FX Weekly Strategy: July 1st-5th

US employment report and French and UK elections are the event highlights

Reaction to elections likely to be muted

Mild USD downside risk on employment report

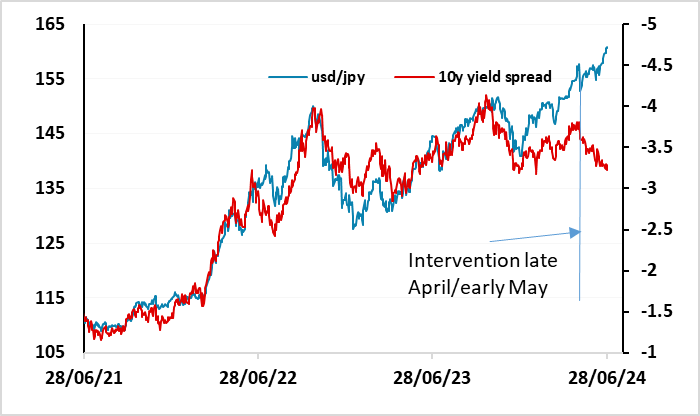

JPY remains in the spotlight

Strategy for the week ahead

US employment report and French and UK elections are the event highlights

Reaction to elections likely to be muted

Mild USD downside risk on employment report

JPY remains in the spotlight

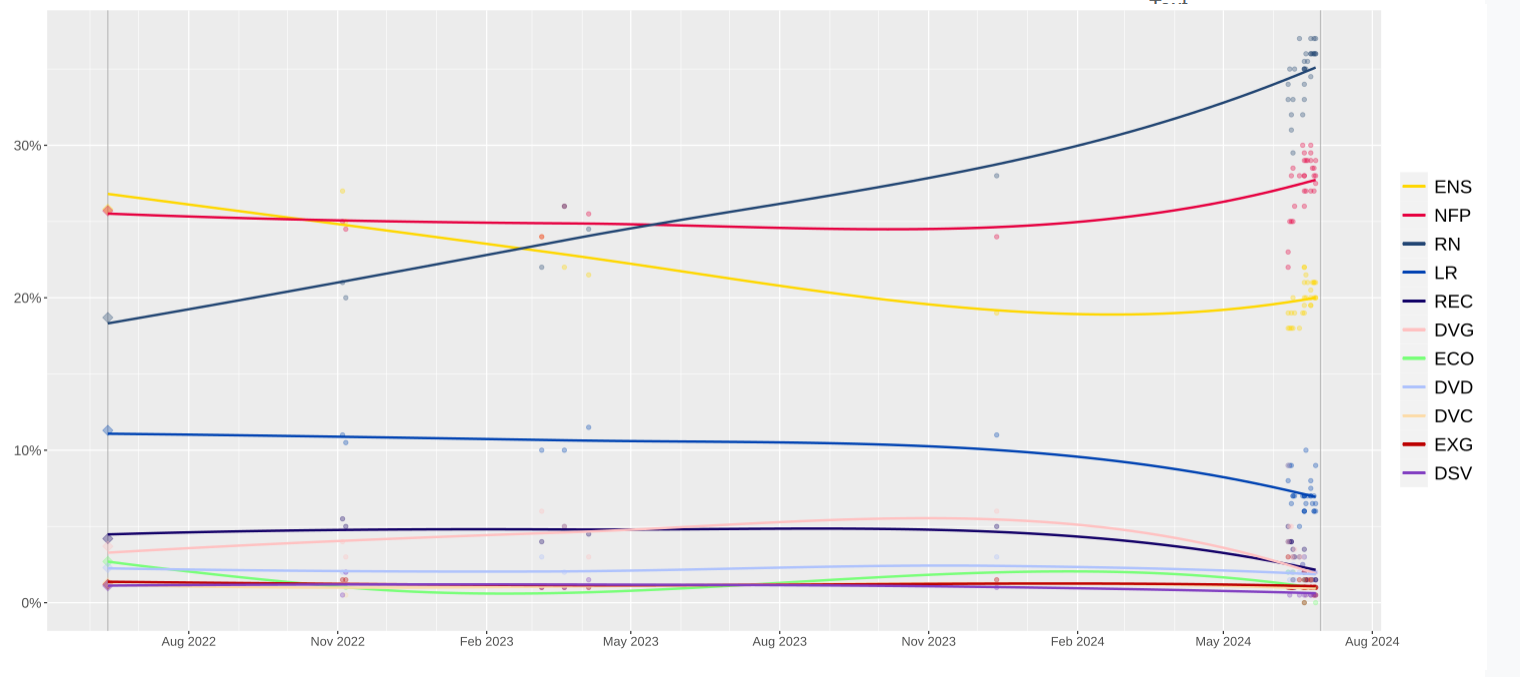

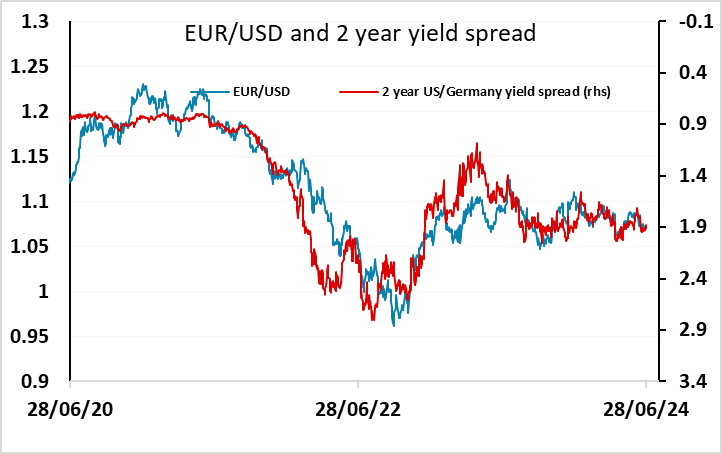

The US employment report and the French and UK elections are the standout events for this week. The impact of the French elections is unlikely to be large, with the right wing RN expected to be the largest party, followed by the left alliance and the liberal coalition. But nothing will be really decided until the second round of voting on July 7. Even then, most expect a messy result which makes it impossible for any coalition to form a government. For now, the impact on the EUR is likely to be small, with EUR/USD still stuck close to 1.07. An unexpectedly large win for RN that suggests they might be able to form a government would be EUR negative, but otherwise expect little impact.

French election polls

The UK election is similarly relatively predictable. It would be a huge surprise if there was anything other than a victory for the Labour Party. However, there is a lot of uncertainty about the size of the victory and whether there will be big gains for the Liberal Democrats or Reform parties at the expense of the ruling Conservatives. There is even a possibility that the Conservatives win fewer seats than the Liberal Democrats. The market would probably prefer the Labour victory not to be too large, in order to discourage excessively left wing policies in the future, but there is little danger of anything too radical in the short run. GBP may there gain a marginal benefit from a moderate Labour victory, and might suffer if the victory is too large, but the impact is unlikely to be dramatic.

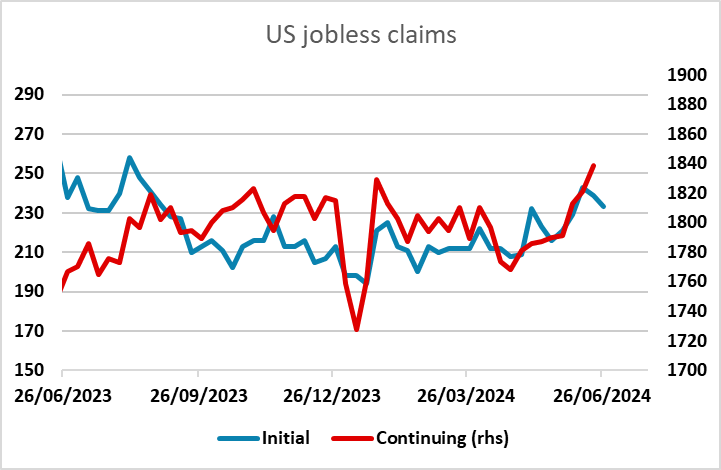

The US employment report has more potential for market impact. The recent US data has erred on the soft side, and there has been a particularly noticeable pick-up in jobless claims, including the claims data for the week of the payroll survey. Our forecasts for the employment report are essentially in line with the market consensus, so we are not anticipating a big reaction. But there is scope for a USD move in either direction. The average hourly earnings data is possibly the most important part of the report for Fed policy, but the initial reaction is likely to be to the payroll number. Given the recent rise in claims, the risks to our forecast and the consensus may be on the downside, and therefore also on the downside for the USD and US rates.

While all these events could have an impact, the greatest potential for volatility is still in the JPY, given the recent significant losses, the speculation about possible BoJ intervention and the huge current JPY undervaluation. The lack of BoJ action thus far suggests that the Japanese authorities are hoping the market will correct itself without their help. There is certainly a strong fundamental case for a JPY recovery, but the market is not being driven much by fundamentals at this stage. Since the intervention in late April/early May, yield spreads have moved clearly in the JPY’s favour, but the JPY has nevertheless moved sharply lower. It’s currently a momentum and carry driven market, so unless we have a shock of some sort which undermines risk appetite, the trend is likely to remain your friend in the absence of BoJ action. Even so, in an event heavy and holiday shortened week we may see some short term stabilization ahead of the US employment report.

Data and events for the week ahead

USA

FOMC minutes on Wednesday and June’s non-farm payroll on Friday are the highlights of the US week ahead, while Fed’s Powell will speak on Tuesday. FOMC minutes are likely to show agreement that more evidence of inflation moving back to target is needed before easing and that policy is data-dependent, though we do not expect the tone to be hawkish. Fed’s Williams will speak on Wednesday and Friday.

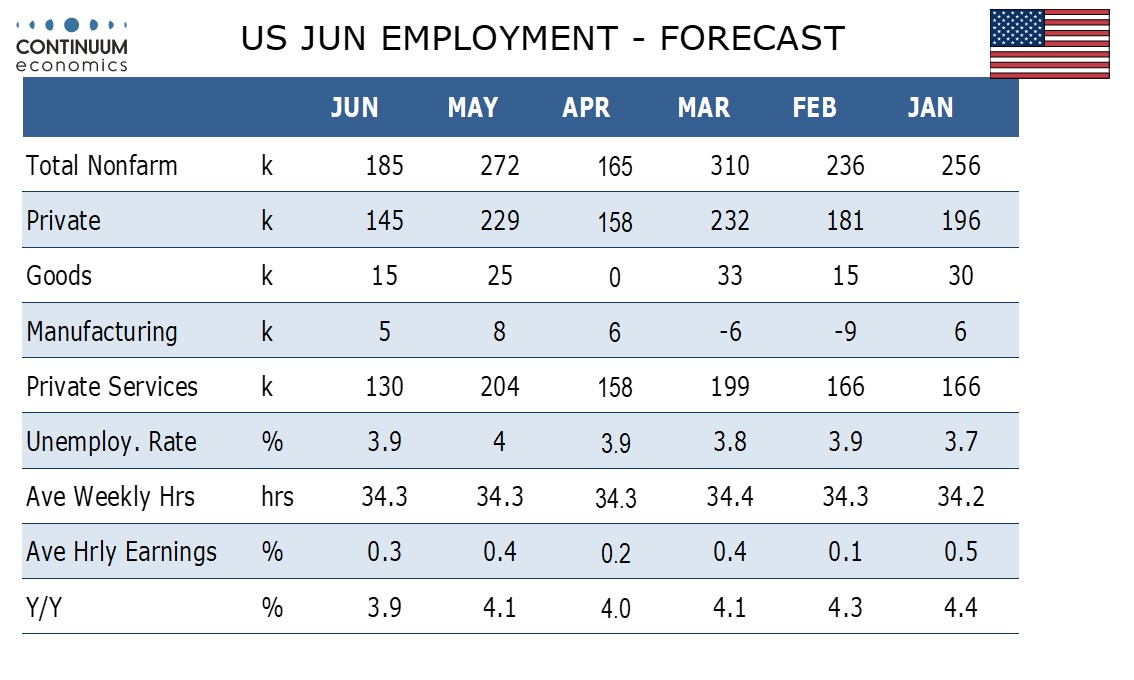

For the non-farm payroll we expect a slower 185k increase, with 145k in the private sector, and a moderate 0.3% increase in average hourly earnings. We do however expect a correction lower in unemployment, to 3.9% from 4.0%. We expect Wednesday’s ADP estimate of private sector employment growth to rise by 125k, underperforming private sector non-farm payrolls as has been the case in most recent months. Other labor market signals will come from May’s JOLTS report on job openings on Tuesday and weekly initial claims, which will be released on Wednesday due to Thursday seeing the Independence Day holiday.

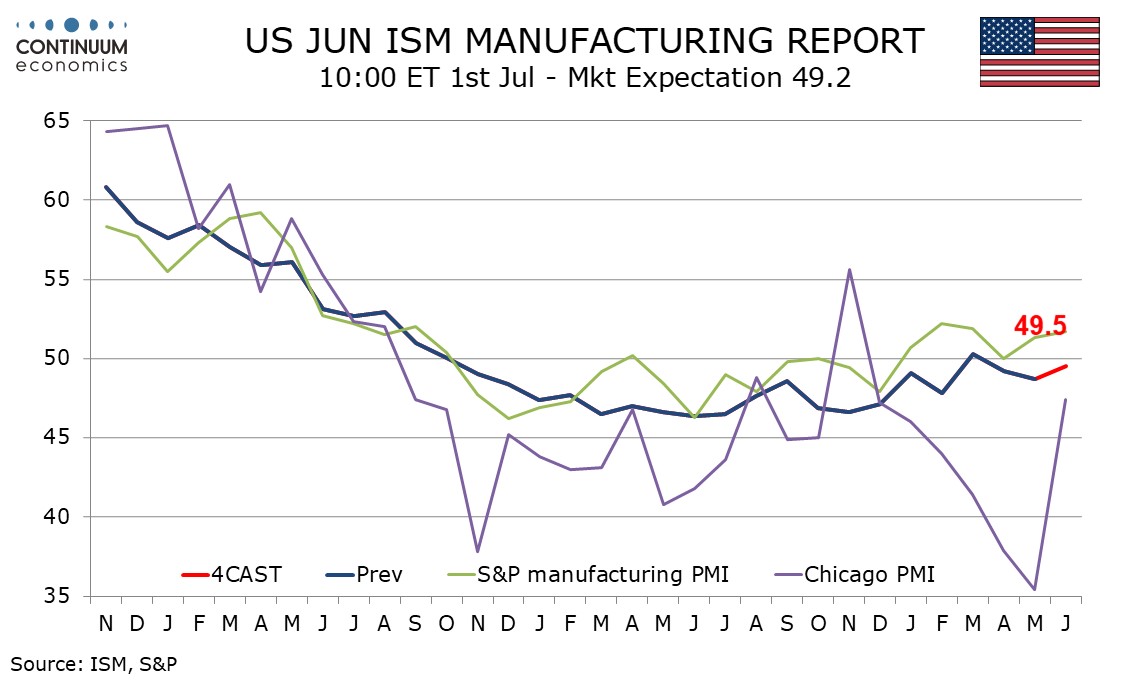

For June’s ISM surveys, we expect manufacturing on Monday to rise to 49.5 from 48.7 and services on Wednesday to correct lower to 53.0 from 53.8. Monday also sees May construction spending. On Wednesday we expect May’s trade deficit to increase to a 23-month high of $77.0bn from $74.6bn. May factory orders are also due.

Canada

Canada’s data highlight is June employment on Friday. May’s trade balance is due on Wednesday. June PMIs are also due, S and P manufacturing on Tuesday, S and P services on Thursday and Ivey manufacturing on Friday.

UK

An election-dominated week begins on Monday with fresh BoE-compiled money and credit data that may be of increasing importance. Firstly, they will show the extent to which cash-strapped households are still turning to borrowing to fund everyday spending. Secondly, they will highlight how BoE balance sheet reduction is having a wider impact, given the drop in bank deposits that has occurred of late, the question being to what extent is this adding to downward pressure on private sector credit. The BoE also releases survey data from its so-called Decision Makers (Thu).

Also on Thursday comes the BoE Credit Conditions Survey. It will help assess how the recovery is faring, not least in the housing market. Three months ago it pointed to the availability of secured credit to households having increased albeit this came, however, alongside no material change in credit supply for either unsecured lending or on the company side. What was also evident however, was a marked ump in demand for secured lending for house purchase and re-mortgaging increased in Q1, and both were expected to increase in Q2. But the general election result dominates the week this due with exit polls from 10 pm (BST) on Thursday and where a conclusive Labour victory is very likely

Eurozone

Datawise, it is a very busy week for high-profile survey numbers and inflation updates. Indeed, HICP data for the EZ arrives on Tuesday. This June data may be more reassuring, with the headline rate possibly hitting a new cycle-low of 2.3% (rounding effects could also mean the rate merely drops to 2.4% and thus merely reverses the May rise). Within this, services inflation may drop afresh but only 0.2-0.3 ppt but the core should fall 0.2 ppt and even possibly also instead hit a cycle low of 2.6%. German HICP arrives the day before; headline inflation is seen moving back down to 2.6% but with a similar-sized fall for core reading

Datawise, but more weak retail sales (Fri) and PPI (Wed) numbers may be followed by more construction sector weakness in the sector PMI numbers, these coming on Thursday, ie after final PMI survey data arrive (Mon/Wed). German industrial production (Fri) is likely to see perhaps a consolidation as may manufacturing orders numbers due a day earlier.

There is much ECB wise. Not only is there the minutes/account of this month’s rate-cutting Council meeting but there is also the annual and often-influential central banking conference in Sintra (Mon to Wed). This will include appearances from ECB Lagarde, Lane and Fed Chair Powell.

Rest of Western Europe

There are key events in Sweden, with (expected to be weak) monthly GDP indicator data (Fri) and the minutes to this month’s Riksbank meeting (Wed) likely to confirm the message from the m/m GDP indicator, albeit the latter plagued with volatility and revisions. Switzerland sees CPI data (Thu) with a stable 1.4% headline reading envisaged and a result consistent with SNB thinking.

Japan

Little critical economics release for Japan next week. Overall household spending on Friday may carry the most weight as it indicates the situation of domestic consumption. A positive figure would support our central forecast. We also have the manufacturing index on Monday and PMI on Wednesday.

Australia

We have a slate of Australian data on Wednesday. Retail sales and private inflation survey would be market moving while PMIs and Building permits may affect sentiment less. The RBA meeting minutes on Tuesday maybe a non-event and Trade balance on Thursday would instead be more insightful.

NZ

Business confidence and Building Permits on Tuesday, GDT Price Index will also be released within the week.