FX Daily Strategy: N America, March 14th

UK January GDP weaker than expected

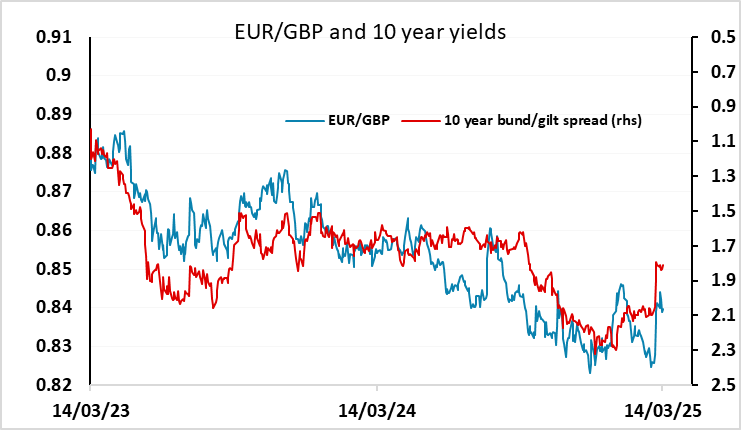

EUR/GBP risks mainly on the upside

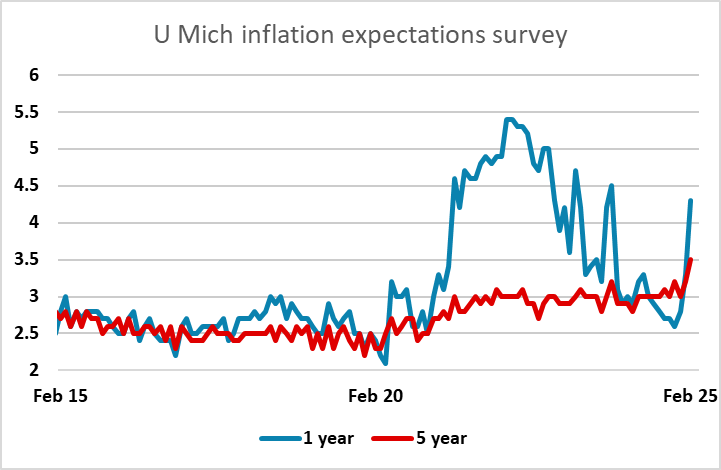

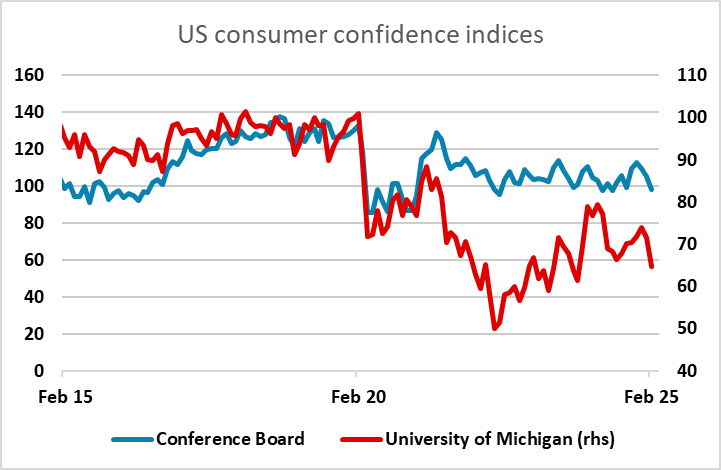

More focus than usual on University of Michigan confidence data

USD remains vulnerable to softer numbers, even if inflation expectations rise

UK January GDP weaker than expected

EUR/GBP risks mainly on the upside

More focus than usual on University of Michigan confidence data

USD remains vulnerable to softer numbers, even if inflation expectations rise

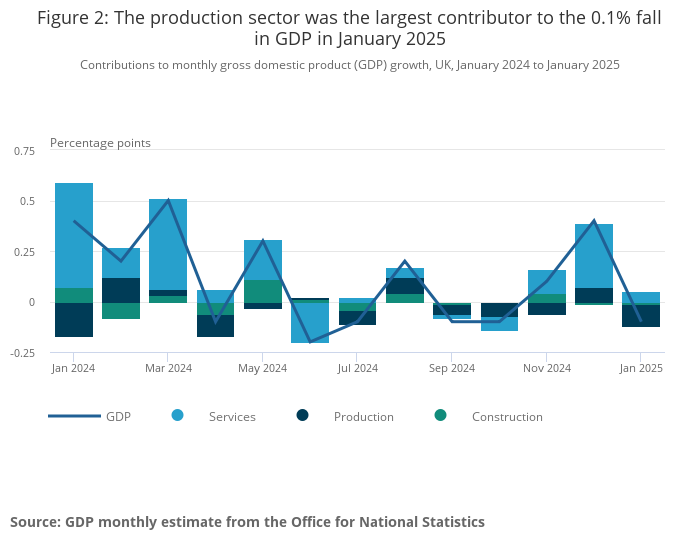

EUR/GBP gained 10 pips in early trade after weaker than expected January UK GDP data. This fell 0.1% m/m against a market consensus of a 0.1% gain, due mainly to a 0.9% decline in production. Services rose 0.1% and construction fell 0.2%. The picture is still not clearly weak, as the December gain of 0.4% means that Q1 is still likely to be positive, and on a 3m/3m basis GDP is still up 0.2% in January. Nevertheless, the data is on the soft side and with yield spreads already suggesting upside scope for EUR/GBP, a break back above 0.84 looks possible.

GBP has recovered slightly against the EUR in the last couple of days, helped by some expectations that the UK will be less affected by US tariffs than the EU. Even so, EUR/GBP has risen quite sharply in the last couple of weeks on the back of expectations of a boost to Eurozone spending on defence and infrastructure, which has pulled up Eurozone yields. Whether the rise in yield spreads is sustained will depend on how quickly the new spending comes on board and whether it will offset any drag to growth from the imposition of US tariffs. It is likely that the main impact of the new spending isn’t felt until 2026 and beyond, while the impact of tariffs on export demand could be felt more quickly. Nevertheless, EUR/GBP remains at quite low levels near 0.84, so there is scope for a move up towards 0.85.

The only US data of note is the University of Michigan consumer sentiment survey. This is not normally a major market mover, but takes on greater significance because of the current concerns about the US economy and the dips in confidence and rise in inflation expectations seen in recent months. The market consensus looks for some further decline in sentiment, which could trigger renewed USD losses after the stabilisation seen for much of this week. Higher inflation expectations have historically tended to be USD positive because of the expected Fed response, but with confidence slipping and the Fed potentially prepared to look through short term tariff related inflation increases and focus on demand and the labour market, higher inflation expectations are less likely to be USD favourable.

We continue to see USD/JPY as having the most potential for declines if we do see any further weakness in US confidence, with Japan looking out of step with most of the rest of the developed world in trying to manage increases in wages and a higher yield profile. But with the USD seeing less of tendency to benefit from weaker equities in recent weeks, softer US data could see the USD weaken across the board. We continue to see the AUD as having significant potential for gains if Asian equities prove resilient to any decline in the US markets.