Preview: Due August 29 - U.S. July Advance Goods Trade Balance - Deficit to rebound after June dip

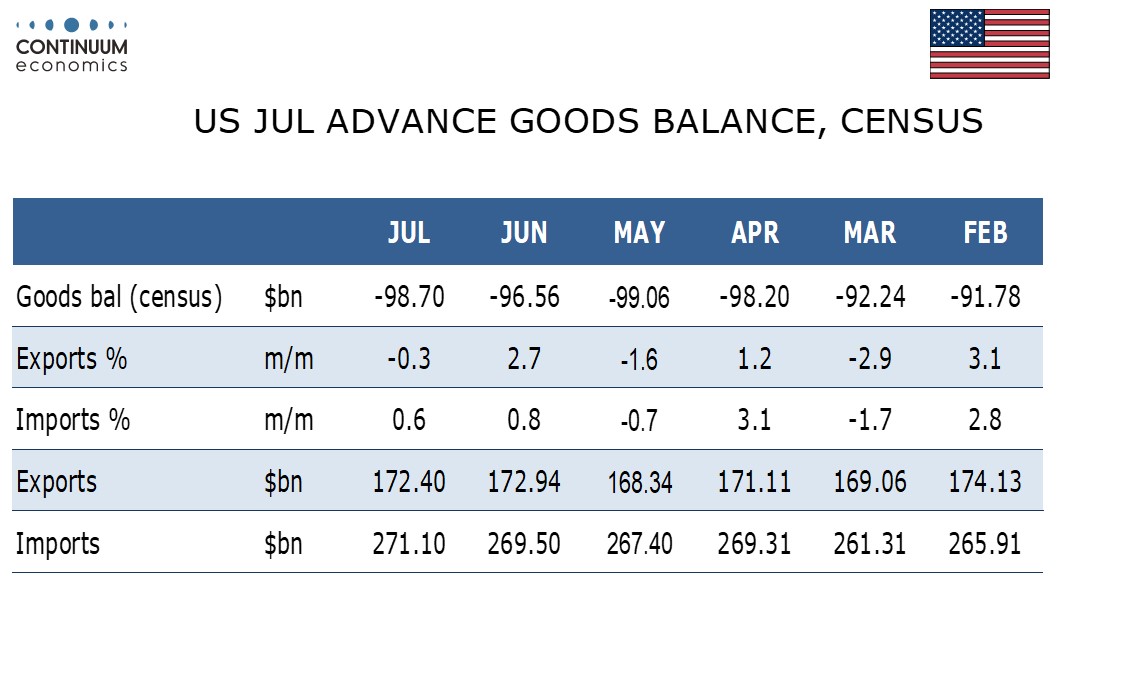

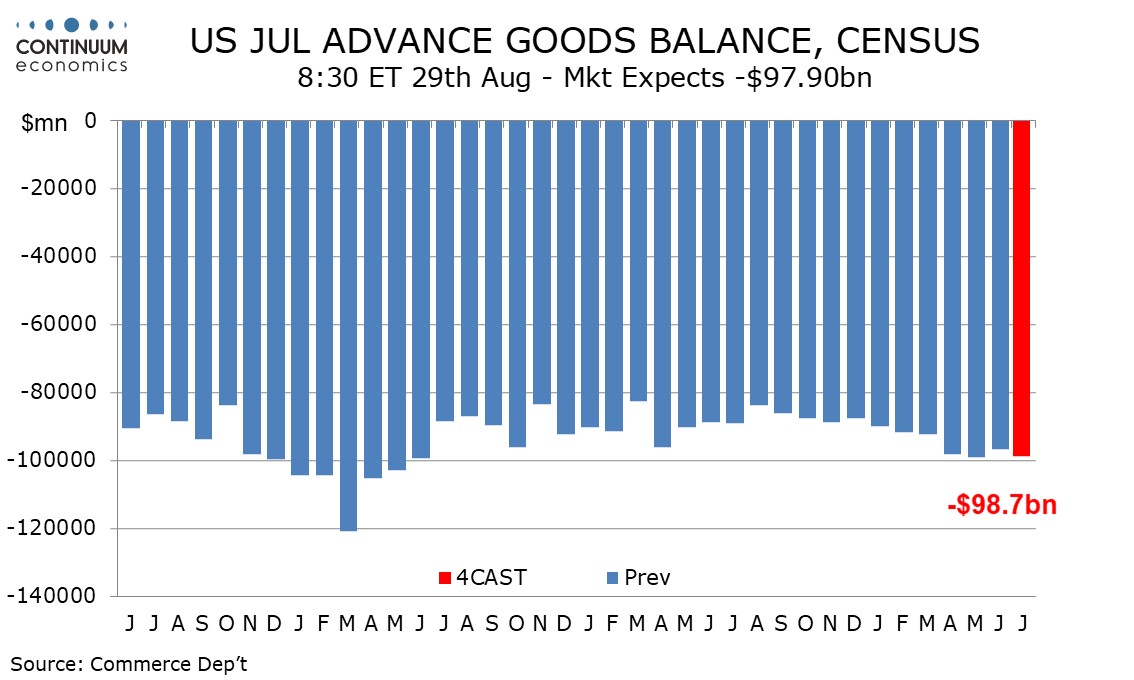

We expect July’s advance goods trade deficit to increase to $98.7bn from June’s 96.6bn, leaving it slightly below the May deficit of $99.1bn which was the highest since May 2022.

We expect exports to fall by 0.3% after a 2.7% June increase while imports rise by 0.6% after a 0.8% increase in June. In real terms we expect the deficit to reach its highest level since May 2022 but exports will gain some support from a 0.7% rise in prices, while import prices increased by only 0.1%.

Suggesting weakness in exports is a fall in July industrial production, led by autos. Data from Southern California ports suggests increasing strength in imports. Advance July wholesale and retail inventory data will be released with the advance goods trade report, providing further insight on Q3 GDP prospects.