USD flows: USD lower after weaker than expected April CPI

US CPI 0.1% below consensus, USD has scope for extended decline

US CPI comes in 0.1% softer than expected in both headline and core, at flat and 0.2% respectively. While this won’t change the fact that the FOMC dots tonight are likely to be more hawkish than March, it improves the odds that the median FOMC view will be for two rather than one rate cut this year. This is still less than the three cuts envisioned in March, but more than the market currently has priced in. Pre-data, there were around 38bps of easing priced for this year, and post-data there are now 50bps of cuts priced, with the US 2 year yield dropping 13bps to 4.70%. This may be a slight overreaction to the data, but the numbers are clearly USD negative.

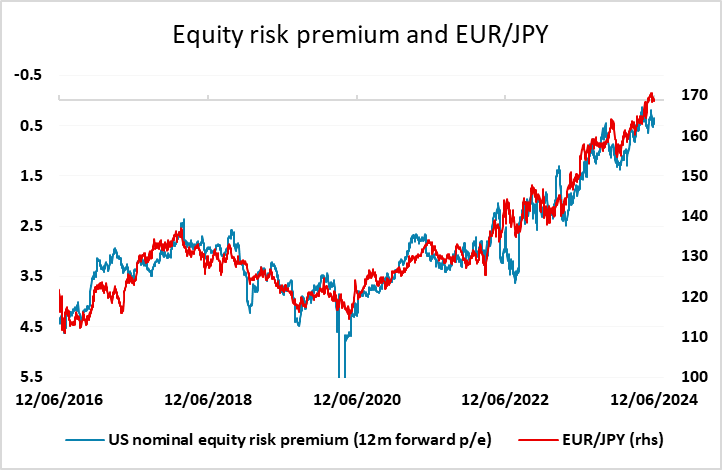

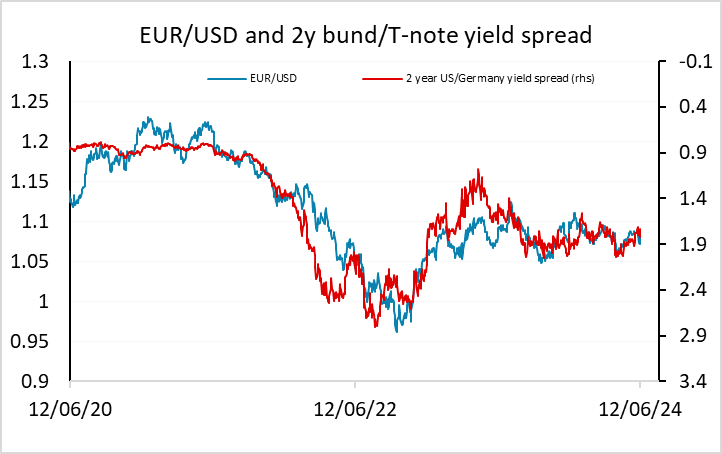

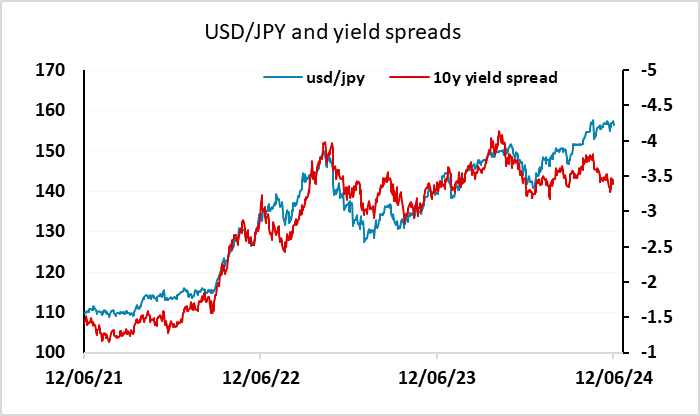

Both EUR/USD and USD/JPY were already underperforming historic correlations with yield spreads before the data. The EUR underperformance has been in place since the French election announcement, while the JPY underperformance is more longstanding and appears to be related to carry trade enthusiasm encouraged by risk positive sentiment. The decline in US yields supports USD losses across the board, and the initial rise in equities after the data suggests that some of the more risk positive currencies can outperform. The AUD has initially been the best performer, and this may be maintained in the short term. But the JPY is likely to catch up as JPY crosses tend to be correlated to equity risk premia rather than equity prices themselves, so that a rise in US equities triggered by yield declines is often positive for the JPY on the crosses as well as against the USD. Even though the FOMC dots are likely to be more hawkish than March, the data does suggests there is potential for more USD downside than we have seen initially, particularly against the JPY.