FX Daily Strategy: Asia, April 21th

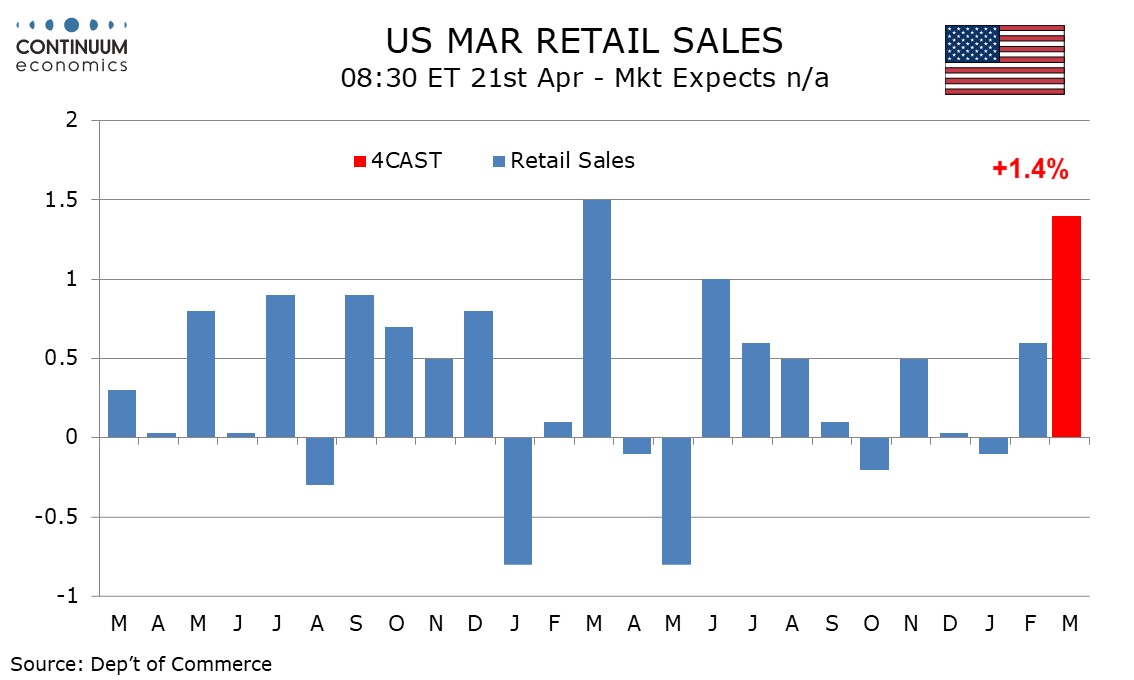

U.S. March Retail Sales Show Surge on gasoline prices

Geopolitics Favor DXY in a Short Term

NZ Q1 CPI May Further Tilt the RBNZ

We expect March retail sales to surge by 1.4% largely on surging gasoline prices, with sales ex auto and gasoline even stronger at 1.6%. Ex autos and gasoline we expect a rise of only 0.2%, on the weak side of a trend that has recently lost momentum. Most of the rise in sales will come from a surge in gasoline prices. Industry data suggests a rise in auto sales, we expect by 0.7% after a 1.2% increase in February, but this will not match the ex-auto increase, leaving overall sales underperforming the ex-auto gains.

Resilient auto sales suggest consumers did not immediately cut down on other items in response to higher gasoline prices but should the gasoline price rise persist, downside risks will build in Q2. A 0.2% increase ex autos and gasoline would be in line with what has been a subdued trend over the last six months. Higher tax refunds than seen at this time in 2025 may provide some offset to the hit to real disposable income coming from higher gasoline prices.

Geopolitical uncertainty continues to benefit the USD in a short run. Haven demand for the USD remain strong as the back and forth negotiation kept market participants on their toes, restraining their to turn cash into risk asset.

On the chart, the anticipated break below 98.00 has bounced smartly from above support at 97.50, as intraday studies turn higher, with prices currently trading around 98.30. Oversold daily stochastics are edging higher and the bearish daily Tension Indicator is flattening, suggesting room for a test of congestion resistance at 98.50. A break will open up stronger resistance at further congestion around 99.00 and the 99.18 high of 8 April. But negative weekly charts should prompt renewed selling interest towards here. Meanwhile, a close back below congestion support at 98.00, not yet seen, will add weight to sentiment and extend late-March losses back towards 97.50.

The Q1 NZ CPI could further tilt the RBNZ hwakish if we see another beat. The RBNZ has begun to shake off their dovish tilt after overshooting CPI exacerbated by energy shock. Market consensus is seeing Q1 CPI to be around the 3% ballpark but there is a good chance for a beat on the sustained oil spike.

On the chart, the pair turned lower from the .5920 high as prices consolidate strong gains from the .5680 low of 3 April and unwind overbought intraday studies. Daily studies are overbought as well and suggest scope for pullback to support at the .5850 congestion. Below this will open up room for deeper pullback to the .5800/.5795 congestion and 13 April low. Corrective pullback is expected to give way to renewed interest later. Above the .5920 high and see room for extension to strong resistance at the .5930/50 February low and congestion area then the .6000 figure.