Turkiye’s Inflation Roared Strong in January: Biggest Monthly Jump since August

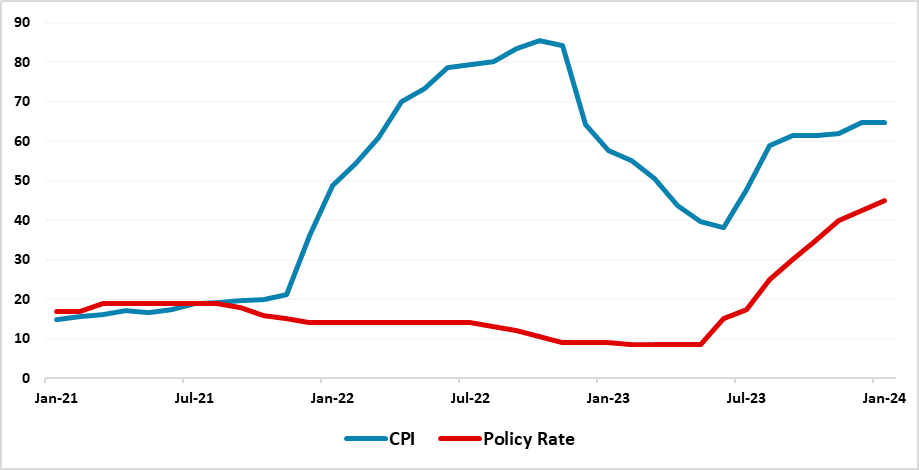

Bottom Line: Turkish Statistical Institute (TUIK) announced on February 5 that Turkish CPI surged to 64.9% annually and 6.7% monthly in January, which marked the biggest jump in the last five months, due to recent hikes in salaries and pensions, continued adverse impacts of deterioration in pricing behaviour, depreciating Turkish Lira (TRY) and strong inflation expectations. In January, producer prices also increased by 44.2% annually and 4.14% monthly, reaching a five-month peak. We feel upside risks such as weakening currency, elevated upward pressures in services, and hikes in public spending before the March local elections remain strong, which would likely drive the inflation in 1H of 2024, as the impacts of the strong monetary tightening are still feeding through.

Figure 1: CPI (YoY, % Change) and Policy Rate (%), January 2021 – January 2024

Source: TUIK, Datastream, Continuum Economics

When annual rate of changes (%) in the CPI’s main groups are examined in January, we see that clothing and footwear with 40.6% was the main group with the lowest annual increase while hotels, cafes and restaurants with 92.3% was the main group where the highest annual increase was realized. It is worth mentioning that education (79.8%), health (78.6%), and transportation (77.5%) also recorded remarkable YoY increases.

Core inflation (CPI-C) recorded a strong 7.58% MoM increase, scaling up to 70.48% on an annual basis as it improved in January. After domestic producer price index (PPI) hit 157.69% hike on annual basis in October 2022, domestic PPI stood at 4.14% MoM translating into 44.2% YoY in the first month of the year, reaching a five-month peak.

Speaking about the January inflation reading, Minister of Treasury and Finance Minister Simsek stated that "Starting from February, monthly inflation will decrease significantly, consistent with our forecast path. We will see a significant decline in annual inflation in the second half of the year. Ensuring price stability is our main priority."

In the meantime, one important development on the macroeconomic policy making front was the resignation of the Central Bank of Turkiye (CBRT) governor, Hafize Gaye Erkan, on February 3, who announced she was stepping down citing a major reputation assassination campaign launched against her. Fatih Karahan, who has been appointed as the new governor of the CBRT, underscored on February 4 that "The main objective and priority for the CBRT is to achieve price stability. We continue our efforts to ensure disinflation, and we are determined to maintain the necessary monetary tightness until inflation falls to levels consistent with our target. We closely follow inflation expectations and pricing behaviour, and we will definitely not allow any deterioration in the inflation outlook." (Note: We foresee that CBRT would continue with the conventional monetary policy framework that prioritizes the fight against inflation, -just like in Erkan’s era- taking into account that Karahan has been the deputy governor and MPC member in the last nine months. We do not think Erkan’s resignation will have a major negative impact over the markets).

According to the CBRT’s MPC statement on January 25, CBRT appeared to remain concerned about the strong course of domestic demand, the stickiness of services inflation, and geopolitical risks that keep inflation pressures.

Following the January inflation data, we are of the view that there are signs that inflation will continue to stay high in the first half of 2024, in line with CBRT’s inflation projections. (Note: CBRT forecasts that annual inflation will record 36% at the end of 2024 after rising to the 70-75% band towards the middle of the year). We think recent hikes in salaries and pensions, strong course of domestic demand, increases in raw material prices, weakening currency, strong inflation expectations and surges in public spending before the March local elections would likely continue to ignite general level of prices. Despite strong monetary tightening in force and lagged impacts of the tightening cycle are still feeding through, we still see upside risks to the inflation outlook.