FX Daily Strategy: Asia, February 13th

US PPI risks on the upside

USD could extend Wednesdays gains, particularly against riskier currencies

JPY weakness and equity strength look unreliable

GBP vulnerable to weak GDP data

US PPI risks on the upside

USD could extend Wednesdays gains, particularly against riskier currencies

JPY weakness and equity strength look unreliable

GBP vulnerable to weak GDP data

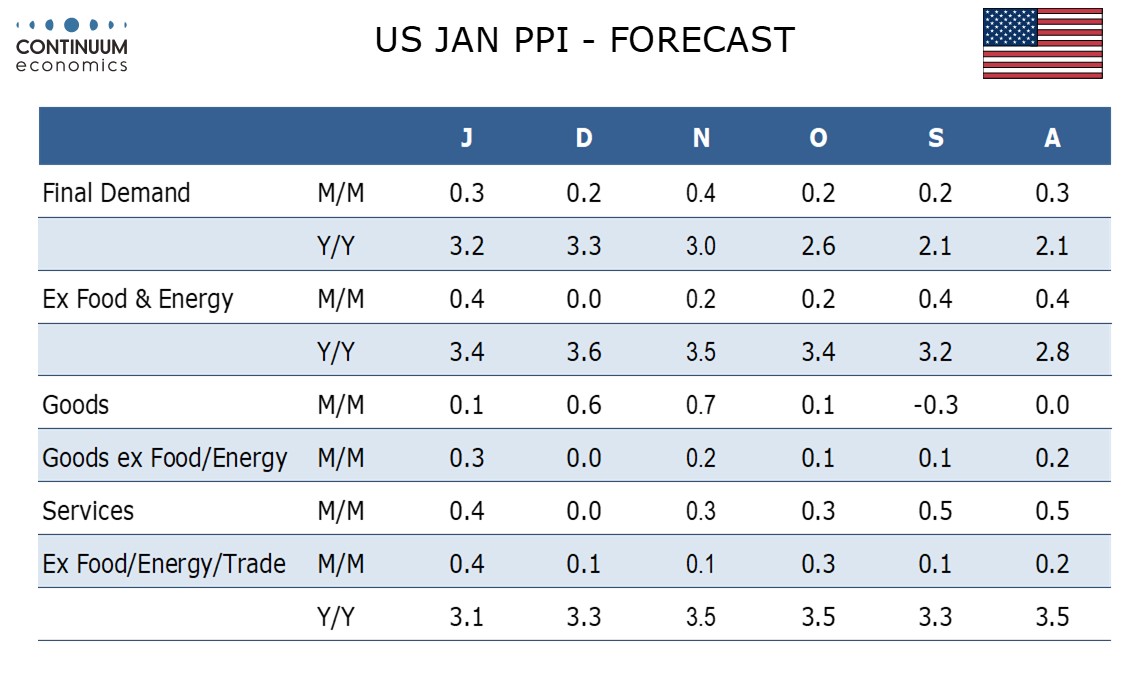

Following on from US CPI Thursday sees US PPI data. We expect January PPI to pick up from a below trend December, rising by 0.3% overall and 0.4% in both core rates, ex food and energy and ex food, energy and trade, as new year price hikes are introduced. However, a stronger rise in January 2024 will allow yr/yr rates to slip. Our core forecasts is above the market 0.3%, so could extend the USD positive reaction seen after the CPI data.

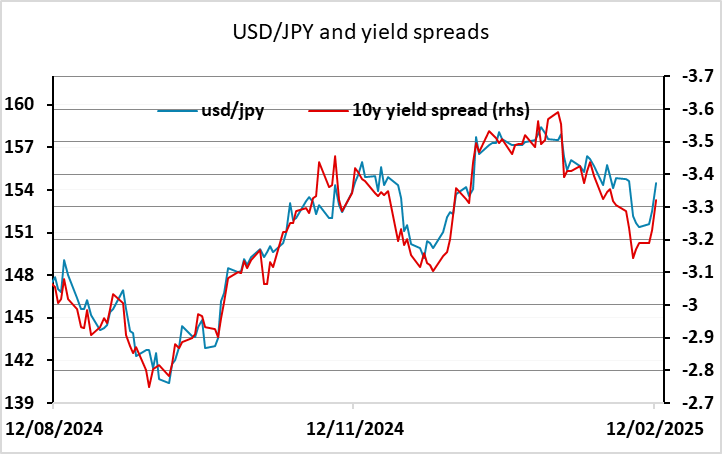

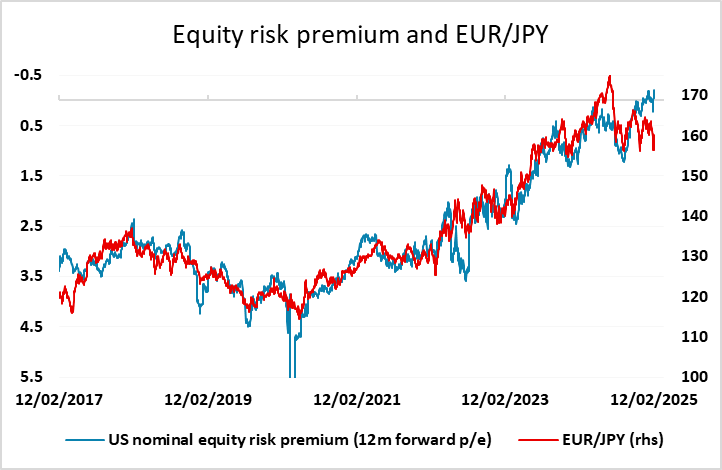

In fact, only USD/JPY and to a lesser extent USD/CHF really sustained the gains seen after the CPI data. EUR/USD recovered back to pre-data levels by the end of European trading, helped by a very resilient equity market performance which gave support to all the riskier currencies. This looks a little too good to be true, as higher yields driven by higher inflation are much less equity positive than higher yields driven by stronger growth, and US equity indices remain very close to the all time highs. Having said this, the JPY has gained on the crosses this year despite equity risk premia remaining at very low levels. There has been a strong (negative) correlation between EUR/JPY (and other JPY crosses) and (US) equity risk premia in recent years, and the resilience of equities suggests there is some scope for recovery in EUR/JPY and other JPY crosses. The EUR also gained support from EUR yields being dragged higher by US yields.

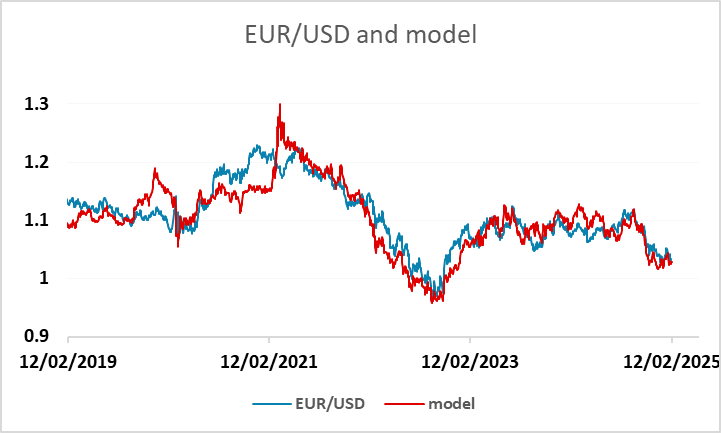

Even so, our models don’t suggest any EUR/USD upside above 1.04, and yield spreads suggest USD/JPY gains above 154 are also overdone, so that EUR/JPY above 160 is also likely to be a medium term selling area.

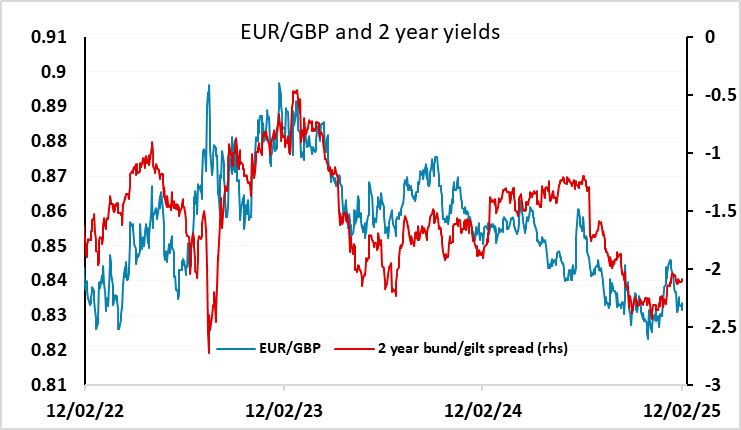

In Europe, UK Q4 GDP will be of interest. Recent data add to already-growing questions about the UK’s economy’s strength, as seen in sizeable q/q gains in the first two quarters of the year. We see a flat m/m reading for December but, combined with drops in the two previous months, this should mean that Q4 numbers (released alongside) see the first drop in five quarters at -0.1% q/q. Indeed, without revisions, December GDP needs to rise 0.2% m/m to avoid a Q4 fall and mild, wet and stormy weather (which may already have caused a drop in December retailing) argue against any such a rise. Moreover, this poses the likelihood of the BoE GDP estimate being undershot for a second successive quarter adding to BoE growth concerns that are also being fanned by business survey data. Our -0.1% q/q forecast is in line with consensus, but nevertheless suggests EUR/GBP risks are on the upside.