ECB Preview (June 6): D-Day

Given the almost unanimous hints from Council members, something unexpected is needed to prevent the ECB from starting to cut its policy rates on June 6, most notably the key deposit rate currently at an unprecedented 4.0%. The question markets are considering is how/when this widely expected 25 bp cut will be followed by subsequent moves. Given splits within the ECB Council no formal guidance may be forthcoming at the press conference, save to underline that policy will be data dependent and independent of the likes of the Fed. But updated ECB forecasts are likely to corroborate market thinking of an ECB depo rate falling well below 3%, if not lower if an earlier and more sizeable undershoot of the inflation target is flagged. This would chime with ECB Chief Economist Lane’s thinking which suggest that on the basis of inflation moving durably to target as seen in 2025 would allow policy to veer away from restrictiveness and thus toward a neutral setting of circa-2%!

Figure 1: Little Change in the Economic Outlook?

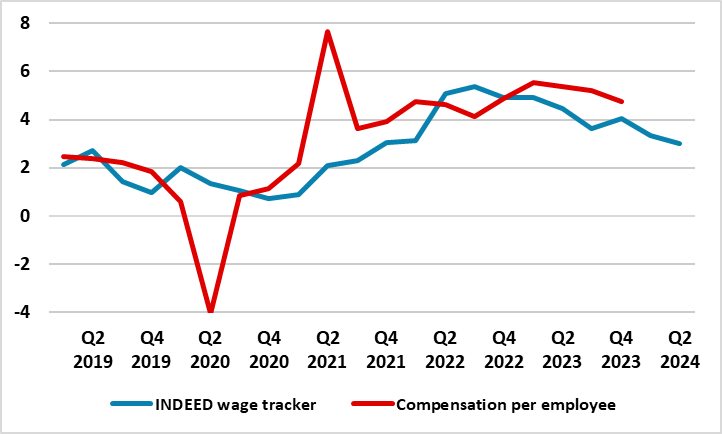

Even at its last meeting in April, the ECB Council made it clear that it is preparing to cut official rates, after what have been five successive stable policy decisions. It explicitly suggested that it could be appropriate to reduce the current level of monetary policy restriction, a policy hint backed up by dropping its previous rhetoric about ‘maintaining’ rates for sufficiently long time. Indeed, there was some dissent from a minority in favor of actual cuts at that particular juncture. Regardless, the path to a rate cut at the June 6 Council meeting and for some further easing beyond then is thus made clearer, as even a series of rate reduction would still leave policy restrictive. Equally unsurprising, the ECB is reluctant to plan out any particular path, insistent it is, and will remain, ‘data dependent’ most notably on labor costs data. But given existing projections already showing inflation below target by H2 next year (Figure 1) and with downside risks from the likes of the transmission mechanism, the bar is higher for such data to forestall a 25 bp cut next week. The key wage compensation data the ECB has been awaiting in revised Q1 national accounts numbers due officially on June 7 have already been effectively superseded by the likes of monthly wage tracking numbers which suggest such cost pressures have fallen to around 3% into early Q2 (Figure 2). This drop has exceeded ECB expectations and makes it more likely that still stubborn and wage sensitive service sector HICP inflation will fall further.

Earlier/Larger Inflation Undershoot More Likely?

We also feel that neither Fed policy, nor the US$, are likely to delay any ECB move(s). Perspective is needed. Despite the stronger US dollar, the EZ is not getting any competitive gain as the euro effective exchange rate is almost at record highs, partly a result of the weak yen, the net impact adding to tighter EZ financial conditions. Indeed, it has been noted that the tightening in financial conditions caused by higher bond yields ensuing from diluted Fed easing speculation may mean that the ECB has to cut short rates earlier or faster than otherwise.

Indeed, market rates have risen in recent months now being some 20 bp higher than those used to compile the March ECB projections. This is important as it implies that the updated projections the ECB will produce at the June meeting should not see any marked upgrade to the GDP picture save for a small upward revision to the path for this year after the better than expected Q1 figures. In fact, they may even be a softer growth outlook beyond this year, something seen in the recent European Commission projections, this due to a range of factors not least as fiscal policy assumptions may be more restrictive as well as tighter financial conditions. As a result, the inflation outlook that the ECB points to may see an earlier and/or more sizeable undershoot of the inflation target than the H2 schedule envisaged by the Council in March.

Possible Rate Cut Path

As is clear, the ECB seems very reluctant to discuss openly any possible rate cut path. But regardless, perhaps the main risk is that interest rates cuts may be larger and/or faster than we have assumed as the monetary policy transmission mechanism proves even more powerful than we have estimated reflecting a grudging and belated acknowledgement that the ECB balance sheet reduction is adding to tighter financial conditions. It is noteworthy that the ECB cites the transmission mechanism as a downside risk to its outlook and this risks continues, if not grows.

Balance Sheet Considerations.

In this regard the ECB has become ever more aware of a still very weak credit and bank deposit backdrop. This was accepted as far back as the March Council meeting where the account noted that a reduced supply of liquidity was also contributing to monetary tightening. Notably, this negative impact from its balance sheet reduction on credit dynamics was very much underscored in the last bank lending survey (BLS). Indeed, the BLS was explicit in highlighting that the shrinkage in the ECB monetary policy asset portfolio had a further negative impact on banks’ financing conditions and liquidity position, resulting in a moderate tightening of terms and conditions and a negative effect on lending volumes. This is something we have long argued was occurring and is evident in the unprecedented drop in bank deposits stemming from the ECB balance sheet reduction. This is all the more important as the ECB has no plans (yet) to slow, let alone stop, its unconventional tightening regardless of what and when its reduces official rates. It could be argued that if the ECB purses further balance sheet reduction, then larger/faster conventional easing may be needed! Alternatively, the ECB could slow the pace of APP QT later this year or early 2025.

Figure 2: Wage Cost Pressures Easing

Source: ECB, Indeed, Eurostat, % chg y/y

Policy Outlook

Regardless, we concur with ECB thinking that a good portion of recent disinflation is supply driven but, note with policy hikes still biting, the impact of weak demand will only accentuate this. This is implicitly accepted by the ECB as coming quarters would see the impact of past policy tightening continuing to be transmitted to bank funding conditions, broader financing conditions, credit volumes and the real economy’. But if the ECB remains focused on the labor costs updates, then as such numbers are produced quarterly, then subsequent rate cuts may only arrive in September and December. Hence, our long-standing view that the ECB may cut only some 75 bp this year. However, by year-end more durable evidence of labour costs easing should convince the ECB to continue easing and we see 100 bp further easing through 2025, with the deposit rate then nearing 2% and thus more in line with a perceived neutral setting!