FX Daily Strategy: N America, March 19th

BoJ kept rates unchanged

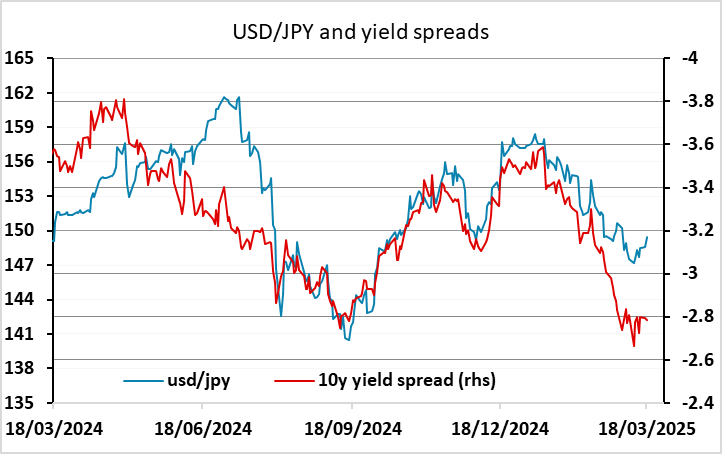

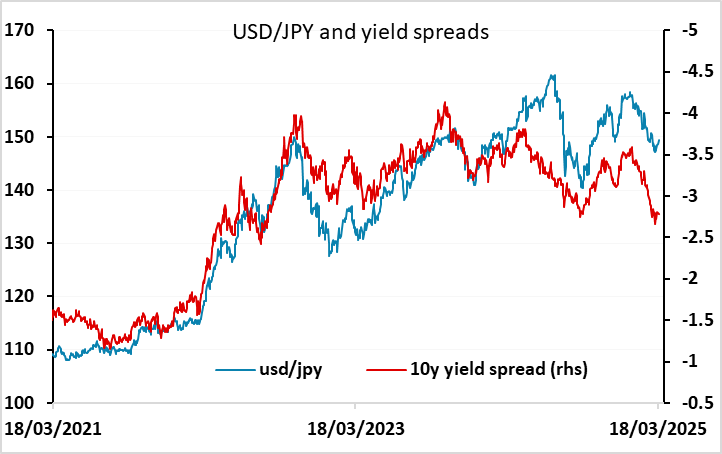

JPY can recover some recent lost ground

Fed to remain on hold given major uncertainties

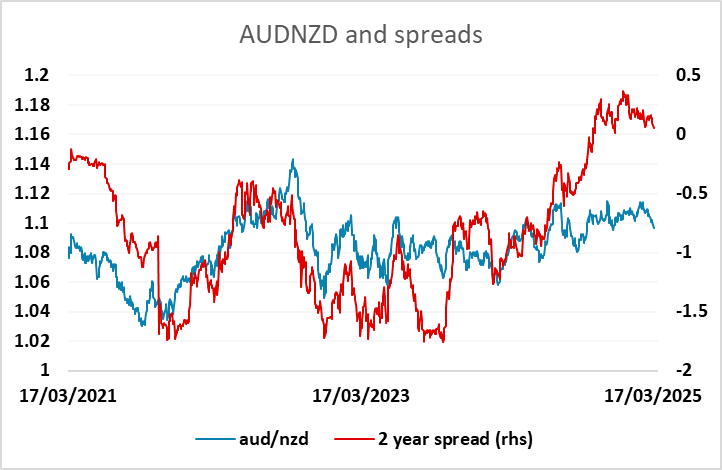

NZD may have downside risks against the AUD unless GDP is unexpectedly strong

BoJ kept rates unchanged

JPY can recover some recent lost ground

Fed to remain on hold given major uncertainties

NZD may have downside risks against the AUD unless GDP is unexpectedly strong

The BoJ left rates unchanged as expected at the meeting overnight, and Europe enters the market with BoJ governor Ueda’s press conference on the wires. Thus far, there hasn’t been a lot of market reaction, but USD/JPY slipped back slightly after breaching 150 briefly at the start of the press conference, helped by a general risk negative tone related to the sharp decline in the Turkish lira. The Japanese yield curve hasn’t moved significantly in response to the BoJ decision or Ueda’s comments, with around 30bps of tightening still priced in by year end and 5 bps for the May meeting.

If anything, we would see Ueda's comments as mildly hawkish, suggesting a May hike is rather more likely than the market is pricing in. He noted that short and medium term (real) yields are still in negative territory, and has said again that if things turn out as the BoJ forecast, they will be raising rates. While he notes a lot of uncertainty related to US tariffs, he indicates that wage awards are strong and at or above the expected levels, and that some on the BoJ had said that they needed to pay attention to price overshoot risks today. Against this, he also said the risk from falling behind the curve in monetary policy was not high, and that he wouldn’t raise rates when the economy was in bad shape, but he was optimistic about Q1 GDP. He noted that the impact of US tariffs will start to be felt in early April. and wage data was key to the next decision. This suggests that with the spring wage round underway, there should be a lot of key information available by the time of the next meeting in May.

USD/JPY is not much changed from yesterday’s levels, but we still see downside risks dominating. If US tariffs are damaging, rates will not be raised soon, but in that case the impact from tariffs will likely be global and will negatively impact risk sentiment, which will tend to benefit the JPY. The JPY may struggle more to make gains if risk appetite is strong, but in that case there is a higher probability of an early BoJ rate hike. So we see little JPY downside risk and 150 and 164 should be toppish in USD/JPY and EUR/JPY respectively.

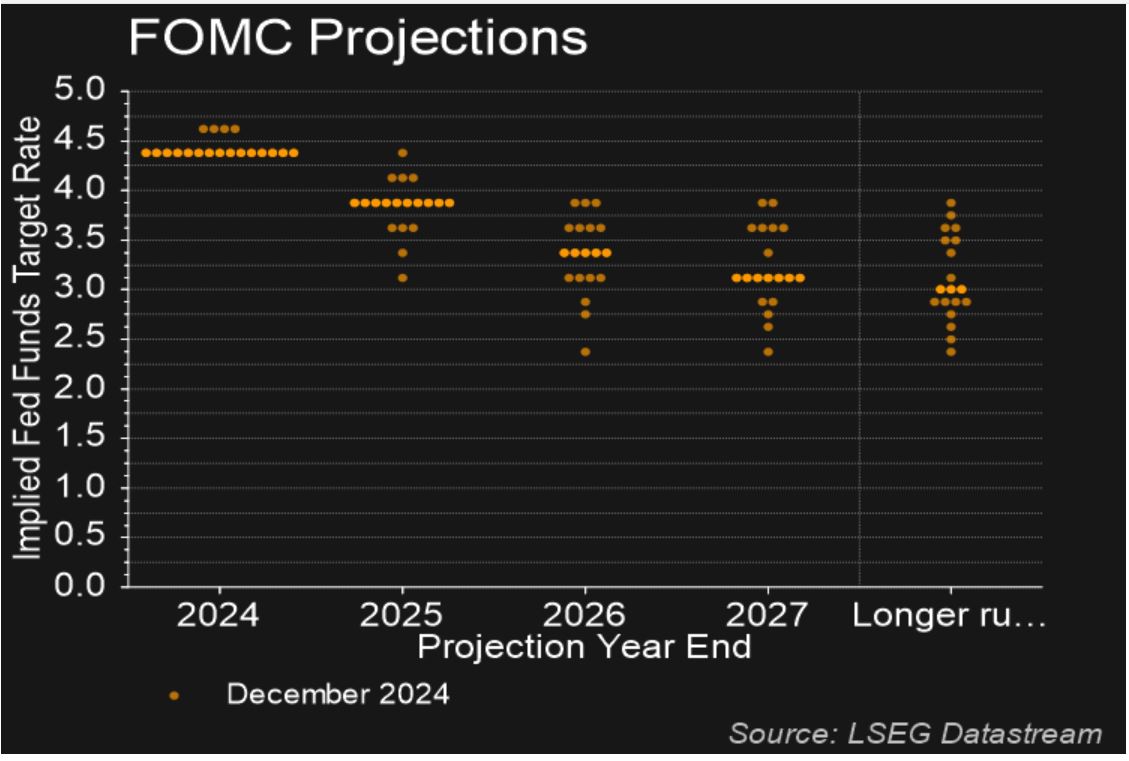

The FOMC meeting is the other main event of the day, but is similarly unlikely to deliver any change in policy. In the current exceptionally uncertain environment, the FOMC is also unlikely to give much away on future policy. The dots will be closely watched but we expect they will change little from January 29. Powell is likely to stress at the press conference that policy will be responsive to incoming data and the dots should not be seen as a plan. The January dots showed a median expectation of 2 more cuts this year, and the market is currently pricing in a further 59bps, so there is some marginal scope for US short term yields to rise on unchanged policy, but we doubt this will have much FX impact. There will be sensitivity to anything Powell has to say on tariffs and the impact on inflation and growth, but knowing this Powell can be expected to be very cagey.

Later on there is NZ Q4 GDP, which we expect will show positive growth, ending the recession seen in H2 2024. The RBNZ is still priced to cut another 50bps off rates this year, and this is likely to remain the case unless the data is exceptionally strong. However, we still see some downside risks against the AUD, which has underperformed relative to yield spreads and will benefit if we see more strength in Asian equities.