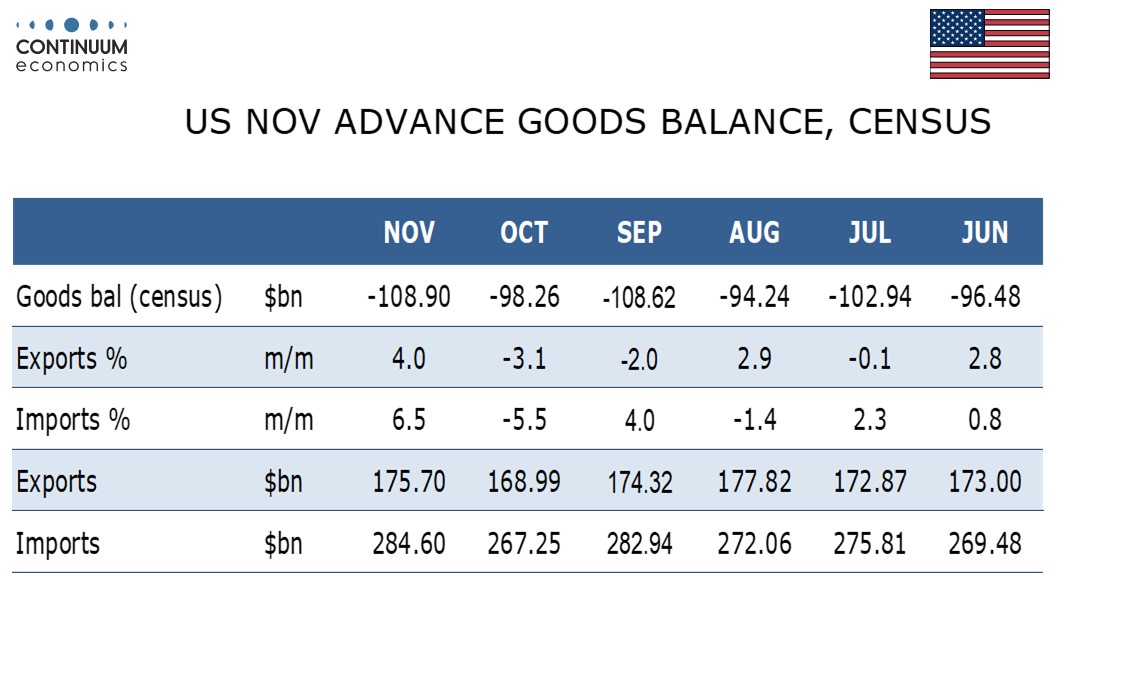

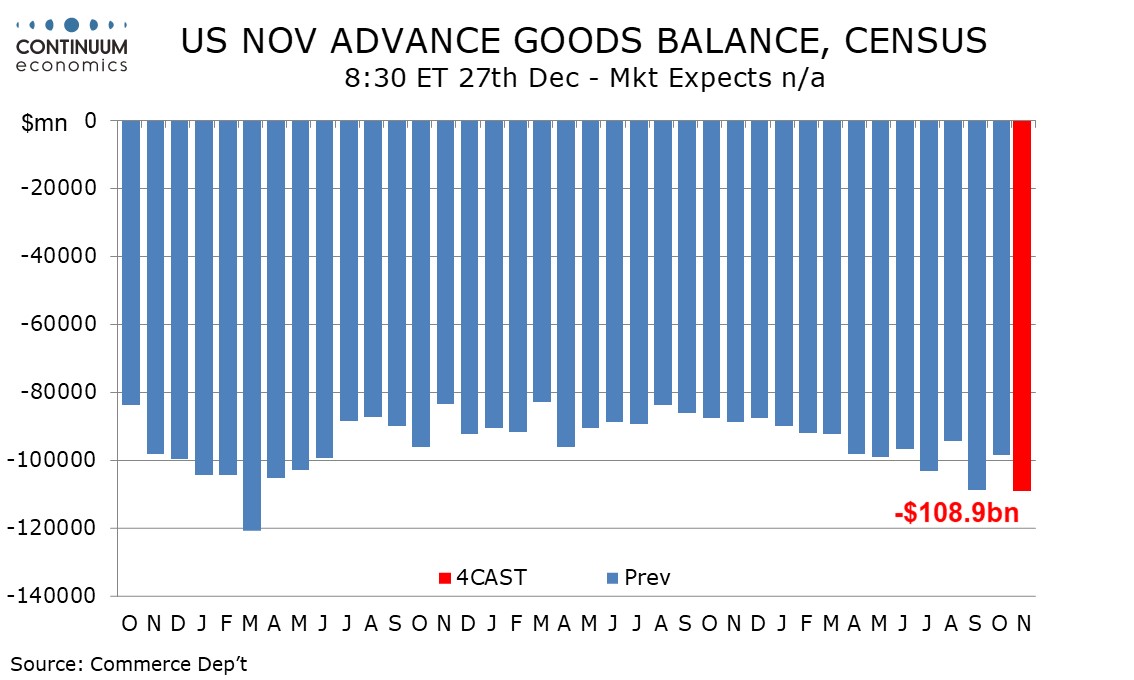

Preview: Due December 27 - U.S. November Advance Goods Trade Balance - Deficit, exports and imports to rebound from October dips

We expect an advance November trade deficit of $108.9bn, up from $98.3bn in October and moving above September’s $106.2bn to bring the widest deficit since March 2022.

We expect exports to rise by 4.0% after a 3.1% October decline while imports rise by 6.5% after a 5.5% October decline. October’s data was likely depressed by a brief strike at Northeast ports at the start of the month. Both export and import prices were virtually unchanged in November so the gains will be almost fully on volumes.

The threat of tariffs may further inflate imports but that may be more of an issue in December than November. Further insight on Q4 GDP will be provided by advance retail and wholesale inventory data for November due alongside the advance trade data. If imports rise, inventories are likely to as well.