FX Daily Strategy: Asia, April 9th

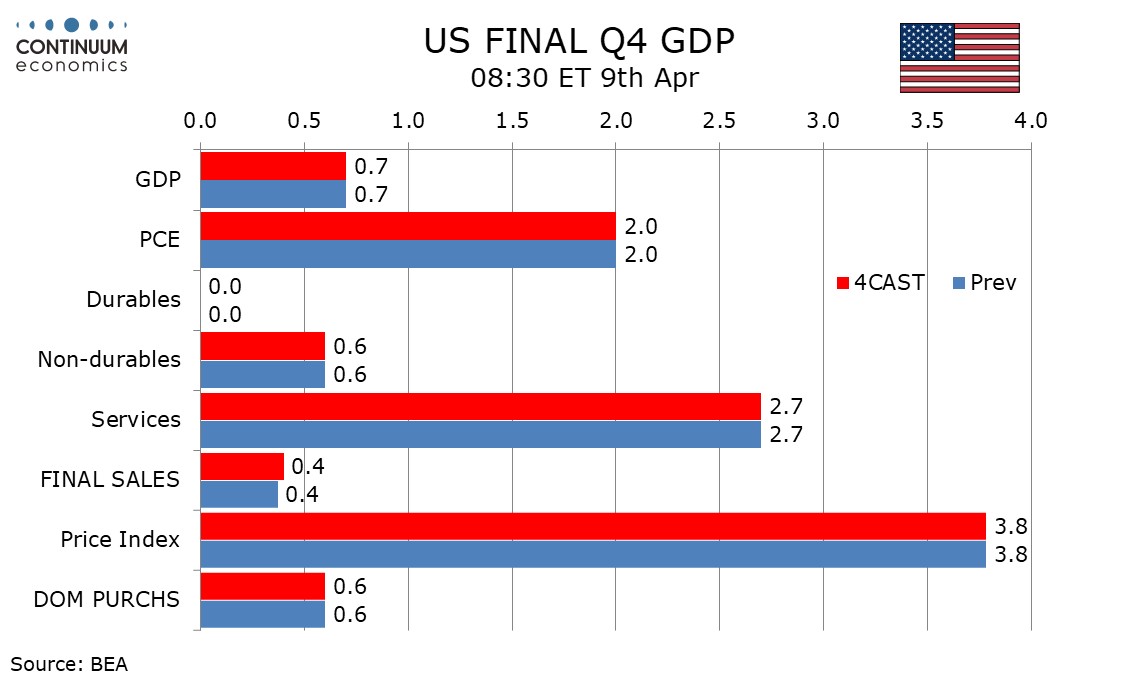

No significant revision for U.S. Final Estimate Q4 GDP

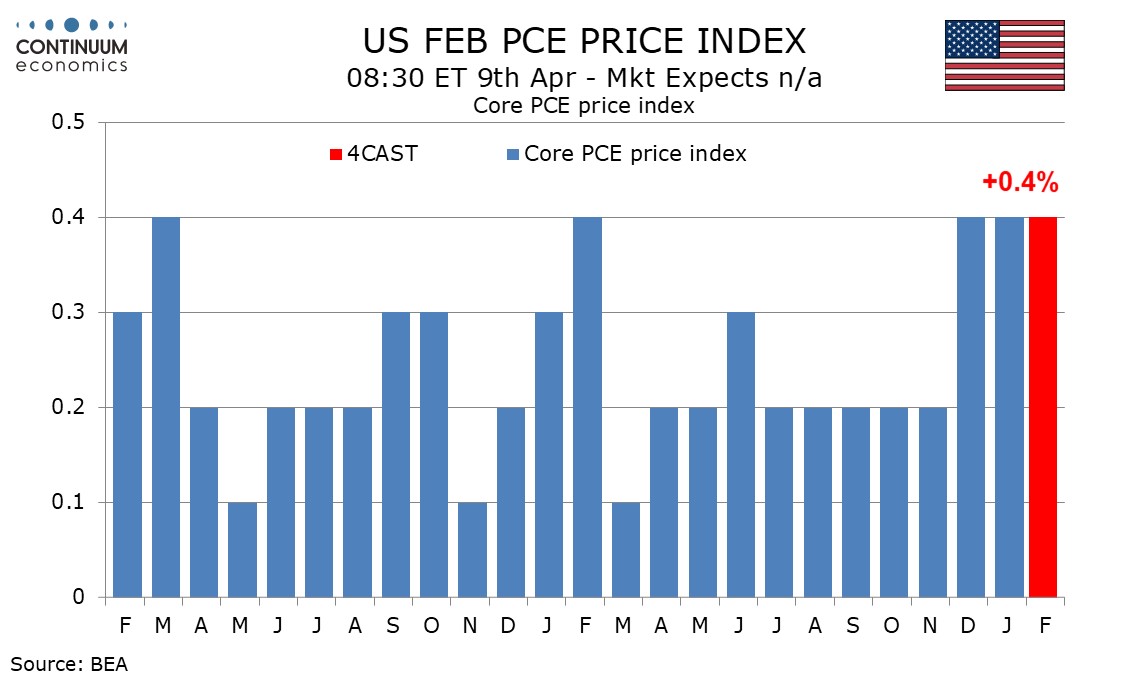

U.S. January Core PCE Prices to outperform CPI

DXY Tests Lower unless a Turn in Geopolitical Picture

We expect the final estimate of Q4 GDP to see no significant revisions, with marginal upward revisions to construction insufficient to lift the annualized gain from the preliminary 0.7%. Construction is likely to see a marginal upward investment to non-residential structures and a slightly larger upward revision to state and local government, though government will remain as a significant negative due to the federal shutdown. Elsewhere we expect no significant revisions.

We also do not expect any revisions to the price indices, of 3.8% for GDP, 2.9% for PCE and 2.7% for core PCE. The overall price index was led higher by government, which may also have been impacted by the shutdown.

We expect February to see a third straight strong 0.4% increase in core PCE prices, while personal spending with a 0.6% increase outperforms a 0.3% rise in personal income. This will see a January bounce in savings corrected. February CPI increased by 0.3% with the core rate ex food and energy up by only 0.2%. However the components of PPI that contribute to core PCE prices were mostly strong, and that is likely to keep core PCE prices elevated in February.

The USD has crashed lower on the two week ceasefire deal. The improving risk sentiment erode the haven base for the greenback. While it will likely be a choppy way to achieve some kind of peace, it looks likely DXY is southbound.

On the chart, prices consolidate the break above 100.00. Intraday studies are rising, suggesting room for a retest of congestion highs around 100.30. But mixed/negative daily readings should limit any initial tests in fresh consolidation, before improving longer-term charts prompt a break and open up a test of strong resistance at the 100.64 current year high of 31 March. Meanwhile, any immediate tests below congestion support at 100.00 should meet renewed buying interest towards further congestion around 99.50.