FX Daily Strategy: N America, May 29th

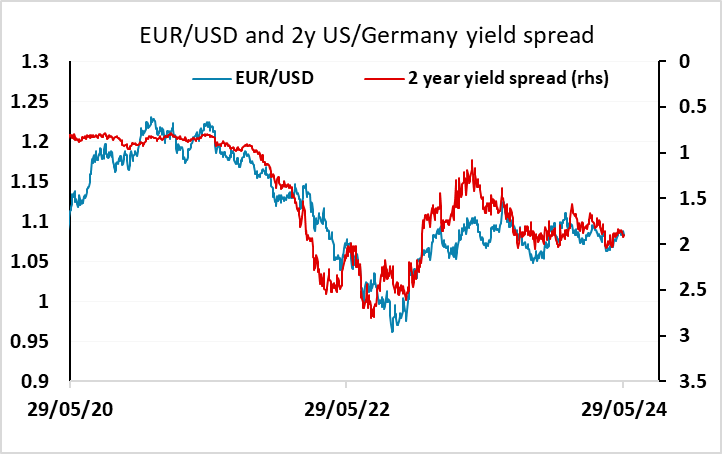

EUR/USD may struggle to extend recent gains as ECB talks dovish

German CPI data may lead to market pricing more ECB rate cuts

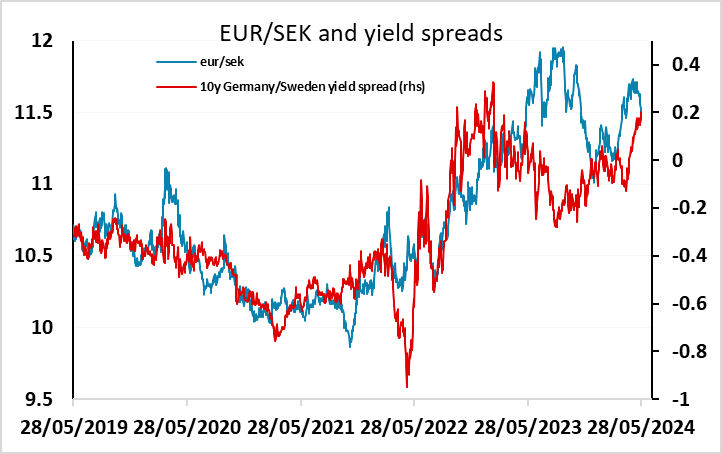

SEK strength could extend as market takes Riksbank comments on board

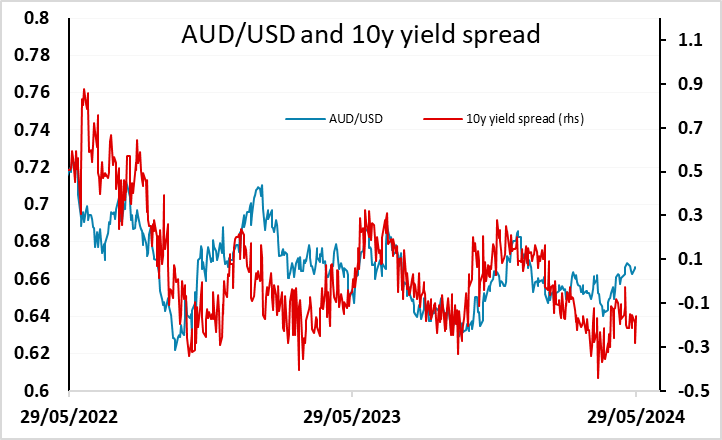

AUD upside looks limited

EUR/USD may struggle to extend recent gains as ECB talks dovish

German CPI data may lead to market pricing more ECB rate cuts

SEK strength could extend as market takes Riksbank comments on board

AUD upside looks limited

German state CPI data look to be broadly in line with expectations. The market consensus is for a rise in the y/y rate for the national CPI to 2.4% in May (2.7% HICP basis) from 2.2% in April (2.4% HICP basis). The average rise in the y/y rate for the state CPIs is around 0.2%, with North Rhine Westphalia and Bavaria, two of the largest states, both rising 0.2% to 2.5% and 2.7% respectively (from 2.3% and 2.5%). However, front end yields are a little lower, and EUR/USD has dropped around 20 pips, suggesting the market sees the data as being on the soft side of expectations. Slightly weaker than expected household loan data in the money and credit data, which showed a 0.2% m/m rise, may also have contributed, but we don’t see the decline in yields or the EUR as really being justified by the data. However, the market is only pricing in a little more than two rate cuts this year, and this looks to be overly conservative in our view, especially given the recent dovish comments from ECB council members Lane and Villeroy, so there is some downside scope for yields in the bigger picture. Even so, the stronger German confidence numbers earlier suggest better growth prospects are materialising, and this should be EUR supportive even if rate cut expectations rise. We therefore would still see support above 1.08 for EUR/USD.

The SEK performed well on Tuesday after comments from Riksbank governor Theeden indicating that a June rate cut was unlikely following on the from the cut already seen in May. EUR/SEK dropped around 4 figures, but the market is still pricing a June rate cut as around a 33% chance, which looks too much in the wake of Theeden’s comments. EUR/SEK has fallen back into line with the historic relationship with yield spreads, but if the market reprices to no change in rates in June, there should still be more upside for the SEK and EUR/SEK might dip sub 11.40. Wednesday sees money supply, lending and retail sales data, but these are unlikely to provide reasons for renewed expectations of a rate cut.

The AUD started the week strongly, moving off support at 0.66 towards the recent highs above 0.67. Wednesday saw Australian April monthly CPI data which came in higher than expected at 3.6% y/y. While it is not as comprehensive as the quarterly CPI, it is likely the q2 CPI will likely come in higher than expected and further delay the pace of rate cuts. The level of inflation is still moderating towards RBA's target range of 3% and we are not forecasting the RBA to restart tightening for a small bump. Currently, yield spreads don’t really support further AUD strength, even with the market not pricing any RBA rate cuts until well into 2025, so the 0.67 area for AUD/USD looks likely to be a bridge too far in the near term.