FX Weekly Strategy: July 22nd-26th

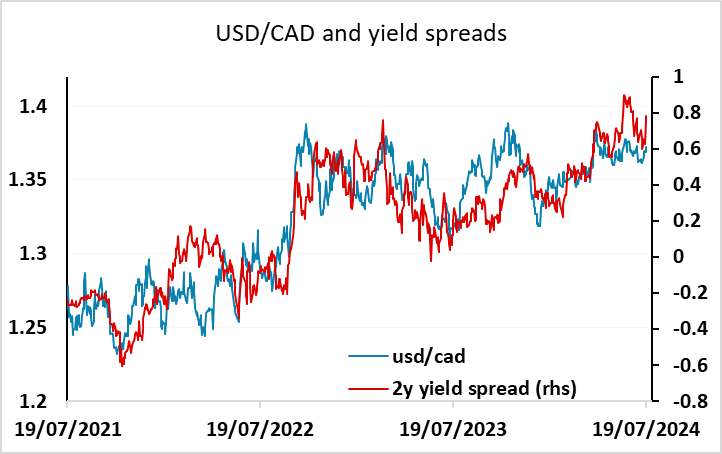

CAD upside risks on BoC

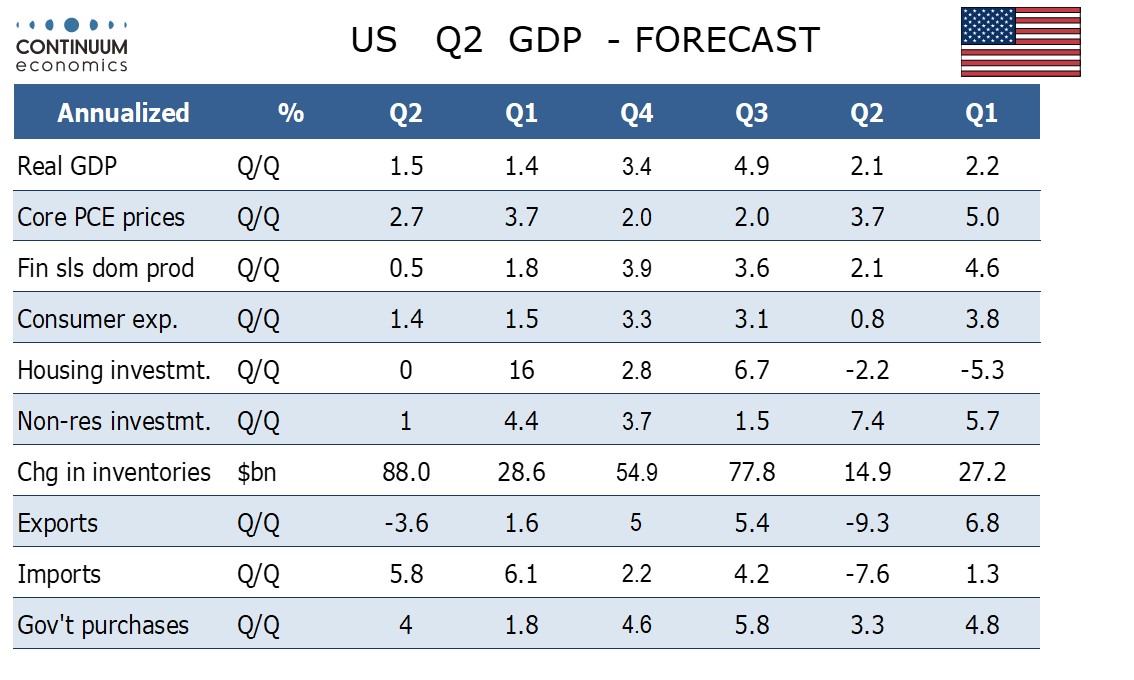

Some USD downside risks on US GDP

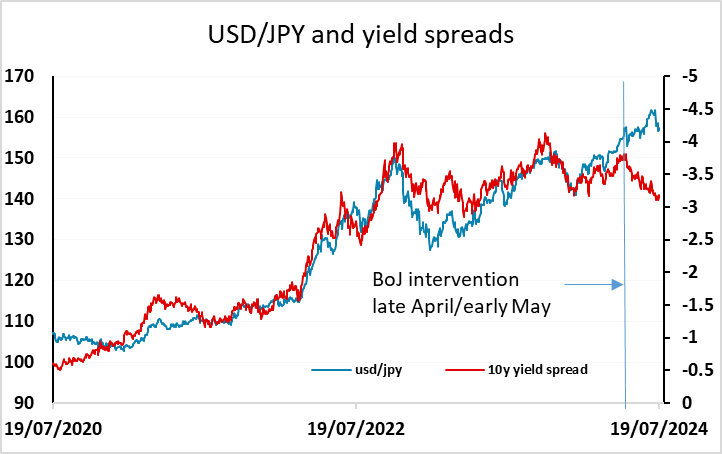

JPY may have upside scope on the crosses

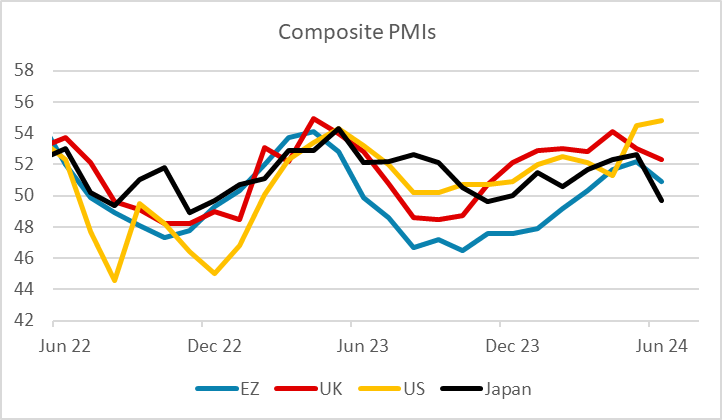

PMIs a focus for European currencies

Strategy for the week ahead

CAD upside risks on BoC

Some USD downside risks on US GDP

JPY may have upside scope on the crosses

PMIs a focus for European currencies

Datawise the US Q2 GDP data, S&P PMIs and the Japanese Tokyo CPI data are the main focuses this week. But we also have the BoC monetary policy meeting which could well have a market impact.

A rate cut is 90% priced for the BoC meeting, and around 75% of forecasters are looking for a rate cut. So there would not be much impact on the market if the BoC do cut rates. But we expect the BoC to surprise the market by leaving rates unchanged. Given market pricing, the risks for USD/CAD should be substantially on the downside, with limited upside on a rate cut, and substantial downside if rates are left unchanged. As it stands, USD/CAD could edge up to 1.3750 based on current yield spreads, but the USD is somewhat expensive from a longer term perspective, and there is scope for USD/CAD to drop a figure or more if the BoC leave rates unchanged.

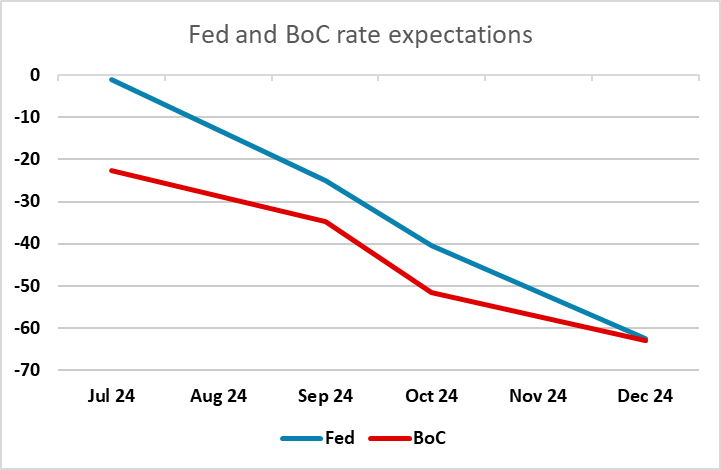

The US Q2 GDP numbers are the most likely market mover in terms of data. We see some downside risks for the data and the USD, with the market consensus at 2.0% and our forecast at 1.8%. There will be some focus on the PCE price data attached to the release as well. We expect a drop to 2.7% annualized from 3.7% in Q1. But with a September Fed rate cut already fully priced in, and 63bps of easing priced by the end of the year, there isn’t a lot of scope for the market to price in any more easing this year. There should therefore be somewhat limited scope for the USD to fall against the riskier currencies, with more scope for USD gains if the data surprises on the upside.

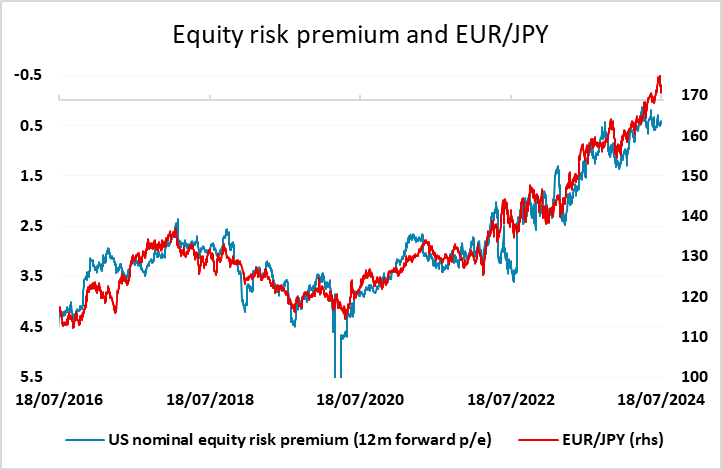

The JPY situation remains very different from the majority of other currencies. After the recovery of the last week, USD/JPY has broken below a key trendline, but JPY crosses have generally held trendline support so far. The risks may therefore be greater in the JPY crosses short term. The only obvious trigger for JPY action this week is the Japanese Tokyo CPI data on Friday, where any evidence of strength might increase expectations of BoJ tightening at the July 31 meeting. This is currently priced as a 40% chance, while the consensus is for a small increase in the Tokyo CPI y/y rate to 2.2% ex-fresh food. But JPY crosses tend to be driven more by general risk sentiment than by yield spreads. If yield spreads were the driver, the JPY would already be a lot higher against all the major currencies. As it stands, even measures of equity risk premia already suggest some JPY upside risks.

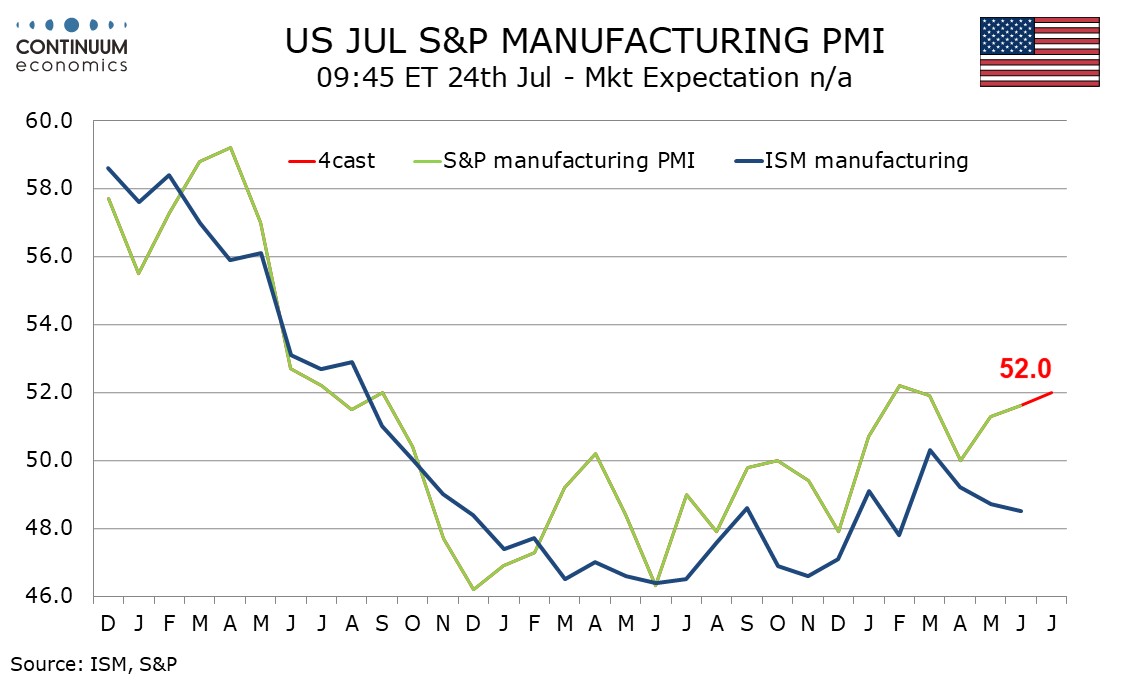

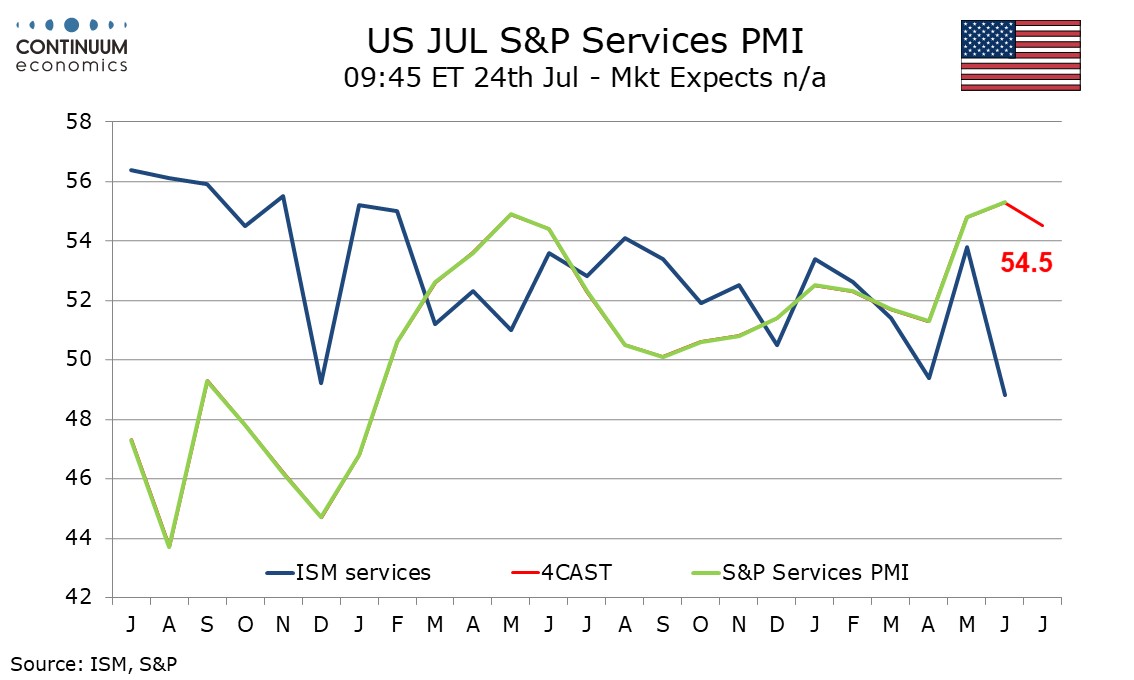

Flash PMIs with be a focus for European currencies after somewhat disappointing numbers in June, particularly relative to the US. But the strong US numbers contrasted with somewhat weaker ISM data, so there is certainly some risk that the US indices correct lower towards Europe. Growth sentiment has certainly improved in Europe in the last few months, notably in the UK, and strong PMI numbers this week, particularly relative to the US, could determine the tone for EUR/USD and GBP/USD. Positioning, yield spreads and valuation all suggest that GBP strength in recent weeks is somewhat overdone, so GBP may be particularly vulnerable if PMIs disappoint.

Data and events for the week ahead

USA

The US week ahead starts quietly with little scheduled on Monday and Fed officials expected to be quiet as the July 31 rates decision draws closer. On Tuesday we expect June existing home sales to fall by 3.2% to 3.98m but on Wednesday we expect June new home sales to correct higher by 1.0% to 625k. Wednesday also sees advance June goods trade, where we expect the deficit to increase to $100.0bn from $99.4bn.

Q2 GDP on Thursday is probably the key release of the week. We expect a 1.8% annualized increase, slightly stronger than Q1’s 1.4%, with a slower 2.7% increase in the core PCE price index, down from 3.7% in Q1. Due with the GDP report are weekly initial claims and June durable goods orders, where we expect gains of 0.3% both overall and ex transport.

Friday sees June’s personal income and spending data, though fresh news will be limited with Q2 totals due with the GDP report. Ahead of the GDP report we expect a second straight subdued 0.1% rise in core PCE prices, with personal income up by 0.3% and personal spending up by 0.2%. Final July Michigan CSI data is also due on Friday.

Canada

With no significant data focus in Canada is on Wednesday’s Bank of Canada meeting, where a debate will be seen on whether to ease for a second straight meeting or leave rates unchanged at 4.75%. We expect the BoC to choose the latter option given limited further progress on inflation since the easing seen on June 5. However the BoC is likely to see the economy evolving in line with its projections made in March’s Monetary Policy Report, which will be updated at this meeting, and this would suggest further easing, if at a gradual pace, can be expected later in the year.

UK

Flash PMI data (Wed) are seen correcting back slightly in the July flashes (Fri), although there is some upside risks from the election result. The composite remained in expansionary territory during June, posting 52.1. While this did signal an eighth consecutive monthly increase in output across the UK service sector, the headline index fell again, from 52.9 in May, signalling the softest rate of growth since November last year. Otherwise, Thursday sees CBI survey numbers

Eurozone

Datawise, the main interest will be the PMI flashes on Wednesday, where we see a small further drop back in the composite having seen its recent upward trend thwarted at the end of the second quarter as it decreased for the first time since October last year. Down to 50.9 in June from 52.2 in May, thereby indicating a slowdown in the expansion, and signalled a rise in output that was the softest in three months and only marginal overall. Other business surveys are due, including the French INSEE figure and German Ifo numbers (Thu) where some declines may be in the offing. There is also EZ construction numbers (Mon) too and ECB attention with its consumer expectations survey (Fr) and some Council speakers due, most notable Chief Economist Lane (Tue).

Rest of Western Europe

In Sweden, there is labor market data (Fri), likely to remain volatile.

Japan

After the elevated national CPI this week, we will be seeing the Tokyo Cpi for July next Friday. While BoJ will hope for an extended period of higher inflation from a demand perspective, preliminary data does not suggest consumption to pick up. If there is another high read, it is very likely coming from the input side and would put BoJ in a hard place and careful with its steps. Our central forecast sees only a bond purchase cut in the July 30 meeting and no rate cut.

Australia

Clear calendar except PMI on Wednesday.

NZ

Trade Balance on Monday would be interesting to see after RBNZ signalling the possibility to ease when data allows. We also have consumer confidence on Friday.