FX Daily Strategy: APAC, October 8th

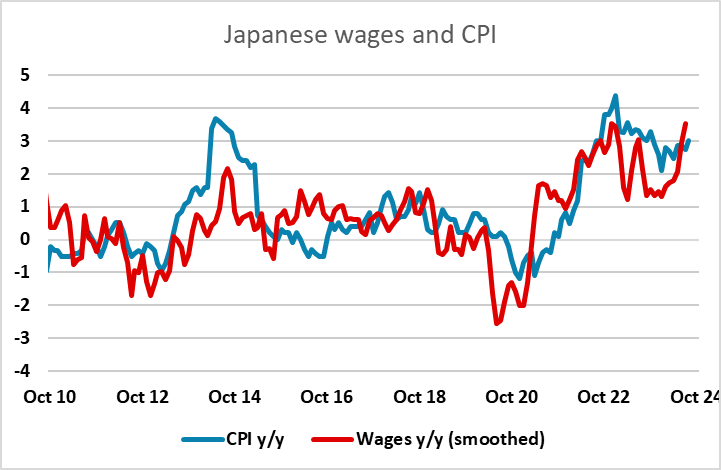

Japanese wage data of interest given recent JPY weakness and dovish policy comments

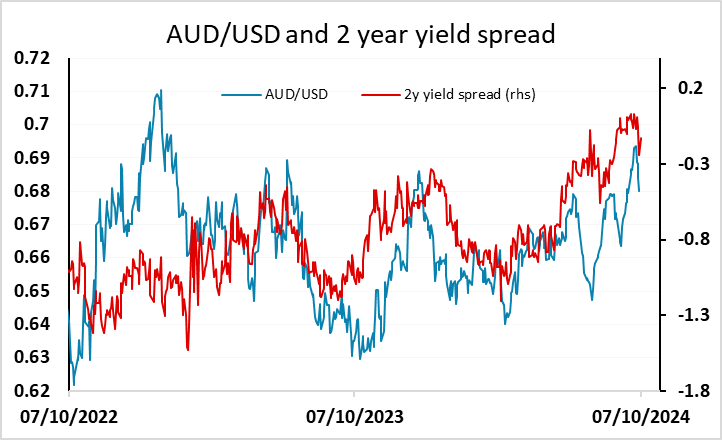

AUD still has upside scope if RBA minutes don’t sound more dovish

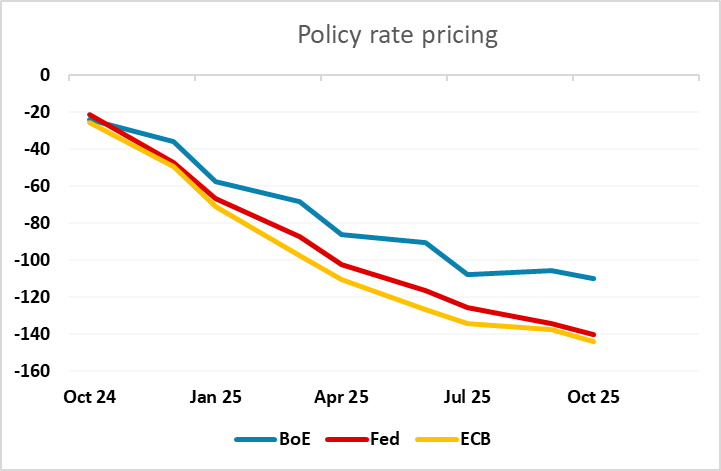

GBP weakness can extend

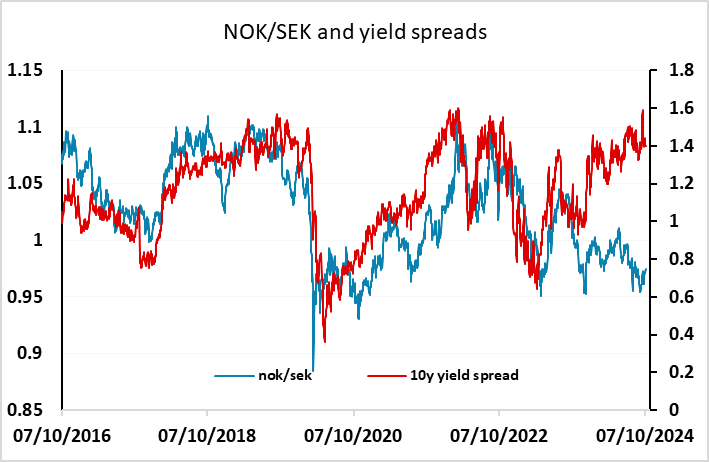

NOK/SEK starting to move higher

Japanese wage data of interest given recent JPY weakness and dovish policy comments

AUD still has upside scope if RBA minutes don’t sound more dovish

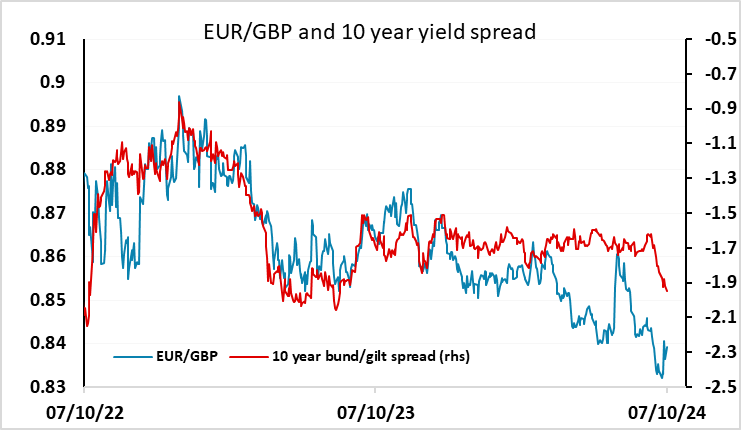

GBP weakness can extend

NOK/SEK starting to move higher

Tuesday is a fairly quiet day for data, with most of the market focus on the US CPI data later in the week. However, given the weakness of the JPY in recent weeks, and particularly since the employment report, there might be more interest than usual in the Japanese wage data. The August wage data was strong, and the trend has certainly been rising strongly, with wage growth now exceeding CPI growth for the first time since early 2022. The weakness of Japanese incomes growth has been one of the main factors discouraging the BoJ from tightening, so this strength will have been welcome. With a consensus of 3.0% the August data is expected to show a slightly less strong rise than the July numbers, and even though this would still keep wage growth at levels sufficient to sustain the hopes of a recovery, it would be unlikely to lead to any increase in expectations of early BoJ tightening. The comments from Ueda and Ishiba recently indicate that an October tightening is not on the cards, but we still see scope for a move in December, and unless the wage data is much weaker than expected, we will continue to anticipate a December hike. As it stands, the market is pricing only 8bps of December tightening, and 33bps by the end of 2025. This still seems on the low side to us, and the JPY has potential for a recovery if the wage data are strong given recent weakness and yield spreads that still suggest current JPY levels are too low.

There are also minutes from the last RBA meeting, but these seem unlikely to significantly change expectations for RBA policy. Currently a 25bp December rate cut is seen as a little less than a 50-50 chance, and while the minutes are likely to keep hopes of an easing alive, we doubt they will show a stronger bias to ease than the market is currently pricing. The AUD has fallen back since the US employment report, but with the Chinese equity market trading more solidly, AUD/USD should find good support below 0.68 with yield spreads still supporting the case for an AUD/USD move to 0.70.

There isn’t a great deal of note on the European calendar, but it was noticeable on Monday that EUR/GBP moved back up towards 0.84 after dipping following Friday’s employment report. The market is now pricing the BoE moving more closely with the Fed and ECB in the coming months, but is still pricing relatively tighter BoE policy further out. We still see scope for the market to price in easier BoE policy in 2025 and this would suggest more GBP downside scope. As we have noted before, EUR/GBP remains quite cheap from a longer term perspective, and if the BoE matches the ECB, there should be scope for a move up well above 0.85 over the coming months.

Finally, it’s worth noting that NOK/SEK is starting to make some upside progress, hitting its highest since August on Monday. The NOK may be being helped by the rise in the oil price and concerns about potential supply disruption due to the Middle East conflict, but in the bigger picture yield spreads have been suggesting scope for substantial gains for some time. If sentiment is turning there is scope for a sharper move up towards parity.