FX Weekly Strategy: Sep 1st - 5th

US employment report the prime focus

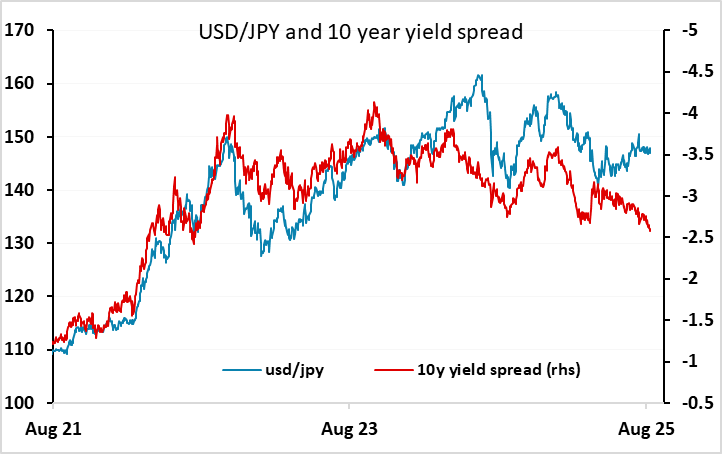

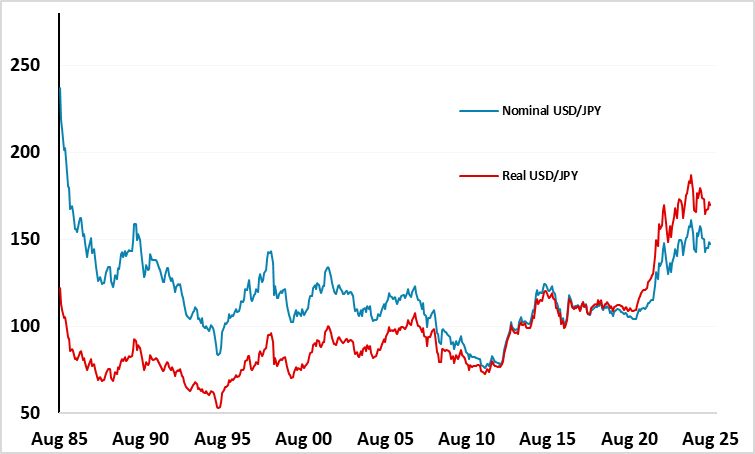

USD risks skewed to the downside, particularly against the JPY

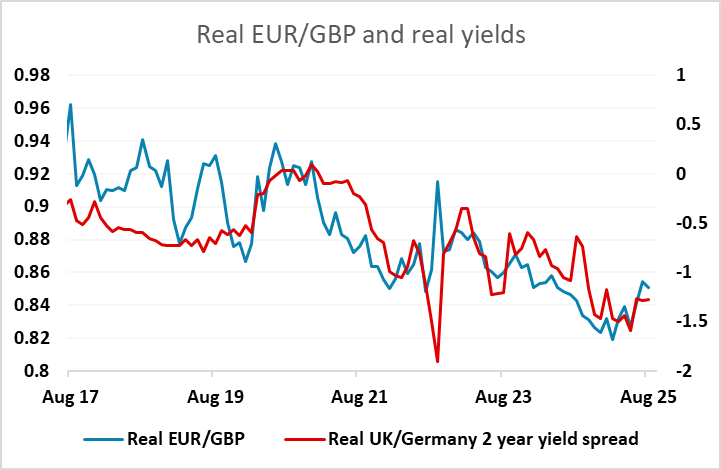

GBP biased lower as fiscal tightening likely to lead to lower UK real yields

Strategy for the week ahead

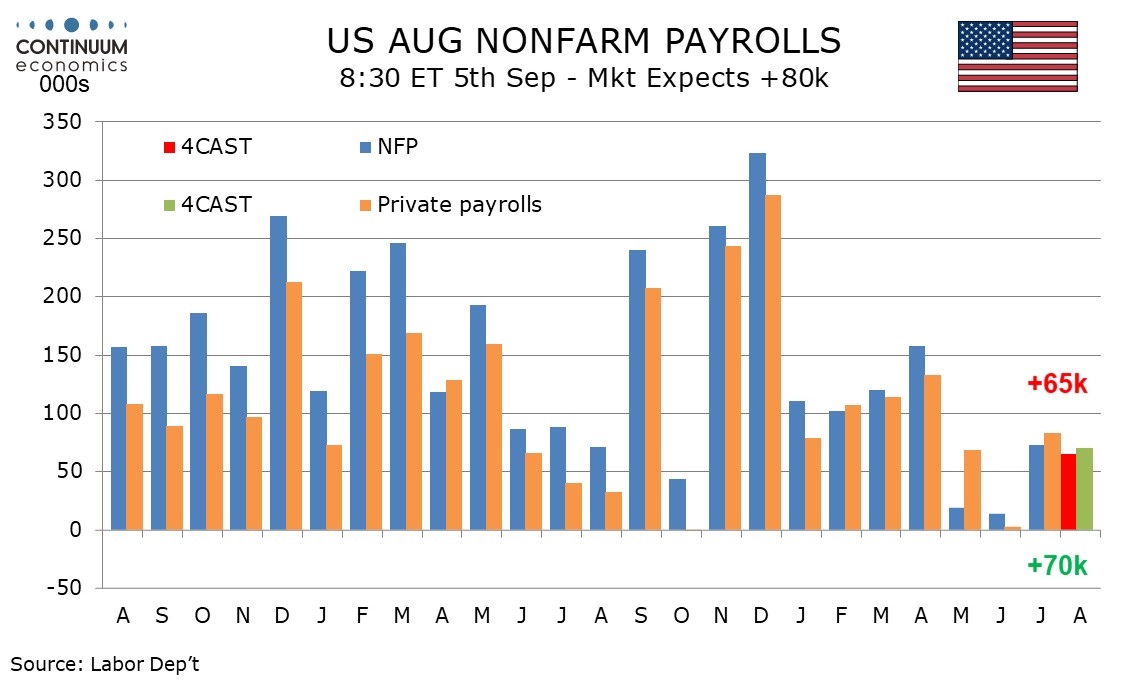

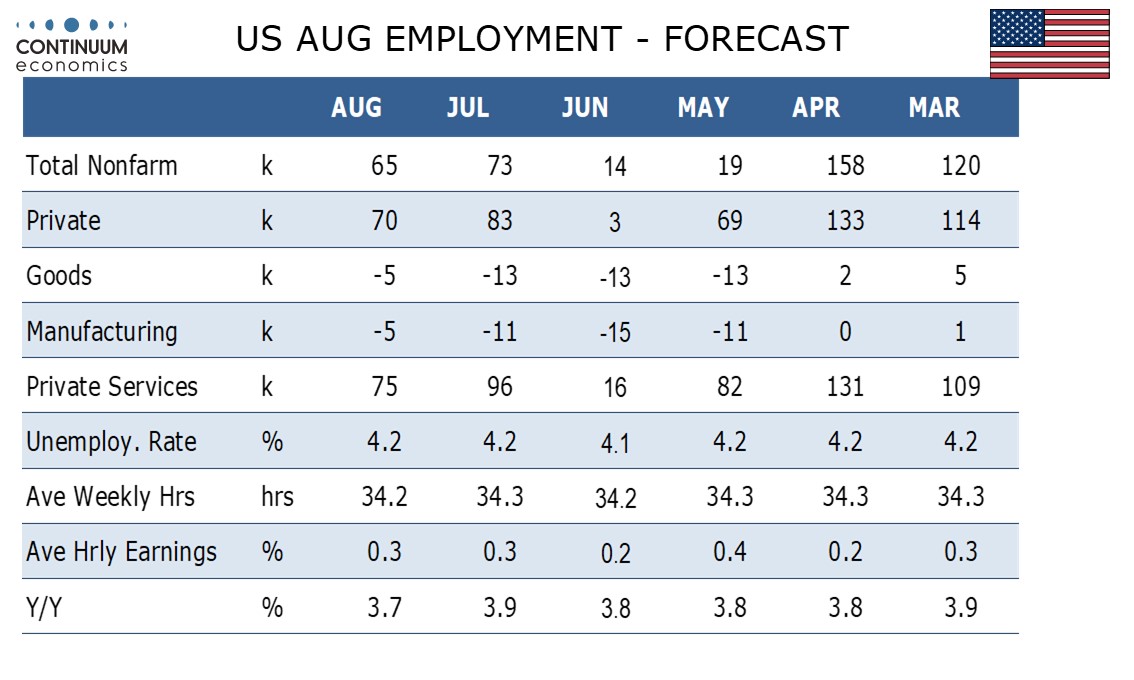

The US August employment report on Friday will be the main focus of the week, and is of greater interest than usual after the much weaker than expected July report which included downward revisions to the April and May payroll data. Our forecast of a 60k gain in non-farm payrolls is slightly below the market consensus of 70k, but either way, we are close to getting the first negative number since 2020, with a standard deviation of near 100k in recent years. The May and June gains were tiny by recent standards, and the jobless claims data in survey week showed a blip higher, so there is a clear risk of a negative number.

As it stands, the market is pricing in just below a 90% chance of a September easing and 137bps of easing by the end of 2026. This is quite an aggressively dovish outlook, and if the economy shows solid growth into the end of 2026 is unlikely to be achieved. The latest Fed dot plot indicated a median expectation of 3.25%-3.5% at end 2026. But the pricing includes the risk of a significant downturn which could see rapid Fed easing in the hear term, as well as some risk that Trump impacts Fed policy when Powell is replaced next year. So we wouldn’t anticipate much rise in US yields on a number sub-150k, while something sub-zero could see the market pricing in a risk of a 50bp cut in September.

The USD therefore looks vulnerable coming into the data, particularly against the JPY. Yield spreads already suggest USD/JPY is significantly overvalued base don recent correlations, and it is of course fundamentally even more overvalued than it looks based on nominal yields, as relatively high US inflation has led to an even larger real USD appreciation. Against the EUR, the USD has underperformed yield spread moves this year, so EUR/USD may benefit less from any weak US data and decline in US yields, particularly if there is a negative knock on effect on equities. While equities will tend to benefit form lower yield other things equal, weak employment data will end to mean both lower yields and lower equities, and would consequently likely prove very positive for the JPY on the crosses. Of course, a stronger number is also possible, but we see the risks of a USD/JPY reaction as heavily skewed to the downside.

GBP fell back on Friday helped by reports that the UK government was considering a tax on commercial bank balances at the Bank of England. We are seeing trial balloons of all sorts of tax ideas for the UK most weeks, as the government is known to need to raise significant revenue – likely upwards of £20bn – at the October Budget. This upcoming austerity remains a negative factor for GBP despite some relatively strong data of late and a quite hawkish market outlook for the BoE. From here, it looks as if the market expectation of BoE policy can only get easier, with only 42bps of easing priced by the end of 2026. In the longer run, we can expect to see convergence between real UK yields and real yields in the Eurozone, and this suggests that EIR/GBP risks are on the upside.

Data and events for the week ahead

USA

The key US release will be August’s non-farm payroll on Friday. We expect a 65k increase, similar to July’s 73k and stronger than the minimal gains for May and June that were revised down sharply with July’s report. We expect unemployment to remain at 4.2% and a second straight 0.3% rise in average hourly earnings. Revisions will be closely watched after last month’s shock, but we do not expect any large revisions this time.

On Thursday we expect ADP’s employment report to show a rise of 60k in private sector jobs. We expect a 70k increase in private sector non-farm payrolls on Friday. Other labor market signals will come from July’s JOLTS report on job openings on Wednesday, and weekly initial claims on Thursday.

July data is due from construction spending on Tuesday, factory orders on Wednesday and the trade balance on Thursday. Thursday will also see revised Q2 productivity and costs. The Fed’s Beige Book is due on Wednesday when Fed’s Musalem is due to speak. Williams and Goolsbee will speak on Thursday. Monday sees a US holiday for Labor Day.

Canada

Canada’s key release will be August employment on Friday. August S and P PMI data is due for manufacturing on Tuesday and services on Thursday, with the Ivey manufacturing PMI following on Friday. Thursday also sees August’s trade balance.

UK

The week ahead has moderately interesting data wise beginning with BoE money and credit data (Mon) where housing market volatility and distortions may again be the order of the day but with further signs of an underlying weakening as may be evident in Nationwide house price data earlier the same day. Final Manufacturing PMI (Mon) will attract little interest as may final Services PMI (Wed) but with fresh survey messages coming from the BoE Decision Makers Panel numbers on Thursday as well as well as the construction PMI (Thu), the latter having remained very weak of late.

The main official data are Friday’s July retail sales numbers which have been delayed by two weeks due to quality assurance issues – NB; the data has been volatile and somewhat more upbeat than survey numbers. Albeit unclear as to whether revisions will occur, we still see a m/m correction but with it unclear how a very warm month may have affected spending.

Eurozone

Several important updates are due this week. The main focus will be the flash HICP for August (Tue). We see a 0.1 ppt rise in the headline to 2.1%, hinting that the ECB’s Q3 projection could be overshot. But this is largely food and energy base effect driven as the core rate in August may drop from 2.3% to a fresh cycle low of 2.1%. But Monday’s labor market data may be even more important now that the ECB has started to acknowledge the increase in labor supply seen of late. Thursday sees retail sales where a fresh correction back may be in the offing.

The first breakdown to EZ GDP Q2 data (Fri) may show growth was partly based around a rebuild in inventories with final PMIs Mon and Wed) as well as the construction counterpart (Thu), the latter having remained very weak of late. Otherwise, Friday sees likely more volatility superimposed over underlying weakness in German Orders. As for the ECB, President Lagarde speaks at an European Systemic Risk Board conference on Wednesday

Rest of Western Europe

There are a few key events in Sweden, most notably flash CPI data for August (Thu) important to see if the July spike persists; we see that energy-induced upside surprise being partly reversed with CPIF inflation down 0.2 ppt from 2.8%. Otherwise, in Switzerland, Friday sees what may still be soft CPI figures for August, likely to stay around 0.2% y/y and thus hinting at a slightly higher Q3 result than SNB thinking.

Japan

Pretty empty calendar for Japan next week. Only overall household spending on Friday would be of much importance. There has been minimal recovery in household spending, it will be critical to see continuous growth for the Japanese economy to remain healthy. We forecast choppy uptrend for real wage goes back and forth into the negative/positive territory.

Australia

The q2 GDP will be released on Wednesday and we expect an expansive quarter. However, private inflation gauge on Tuesday may have more impact towards policy expectation. We also have the trade balance on Thursday, it remains interesting to see trade development after the dust settles for Trump’s tariff.

NZ

Building permit on Monday and a slate of tier 2-3 data will not be impactful for the Kiwi.