chances of second round effects.

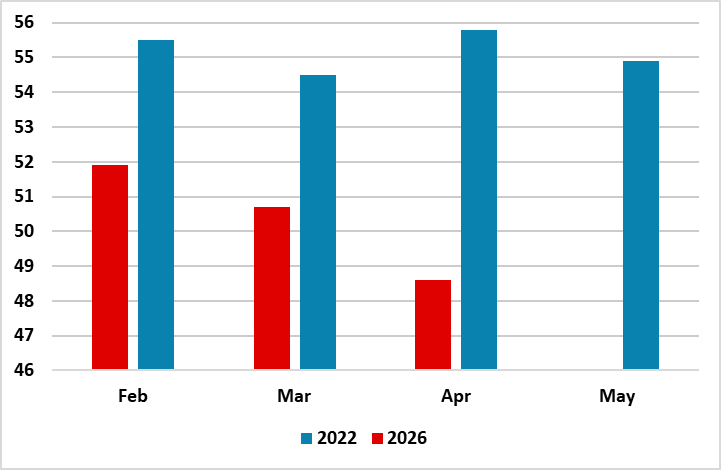

Figure: Real Economy Hit Clear(er) This Time Around

We again expect no change from the ECB on Apr 30, but President Lagarde will probably have to admit in the Q&A that unlike last time the decision was not unanimous. Overall, the communication will again suggest upside risks for inflation and downside risks for economic growth the extent and duration of both depend both on the intensity, length and likely resolution of the conflict. We still think the ECB is too pessimistic about inflation and too optimistic about growth as PMI data have started to show (Figure). And a series of data updates in the coming week may highlight this further, not least a bank lending survey showing probably increasing, signs of banks wariness about lending. In coming months, and given the manner in which the ECB may feel it cannot afford a repeat of what some call the policy mistake of four years ago, a rate hike by mid–year cannot be ruled out. But, this would be a mistake, ignoring how the policy and economic backdrop is vastly and increasingly different to then. As a result, we still see the next move being a cut to address adverse monetary condition albeit very late in the year!

We expect a 2.6% annualized increase in Q1 GDP, improved from a weak 0.5% in Q4 largely due to a rebound in government from Q4 data that was depressed by a shutdown. Excluding government we expect a second straight quarter close to 1.5%. We expect a significant acceleration in core PCE prices, to 4.1%, the highest since Q1 2023, from 2.7% in Q4. We expect government to rise by 6.7%, more than fully reversing a shutdown-induced 5.6% decline in Q4. However we expect slower growth from state and local government and within the Federal detail so not expect a full reversal in non-defense Federal spending. Government did return to growth in Q3 after DOGE-related declines in Q1 and Q2, and we expect moderate growth going forward.

March’s personal income and spending data may be overshadowed by the Q1 GDP report due at the same time and to which it will contribute. We expect a 0.9% rise in personal spending, to exceed both a 0.2% rise in personal income and a 0.7% rise in PCE prices. For core PCE prices, we expect an increase of 0.3%. CPI increased by 0.9% in March with core CPI up a moderate 0.2%. A 0.7% rise in PCE prices would be consistent with the fact CPI is more sensitive to gasoline prices than PCE prices. We expect core PCE prices to rise by 0.3%, exceeding the core CPI. While March’s core PPI was subdued, its components that contribute to core PCE prices were firm.