German Data Preview (Apr 2): Inflation Drop to Continue Amid Less Resilient Services?

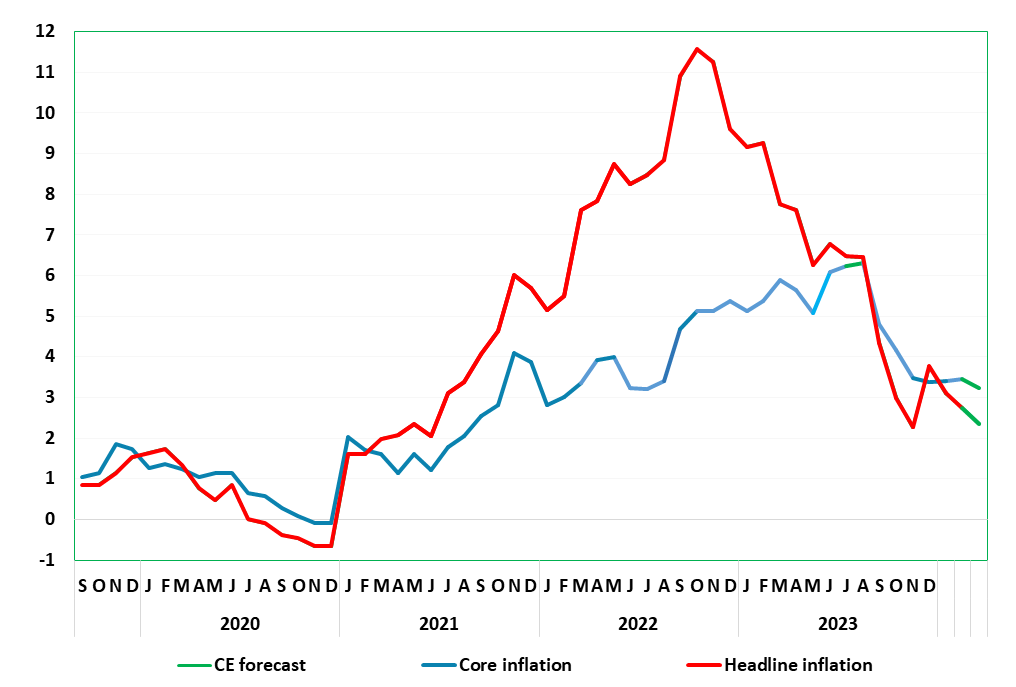

As we have repeatedly underlined, base effects continue to distort the German HICP/CPI readings, but the January data came in a notch below expectations, and reversed half of the surge in the y/y rate seen in December. And February data continued the downtrend, as the HICP rate fell from 3.1% to 2.7%, but with no further drop in the CPI core. We see a further and broader fall from 2.7% to a 33-month low of 2.4% in the March HICP data, dominated by a clear fall in food inflation, and a belated drop in services, both possibly held up somewhat by the earlier Easter this year. Energy will act as a boost to the headline, however. As a result, the core rate (not published in the preliminary reading should, nevertheless fall 0. 3ppt to 3.2%, a 21-month low. But adjusted m/m readings may once again suggest that disinflation may have stalled, albeit at a pace largely consistent with 2% target.

Figure 1: HICP Broadly Lower?

Source: German Federal Stats Office, CE

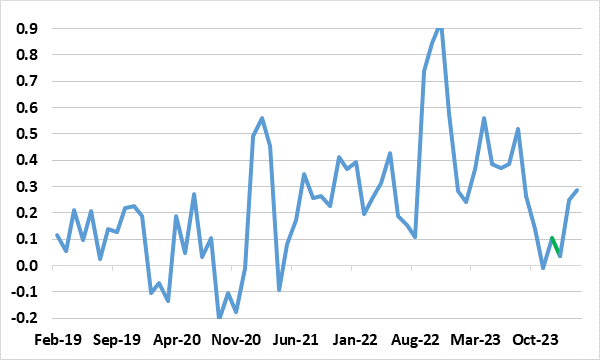

In February, the drop was purely based around lower food inflation while energy prices in February moved the other way while despite favourable base effects, there was seemingly continued momentum in services inflation, very probably a result of higher VAT being levied on restaurant meals in January still being passed on to consumers. Regardless, the disinflation backdrop is underlined by what may be still-soft core seasonally adjusted trend but which may be running just around 0.25% in m/m terms, up slightly in recent months (Figure 2). Regardless, services inflation may slow a little more clearly in y7/y terms in March and where this waning price momentum should see headline HICP below 2% by the autumn, albeit with some swings possibly accentuated by the earlier Easter this year and a little later than we were envisaging 2-3 month ago.

Figure 2: Adjusted Core Rate No Longer Falling?

Source: German Federal Stats Office, CE, seasonally adjusted % chg m/m, smoothed