FX Daily Strategy: Asia, April 4th

ISM services survey could provide more negative news on the US economy

Trade data also likely to emphasise weakness in Q1 GDP

USD can weaken even in a risk negative environment

CHF CPI unlikely to have much impact, but CHF/JPY vulnerable

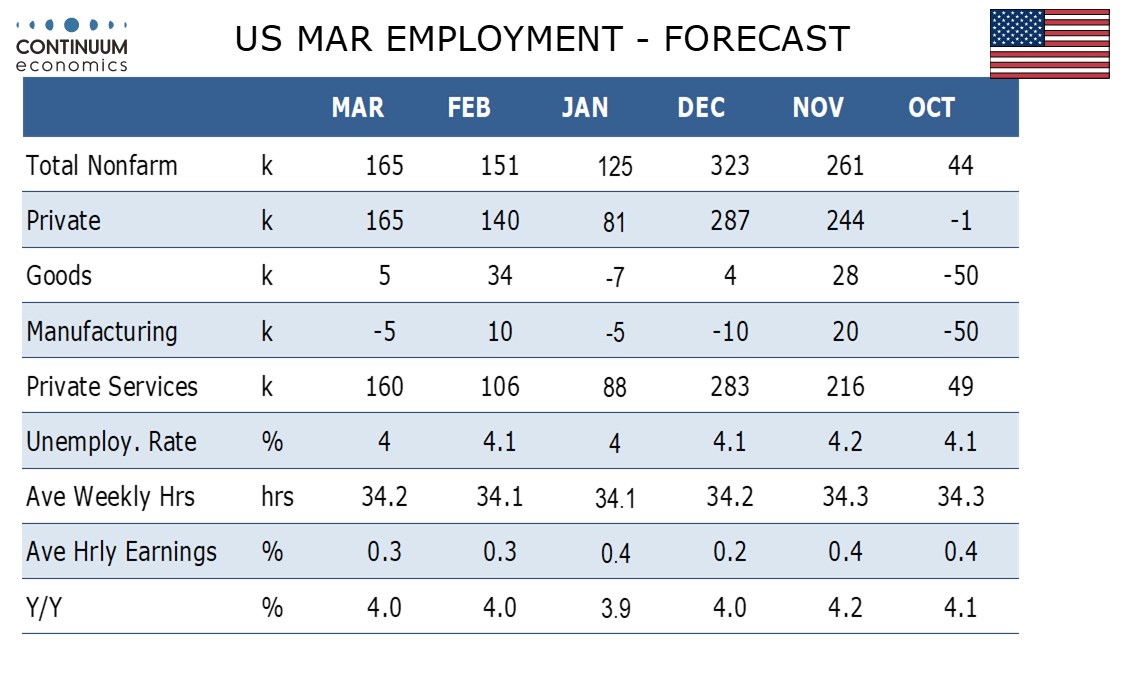

After all the fun of the tariffs, we have the US employment report to contend with on Friday. It looks quite unlikely that we will see any major change in recent trends, with the latest jobless claims numbers still very stable, and in any case the FX market is much more concerned with the implications of tariff policy than the minutiae of the current US labour market. For what it’s worth, we expect a 165k increase in March’s non-farm payroll, both overall and in the private sector, to show the labour market remains healthy despite growing downside economic risks. We expect the unemployment rate to slip to 4.0% from 4.1%, and an in line with trend 0.3% increase in average hourly earnings. Our forecast is modestly higher than the market consensus of a 137k increase in payrolls, and a 4.1% unemployment rate, so there may be some mild relief for the USD in response.

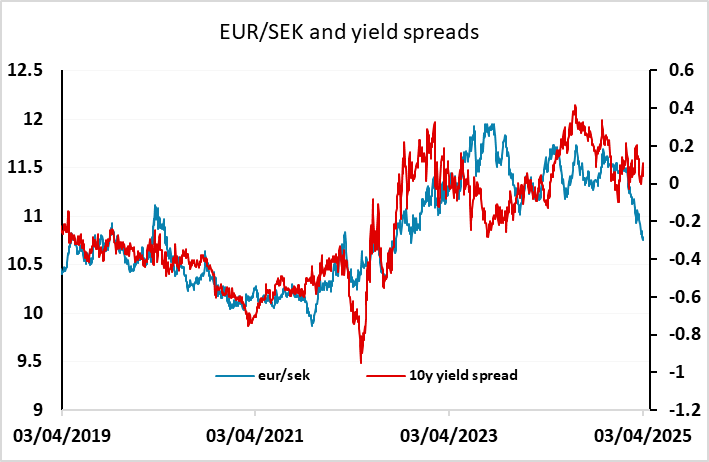

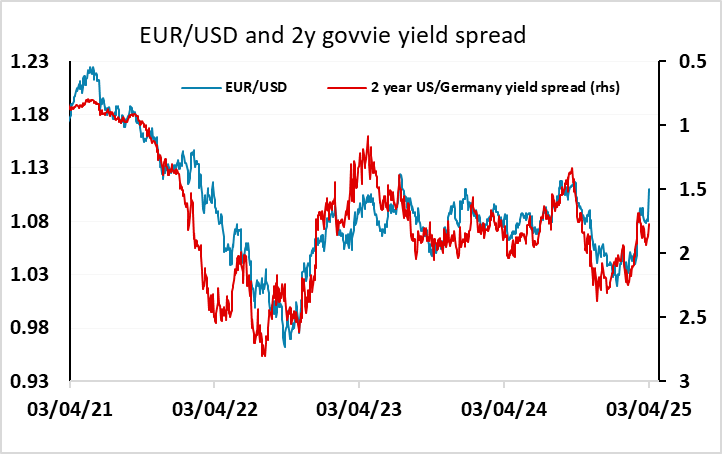

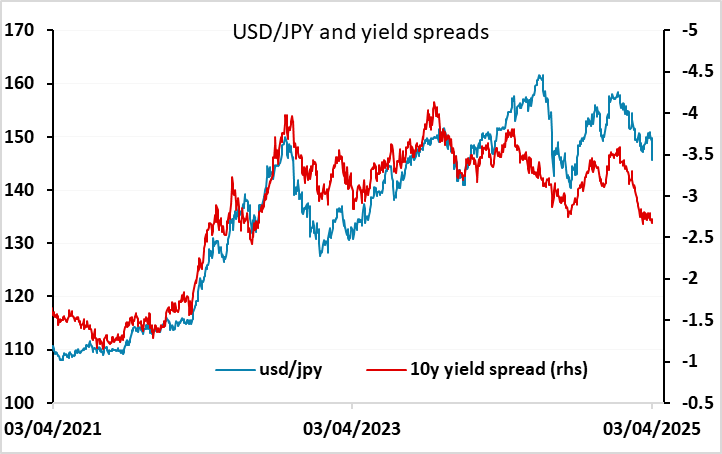

However, the March employment numbers are close to an irrelevance against the background of the tariff increase. The USD has weakened dramatically in the aftermath of the US tariff announcement, with the EUR benefiting as much as the JPY in spite of the decline in equities and yields which would normally favour the more risk negative currencies. While the riskier currencies have generally underperformed, the EUR has outperformed, reflecting its status as the USD’s anti-pole or an alternative reserve currency. Having said this, the SEK has even outperformed the EUR, so this may be mostly about all the currencies with low yields outperforming, in part because there is less downside for yields from here.

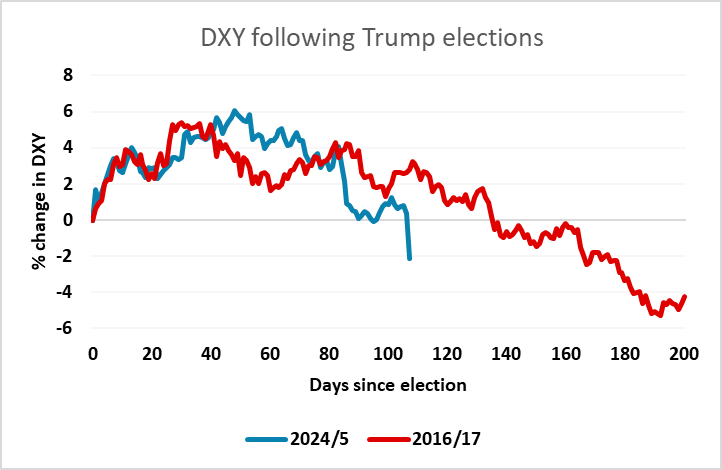

But the USD decline against the EUR is still much greater than a simple yield correlation suggests, while USD/JPY remains some distance above the level suggested by yield spreads. So this is not all about yield spreads, and there may be some shifting of reserves by central banks out of the USD taking place in response to the US tariff policy. From a big picture perspective this does look like something of a sea change for the USD, and to some extent mirrors what happened in the first Trump presidency, when initial USD strength gave way to dramatic USD weakness.

Ahead of the US employment report we have Swedish flash CPI data for March which is expected to show a decline to 2.6% from the 2.9% in February in the targeted CPIF measure. But FX reaction seems unlikely to be significant. In the current climate, lower yields are seen as an FX positive, so declining Swedish inflation will if anything add to the recent SEK strength. German orders data is also unlikely to be significant, although the EUR could suffer if we don’t see a recovery from the 7% decline seen in January.