FX Daily Strategy: APAC, September 11th

US CPI the focus

More risk of market reaction on stronger data

GBP focus on GDP with firm tone intact

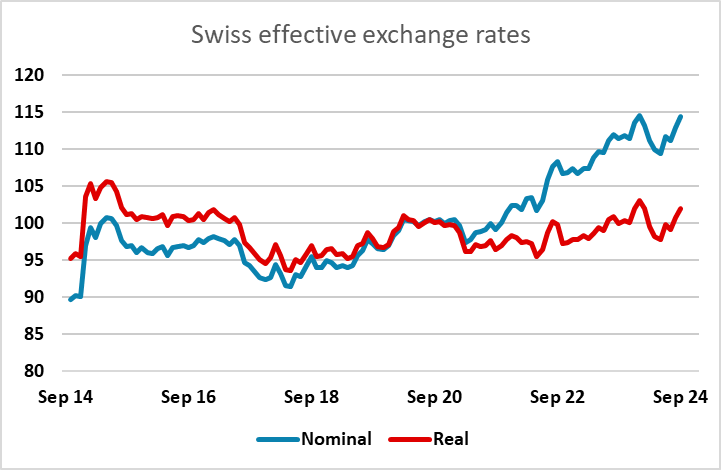

CHF strength reaching limits

US CPI the focus

More risk of market reaction on stronger data

GBP focus on GDP with firm tone intact

CHF strength reaching limits

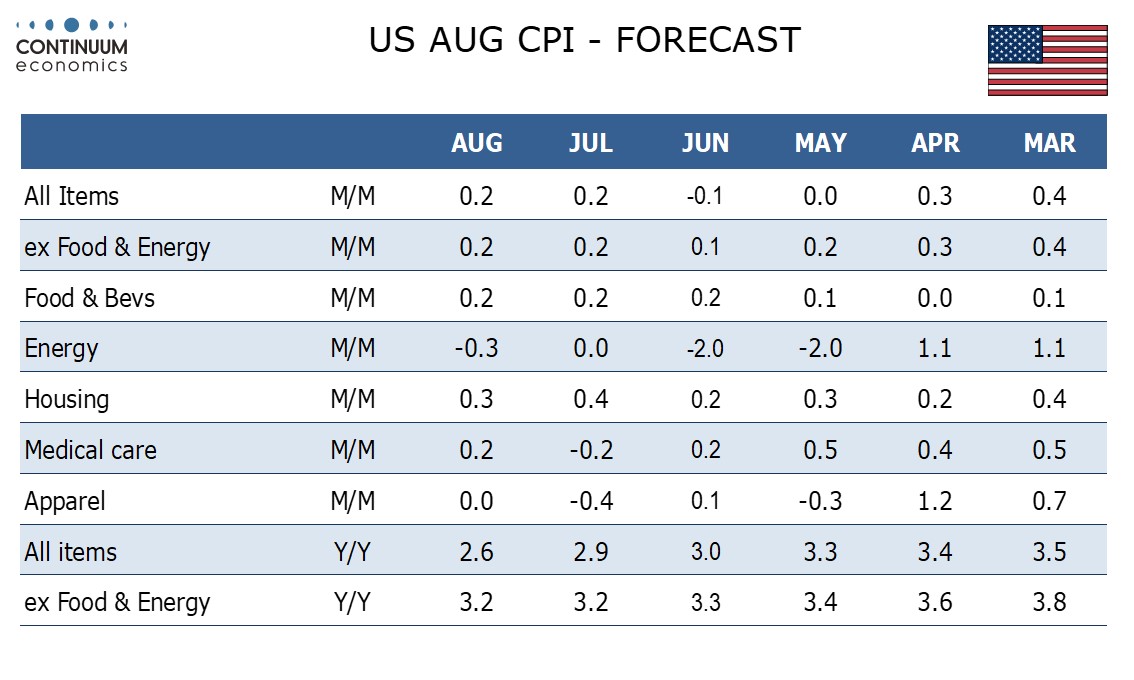

Wednesday sees the main release of the week in the form of US August CPI. We expect August’s CPI to increase by 0.2% both overall and ex food and energy, with the respective gains before rounding being 0.18% and 0.21%. Such an ex food and energy rate would be slightly stronger before rounding than in the preceding three months, though not strong enough to trouble the FOMC. Our forecasts are in line with the market consensus, so we wouldn’t anticipate any significant reaction. Market risks are probably greater on a strong than a weak number, as the chances of a 50bp cut from the Fed likely hinge on weaker real sector data rather than weaker CPI, while stronger CPI data would kill hopes of more aggressive Fed easing and consequently potentially trigger a risk sell off. Softer data might trigger a mild risk positive reaction. However, even in this scenario we might well see lower US yields so that the USD weakens against the lower yielders ads well as the riskier currencies.

Tuesday saw another strong JPY performance in the US session as equities turned lower. US equities held up better than Europe, and the JPY gained more on the crosses than against the USD, with EUR/JPY hitting its lowest since August 5. While yield spreads suggest there is some upside risk for EUR/USD, both USD/JPY and EUR/JPY continue to be biased lower due to yield spreads and declining risk premia, and in a weak risk environment EUR/JPY and other JPY crosses are likely to remain the most vulnerable. Soft US CPI might allow some reversal of Tuesday’s JPY strength, but if CPI is at or above expectations the JPY is likely to stay firm on the crosses.

In Europe, there is UK GDP data for July, with the consensus looking for a 0.2% rise after a flat June. Our forecast is in line with the consensus, and we consequently wouldn’t look for much GBP reaction. But a return to growth after a flat June would if anything support the firm GBP tone we have seen in recent weeks, and potentially allow a EUR/GBP test lower towards 0.84. While we continue to see GBP as a little expensive against the EUR here from a medium and long term perspective, weaker data or more clearly risk negative news is needed if the recent EUR/GBP downtrend is to be reversed.

The weaker risk tone on Tuesday also saw the CHF continue to make gains against the higher yielders, but EUR/CHF is now getting into territory that the SNB is likely to see as too strong, testing the post-2015 real terms highs seen earlier in the year. Unlike the JPY, there is no case of undervaluation of the CHF, and unless we see a clearer case for a risk sell off, EUR/CHF should be near a bottom close to 0.93.