German Data Preview (Jul 1): Inflation Moves Back Down And Broadly So?

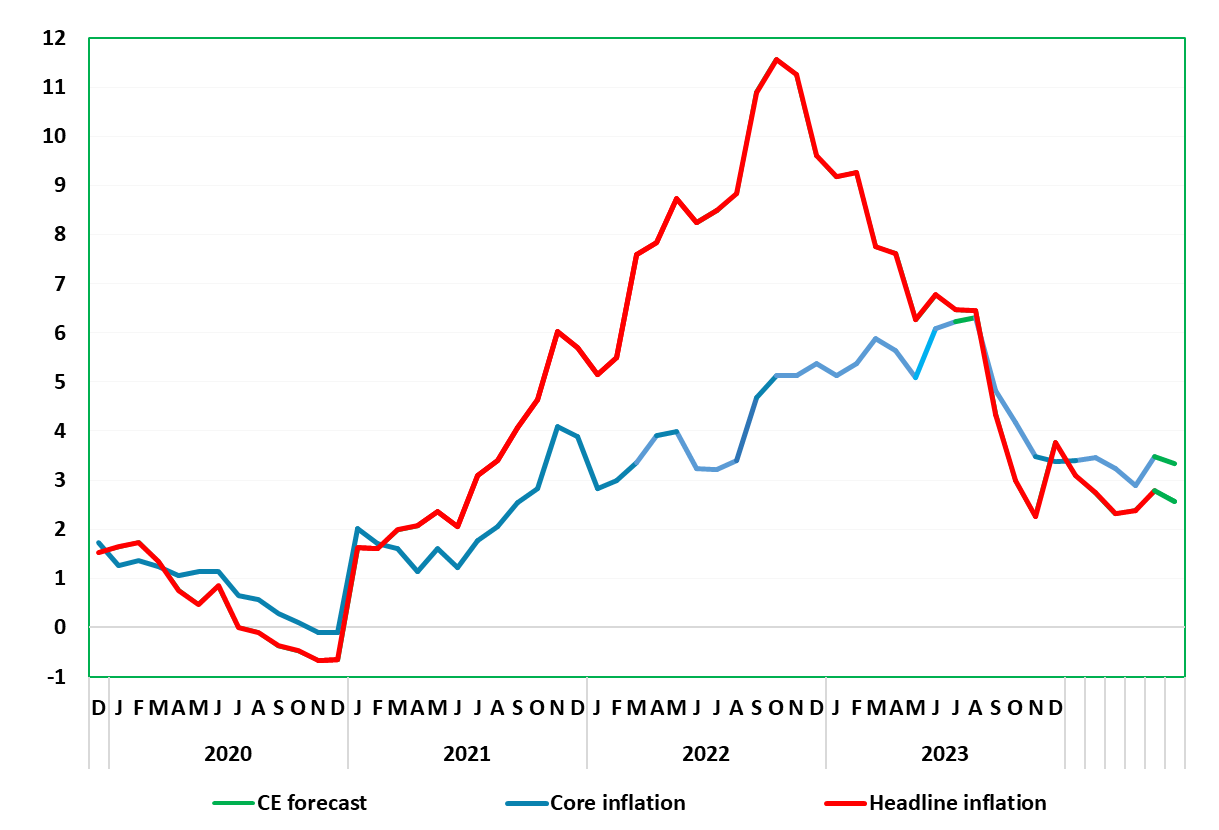

As we have repeatedly underlined, base effects continue to distort the German HICP/CPI readings and the path down for inflation has not been smooth. This was even more clearly the case in the May numbers where a second successive and slightly larger rise in the headline HICP rate occurred rising 0.4 ppt to 2.8%, albeit a rise half that size seen in the accompanying CPI data. There was an even larger jump in core, also based around base effects within transport services. But as petrol prices have started to fall afresh and with no adverse base effects, headline inflation is seen moving back down to 2.6% but with a similar-sized fall for core reading (Figure 1) but with with the adjusted core having risen back above circa-target strength (Figure 2), something we regard more as noise than fresh trend.

Figure 1: Inflation Still Bumpy?

Figure 1: Inflation Still Bumpy?

Source: German Federal Stats Office, CE

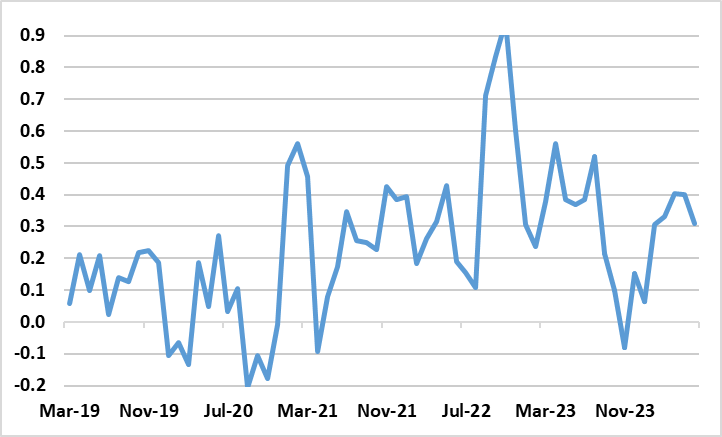

It is unclear to what extent recent services price resilience is due to distortion caused by the early Easter and recent fiscal developments as well as adverse base effects. But adjusted m/m readings for recent months and even our June projection suggest that core rate disinflation may have stalled, albeit at a pace still down from previous rates and largely consistent with 2% target (Figure 2).

As for those May details, consumer price inflation was pushed up despite a fall in road fuel prices. In contrast, transport service costs had a boosting effect. Further rises in fuel costs beckon for June data, where headline inflation is likely to fall to at least 2.6% and where the general downtrend seen of late should therefore have resumed, with the headline dipping below 2% in late Q3. NB: according to the Bundesbank, the rate was envisaged jumping back to around 3 % in May, the central bank seeing the headline moving sideways in coming months

Figure 2: Adjusted Core Rate No Longer Falling?

Source: German Federal Stats Office, CE