FX Daily Strategy: N America, June 11th

Market awaiting FOMC

GBP slips lower on UK labour market data

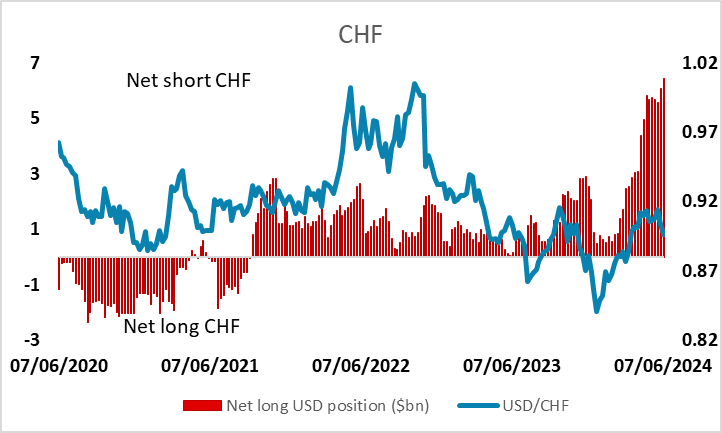

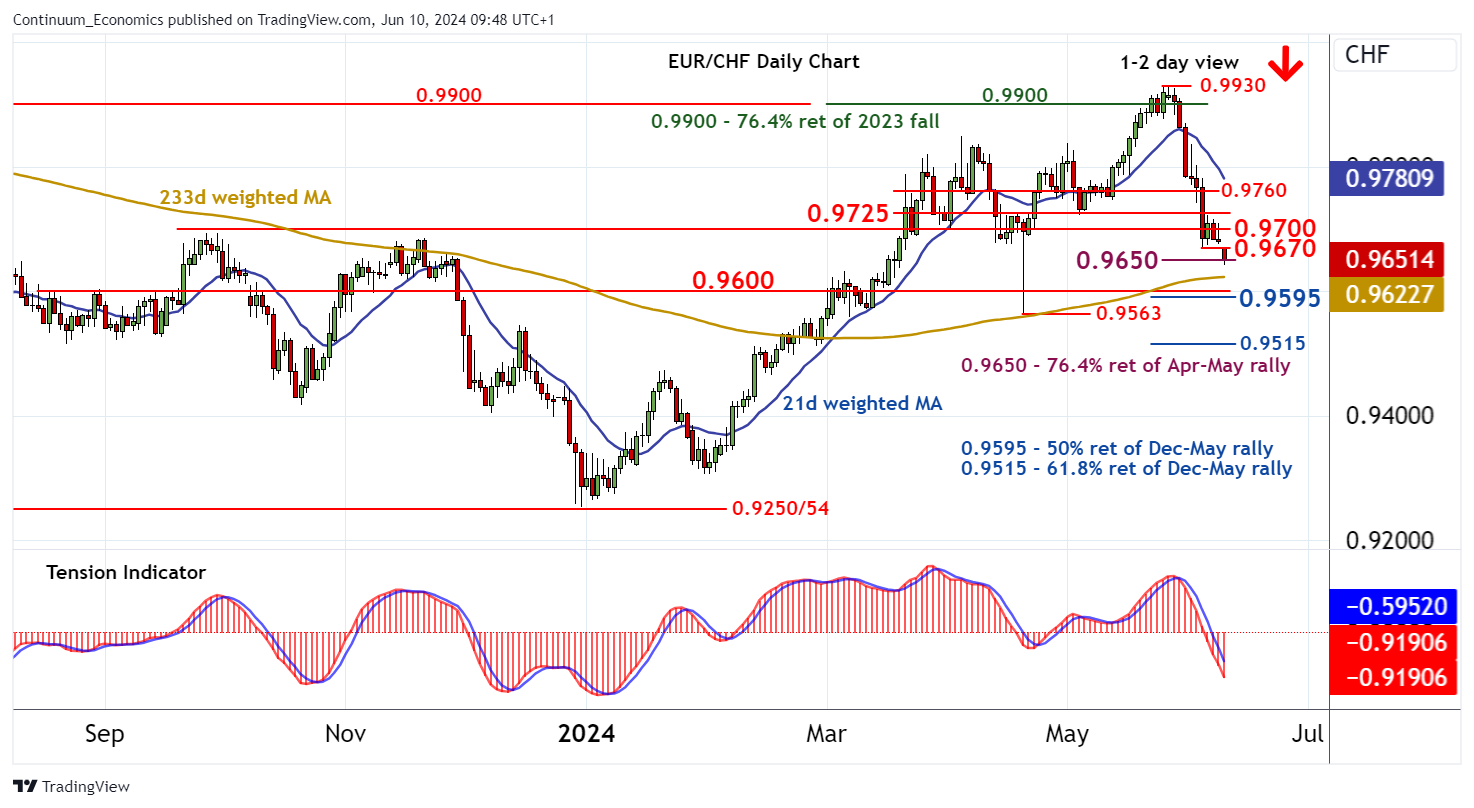

CHF strength may extend…

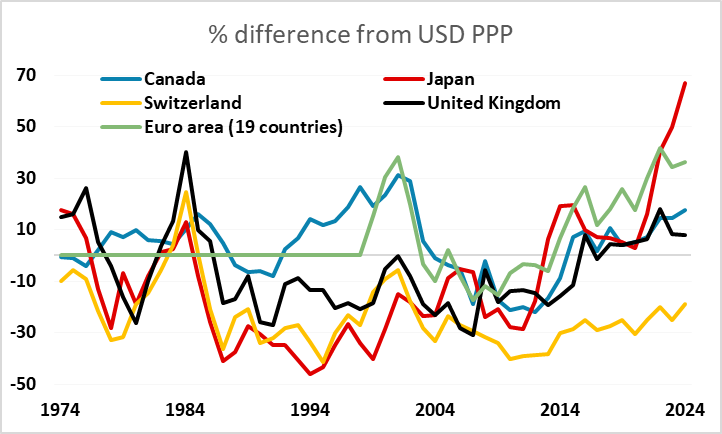

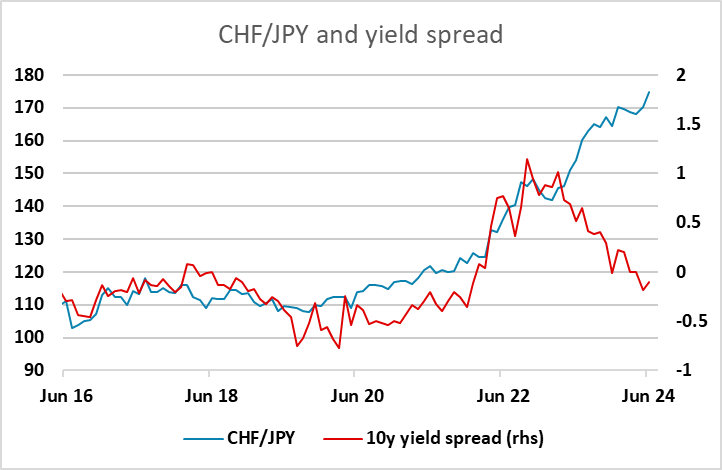

…but JPY remains much better value

Market awaiting FOMC

GBP slips lower on UK labour market data

CHF strength may extend…

…but JPY remains much better value

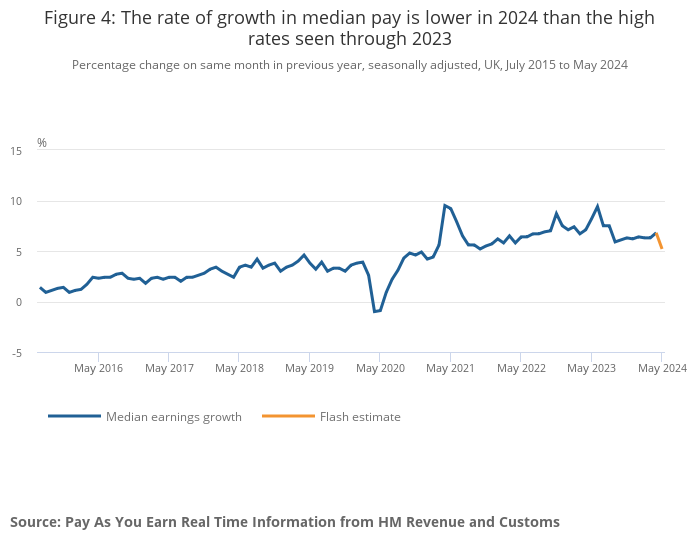

The FOMC meeting is the main event of the week, and the meeting starts on Tuesday, but the result won’t be announced until Wednesday so the market will need to find alternative stimuli before the Fed announcement, starting with the UK labour market data. UK labour market data was generally on the weak side, and GBP is slipping a little lower in response. Although the official ONS average earnings data shows a higher than expected growth rate of 5.9% y/y in the 3 months to April, the more up to data HMRC payroll data shows a decline in the y/y rate of growth to 5.2% in May. The employment measures are on the weak side, with a sharp rise in the May claimant count of 50.4k, the largest since February 2021, and a drop in employment of 140k in the 3 months to April on the ONS measure and a small 3k drop in the HMRC measure in May.

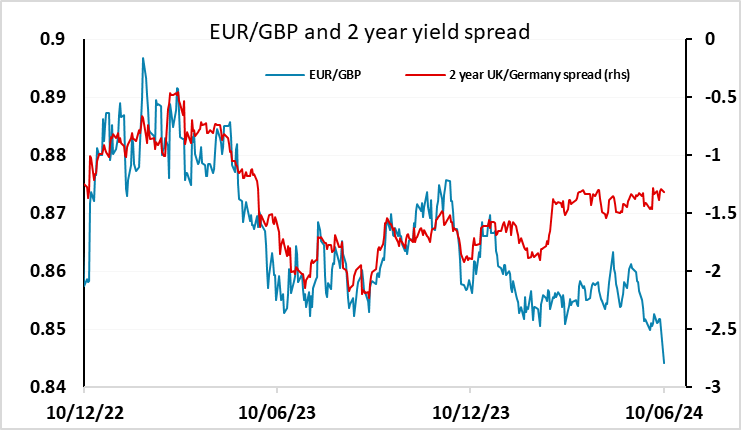

The data is nevertheless not weak enough to convince the BoE MPC to cut rates this month, after the slightly disappointing April CPI data. Although we have the May CPI data released next week just before the BoE meeting which could change sentiment, it is unlikely to be sufficiently weak to alter the June decision. However, today’s weak labour market data increases the chance of an August rate cut, which is currently priced as a less than 40% chance. EUR/GBP already looks a little low relative to yield spreads, and has dipped this week after the French election announcement as the EUR came under general pressure. But we doubt this will have a sustained impact, and see scope for a move up towards 0.85.

The EUR was generally soft in response to the French election news on Monday, falling back against the JPY and CHF as well as GBP. Declines against the safe havens may make more sense than declines against GBP, with yield spreads likely to move against the EUR against the safe havens in the coming months. The CHF also usually benefits from any widening in intra-Eurozone spreads, and we have seen some of that after the European elections and the French election announcement. It is also notable that speculative positioning is extremely short CHF according to the CFTC data, which suggests EUR/CHF is vulnerable to further declines if support at 0.9620 breaks.

However, while the CHF may benefit from some European political uncertainty, it continues to look overextended relative to the JPY, with CHF/JPY hitting a new all time high on Monday. This is more about JPY weakness than CHF strength, with the JPY hugely undervalued against all the major currencies, but the valuation issue is more obvious against the CHF as similar Swiss and Japanese inflation rates mean the nominal exchange rate has moved closely with the real exchange rate. This week’s BoJ meeting on Friday is not generally expected to produce any change in policy, but there are some hawkish voices and we suspect the market is underestimating the risks of another surprise BoJ move. In any case, the JPY continues to represent obvious long term value at these levels.

The USD made general gains after the employment report on Friday, and looks set to hang on to most of them into the FOMC meeting. The AUD may have better prospects for recovery than European currencies, as sentiment towards China has improved on late. The NAB business survey on Tuesday could trigger a move back above 0.66 if it shows sentiment improving.