FX Daily Strategy: APAC, August 29th

Quiet calendar on Wednesday suggests no major moves

CHF and GBP strength have been notable in recent days

CHF strength hard to justify, but could extend a little further on technical

GBP benefiting from relative hawkish expectations on policy, but looks toppy

Eurozone CPI data unlikely to have much impact on ECB expectations

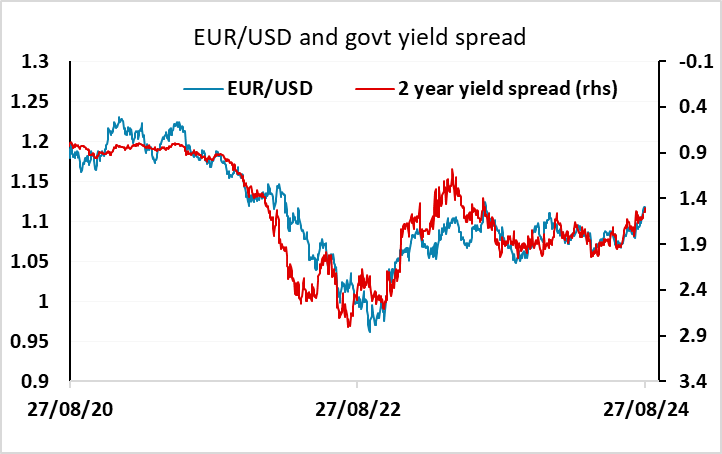

EUR/USD looks fair based on current yield spreads

GBP supported by relatively hawkish BoE, but looks expensive

USD may have upside scope as data continues to show solid growth

Preliminary August CPI from Spain and Germany, the August EU Commission survey and revised US Q2 GDP data are the main data on Thursday. There is also revised Q2 GDP data for Sweden and the latest Swedish economic tendency survey.

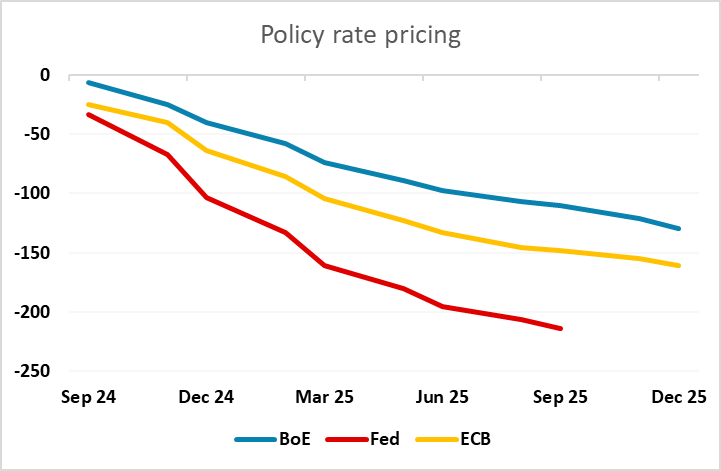

The market consensus is for some further declines in y/y CPI in both Spain and Germany, with the decline in Germany in August possibly helped by the July numbers having been boosted by the European football championships. For similar reasons, the August numbers in France may be boosted by the Olympics, but these aren’t due until Friday. As it stands, the market is pricing a fairly gentle pace of easing from the ECB relative to the Fed, due to a lower starting point, an earlier start and a slightly less rapid decline in inflation. It’s hard to see the market pricing in much more than the 150bps of easing over the next year currently in the market, given that the terminal rate is only seen slightly below this at 2.0%. So even if the inflation data is a little weaker than expected, we wouldn’t expect any substantial decline in Eurozone yields. There is probably more scope for yields to rise if we see higher inflation combined with solid growth data, but at this stage a major change on view seems unlikely.

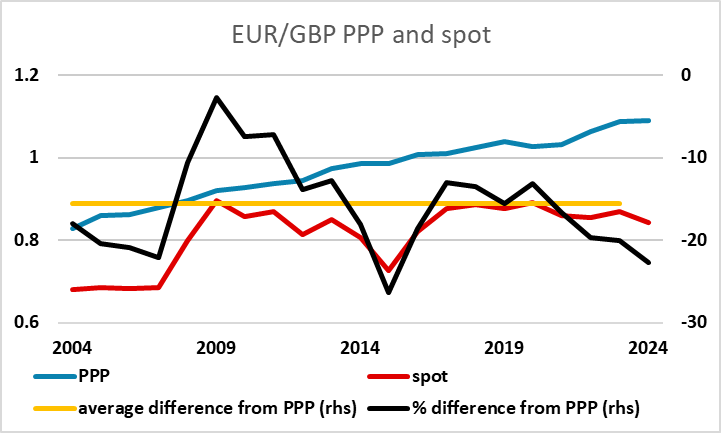

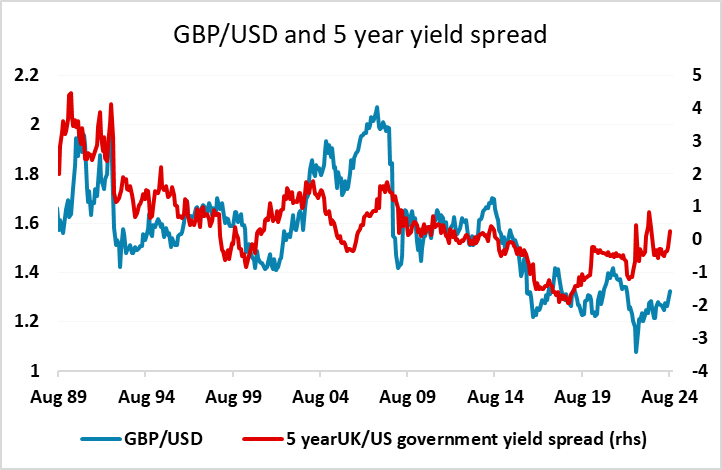

There is more uncertainty about the Fed and Bank of England policy paths, given the higher starting points and the greater typical volatility. As it stands, the Fed is expected to ease a lot more quickly than the BoE, and although this relates partly to the BoE’s earlier start, it does suggests that there is scope for some convergence in the pace of easing. As it stands, EUR/USD looks close to fair based on the steady relationship with 2 year government yield spreads. GBP has performed better in the last couple of weeks as BoE governor Bailey has discouraged expectations of early or rapid easing, and there does look to be some scope for GBP/USD gains based on the historic relationship with yield spreads. This relationship is easier to assess in the long term than EUR/USD, as inflation has been more similar in the US and UK, while Eurozone inflation has generally been lower historically. So while EUR/GBP weakness looks justified based on historic nominal yield spreads, the picture is very different when relative inflation is taken into account. The real EUR/GBP exchange rate is low by historic standards, and this, combined with the potential for the BoE to ease more rapidly than the market is currently pricing in, suggests to us that EUR/GBP will struggle to extend recent losses.

We don’t expect any significant change in the US Q2 GDP data, but the fact that it is likely to be close to 3% annualised emphasises the fact that there isn’t a very strong case for more rapid Fed easing at this point. With the market still pricing around a 30% chance of a 50bp Fed rate cut in September, the risks look to us to be on the upside for the USD in the short term.