FX Daily Strategy: APAC, Sep 24th

Japanese PMI could support rate hike expectations

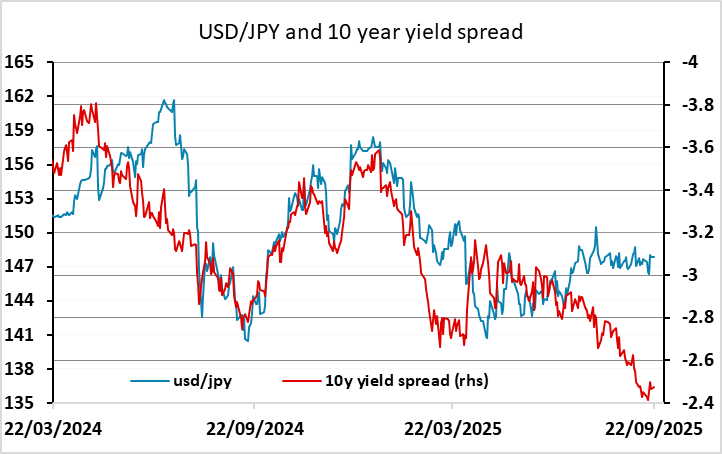

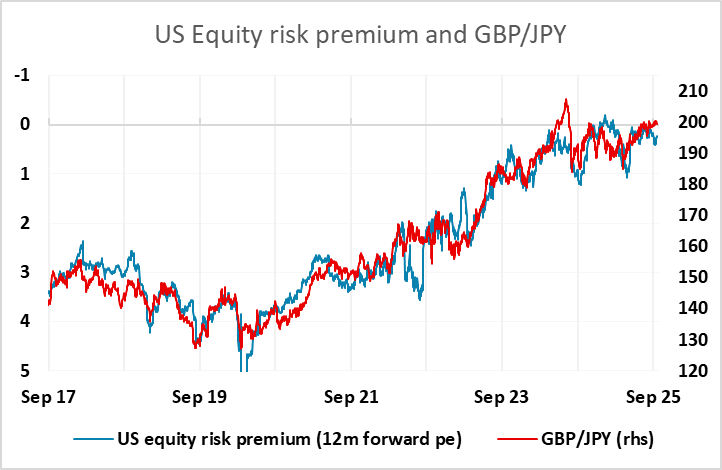

JPY continues to look substantially undervalued

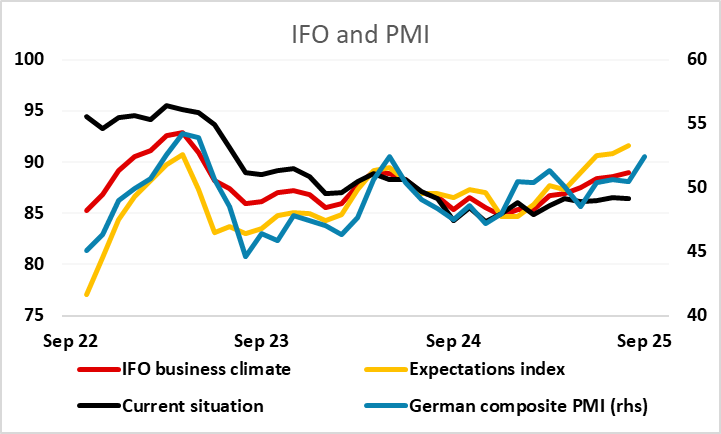

EUR might need above consensus IFO to hold current levels

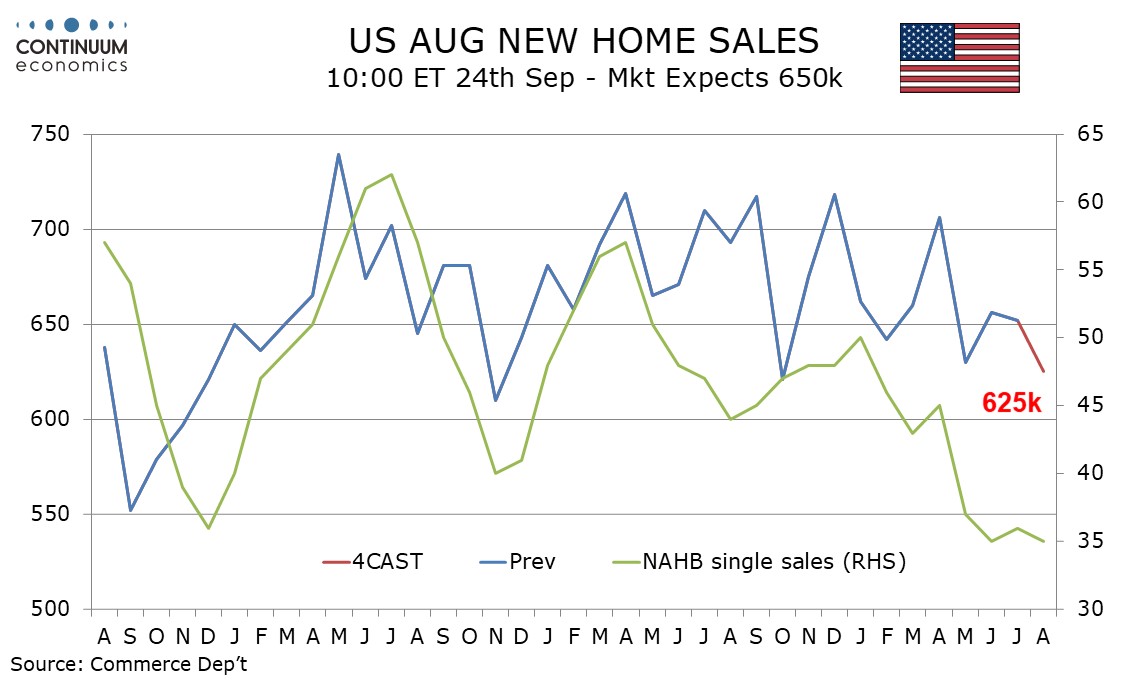

US home sales data could renew USD downside pressure

Japanese PMI could support rate hike expectations

JPY continues to look substantially undervalued

EUR might need above consensus IFO to hold current levels

US home sales data could renew USD downside pressure

Wednesday is a relatively quiet calendar. We start with the Japanese PMI data, delayed because of the Japanese holiday on Tuesday. While most take little notice of these numbers, there has been evidence of a modest improvement in the Japanese economy both in this data and in the GDP numbers this year, and another firm number will add to the chances that the BoJ will tighten policy in October.

USD/JPY remains extremely high from a fundamental perspective and also well above the level normally associated with the current level of yield spreads. Most of this is because of low risk premia and persistent equity market strength, but even on this basis the JPY is starting to look too low. The range could be broken if we see increased expectations of a BoJ rate hike in October. This is currently seen as slightly less than a 50-50 chance, but expectations of tighter policy could increase after the LDP choose a new leader on October 4th. The PMI data won’t affect this in the short term, but could be another plank in the BoJ’s case.

There is also the German IFO survey, following on from the German PMI data on Tuesday. There may be more interest in this than usual, as the German PMI moved sharply higher in September due to strength in services. The IFO business climate index has tended to move closely with the composite PMI in the last year or so, but if it fails to rise in line with the PMI (which would suggest an index above 90, well above the published consensus) the credibility of the PMI reading could be questioned. Without the strength in Germany, the Eurozone PMI would have been significantly weaker, so the EUR could edge lower even if the IFO index managed the modest rise to 89.3 suggested by the consensus.

In the US, we expect an August new home sales level of 625k, which would be a 4.1% decline if July’s 0.6% decline to 652k is unrevised. The level would be the lowest since October 2023. Trend has been fairly stable but the NAHB survey suggests there may be some near term downside risk. New home sales have shown surprising resilience since the NAHB homebuilder’s index saw a sharp dip in May. This resilience may be difficult to sustain in August but once Fed easing is seen the housing market is likely to find some support. Even so, weak data could renew downward pressure on US yields and the USD.