FX Weekly Strategy: Asia, February 23-27th

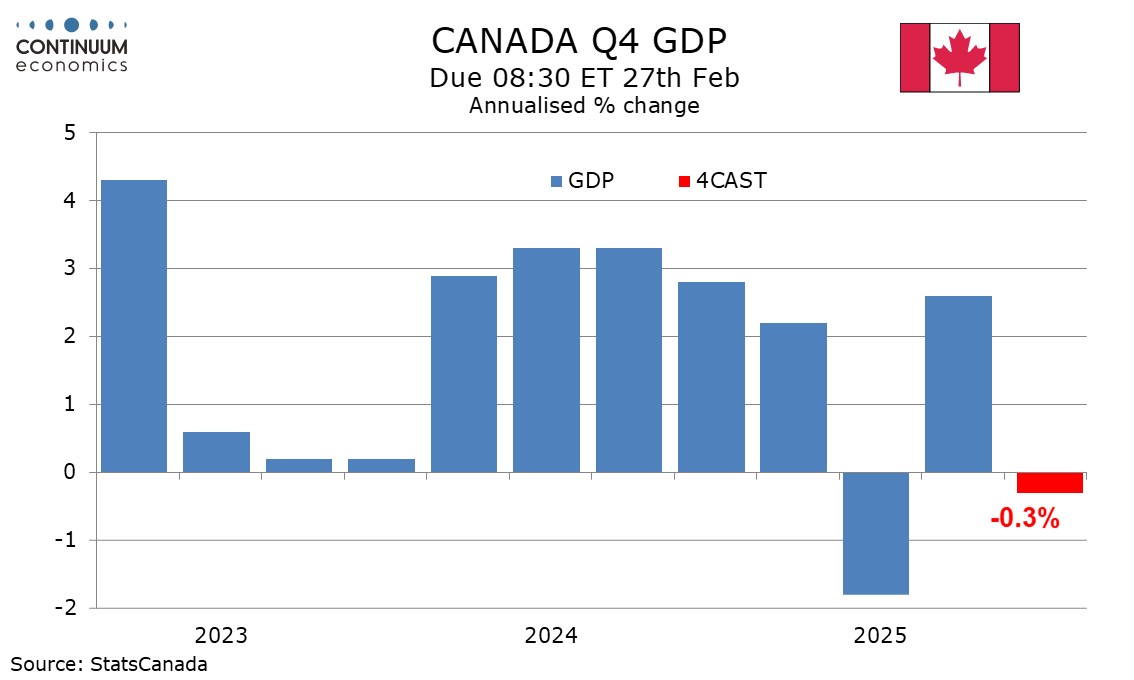

Canada Q4 GDP a modest correction from a surprisingly strong Q3

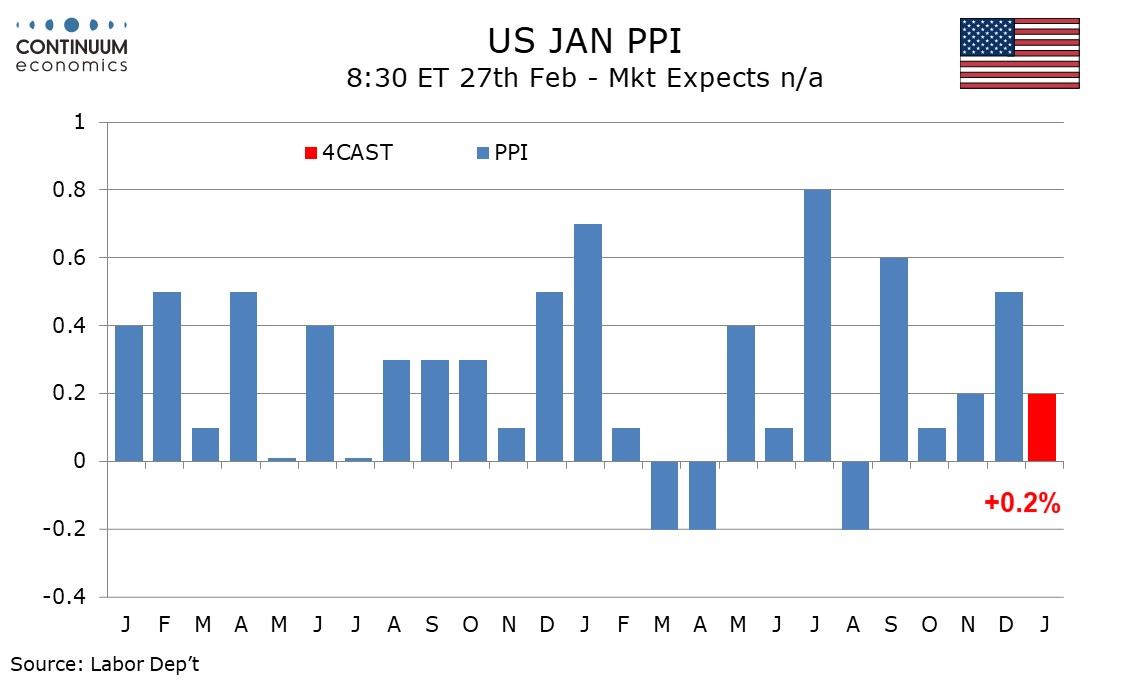

U.S. January PPI Slower than a strong December, but trend still quite firm

Australia CPI Will be Lively

Will Tokyo CPI Dip Further

We expect Q4 Canadian GDP to decline by 0.3% annualized, marginally softer than an unchanged estimate made by the Bank of Canada with January’s Monetary Policy report. This would be consistent with December GDP rising by 0.1% as projected with November’s data. The GDP decline would be a modest correction from a 2.6% Q3 increase that significantly exceeded expectations, though we expect Q4 to see a modest 0.4% increase in domestic demand after a 0.1% decline in Q3. We expect household consumption to look similar to Q3 with a 0.4% decline but gross fixed capital formation to rise by 0.9%. While the latter would be a slowing from Q3 we expect Q4’s increase to come from the private sector, while Q3’s gain came mostly in government. We expect government investment to correct from the strong Q3 but government consumption to see a modest increase after a Q3 decline, though overall consumption will still be marginally negative.

We expect PPI to rise by a slower 0.2% in January both overall and ex food and energy, after strong respective gains of 0.5% and 0.7% in December. The slowing will be largely in trade, though ex food, energy and trade we expect a rise of 0.3%, slightly slower than December’s 0.4%. We expect gains of 0.3% in food and 0.5% in energy after both declined in December, but these gains will not be quite enough to lift the headline above the 0.2% ex food and energy rate.

We expect goods PPI ex food and energy to rise by 0.3% after a 0.4% increase in December. Trend has been accelerating modestly, with the last six months having seen four gains of 0.4% or above and two at 0.2%, while the first six months of 2025 saw four gains of 0.3% and two of 0.2%, while trend in 2024 was slightly below 0.2% per month. The acceleration is likely due to tariffs, and there may be more to come, though trend still appears to be fairly close to 0.3% per month.

The Australian CPI will be lively after the RBA's hawkish tilt. It is widely expected to remain above the 3% target range but we are wary of speculation it will run further hotter from there. What is more important is the trimmed mean CPI, where a high read will persuade market participant to speculate of another imminent hike coming. Thus, driving the Aussie higher on the release.

On the chart, the pair is leaning lower in consolidation below the .7100 level and see room for pullback to the .7000 level. Break here will see deeper pullback to retrace the November/February rally and see extension to strong support at the .6900 level and .6870, 38.2% Fibonacci level. Meanwhile, resistance at the .7100 level now expected to cap. Regaining this will ease the downside pressure and clear the way for retest of the .7147 high and see scope to further extend gains from the April 2025 low.

The February Tokyo CPI will be closely watched, especially when the January low read in National CPI, to see whether the inflationary pressure is easing sustainably. We believe any low read is more of base effect and latest round of energy rebates, rather than the easing of underlying inflationary pressure. However, if we do not see a steady wage growth or early signs of spring wage negotiation wanes, it may begin to sway market sentiment.

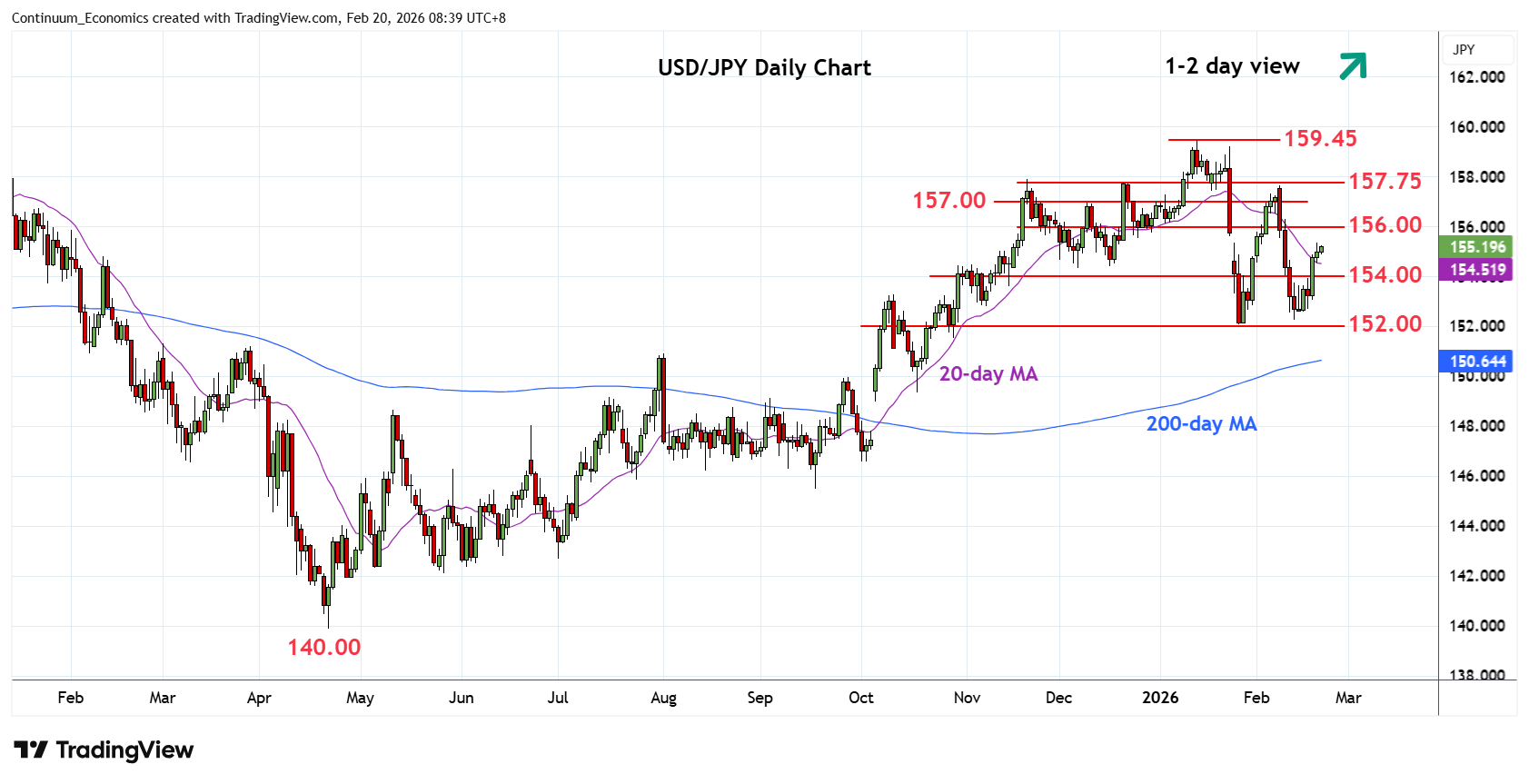

On the chart, the pair is extending bounce from the 152.27 low as prices retrace sharp losses from the 157.66 high of last week. Gains are seen corrective with resistance at the 155.50/156.00 congestion area expected to cap. Break here, if seen, will open up room for extension to 157.00 level and strong resistance at the 157.75/90 area. Corrective bounce expected to give way to fresh selling pressure later with support raised to the 154.00/153.00 congestion. Break here will return focus to the downside for retest of the 152.27 and 152.10 lows.

Recap of the Week

U.S. January Yr/yr ex food and energy CPI slowest since March 2021

FOMC Minutes Shows Splits, But Rate Cuts Should Still Arrive

RBNZ Keeping Their Cool

UK CPI Fresh and Marked Fall Resumes as Core Slips to Cycle-Low?

Washington and Delhi Recalibrate

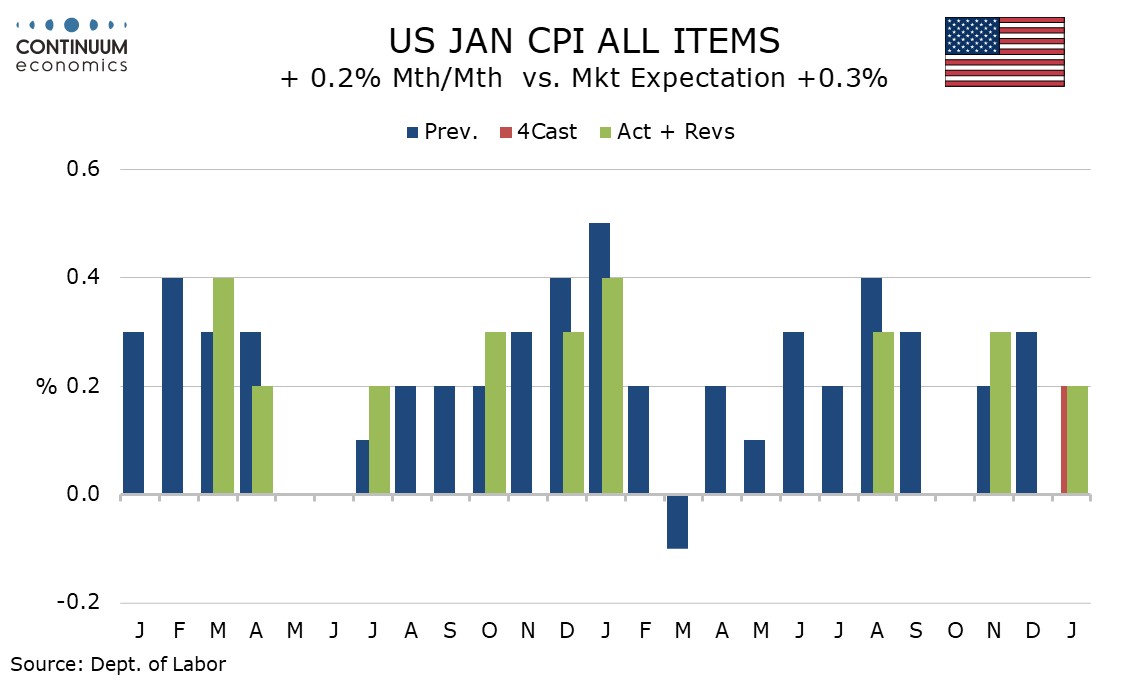

January CPI is slightly lower than expected at 0.2% overall though the ex food and energy rate at 0.3% is on consensus, with the core rate almost spot on 0.3% even before rounding. Given a strong year ago rise, yr/yr growth slowed, overall to 2.4% from 2.7% and the core to 2.5% from 2.6%, the latter the slowest since March 2021. The Fed can take some modest comfort from the release even if the monthly core rate saw its firmest since August, given that January data has had a tendency to be firm in recent years. The new year does not appear to have produced a significant acceleration in tariff pass-through.

Given that CPI tends to outperform PCE prices the data could even be seen as consistent with target, though with core PCE prices, for which December data is not yet visible, looking set to see an unusual outperformance of CPI in Q4 2025, on target core PCE prices are unlikely to be seen soon. The CPI, while moderately encouraging, is not going to significantly accelerate the next Fed easing.

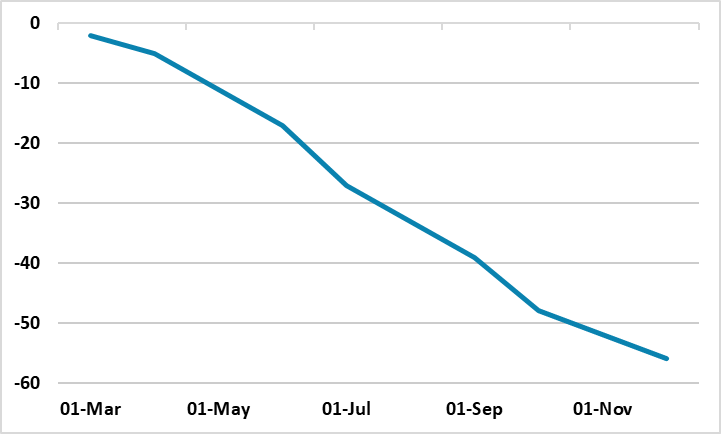

Figure: Fed Rate Cuts Discounted (%)

The January FOMC minutes show a split Fed, with some sounding mildly hawkish. However, the district Fed presidents are on the mildly hawkish side, but most are non-voters and we feel that the FOMC voting consensus is more neutral. Additionally, we feel that Fed is too upbeat on the economy and as consumption slows towards income growth through 2026, and inflation continues to slow, that the Fed will still cut rates. We thus still pencil in 25bps cuts from the Fed for June and September to bring the Fed Funds rate down to 3.00-3.25%. However, even within the 12 FOMC members some dissent is likely and this could lead to a few disputing a June cut and more voting against a September cut.

FOMC Split, but one camp felt that the Fed could consider rate cuts in the future; a 2nd camp felt that with the labor market is now not as weak as the autumn and that the Fed could go on hold and a 3rd camp saying that if inflation remains high that the Fed might have to consider raising rates. However, it is worth pointing out that the district Fed presidents have been more hawkish than the Fed governors or the FOMC voting decisions and some of the hawkish views could be non-voting members. For example, remember that 6 district Fed presidents did not want to cut the discount rate in December. Finally, some officials noted that cutting rates could sent the wrong signal that the Fed are less committed to the 2% inflation target, but this likely reflects an emotional backlash against Trump administration pressures on the Fed and non-voting members. Later in the year when it comes to data review, this emotion will likely be less important.

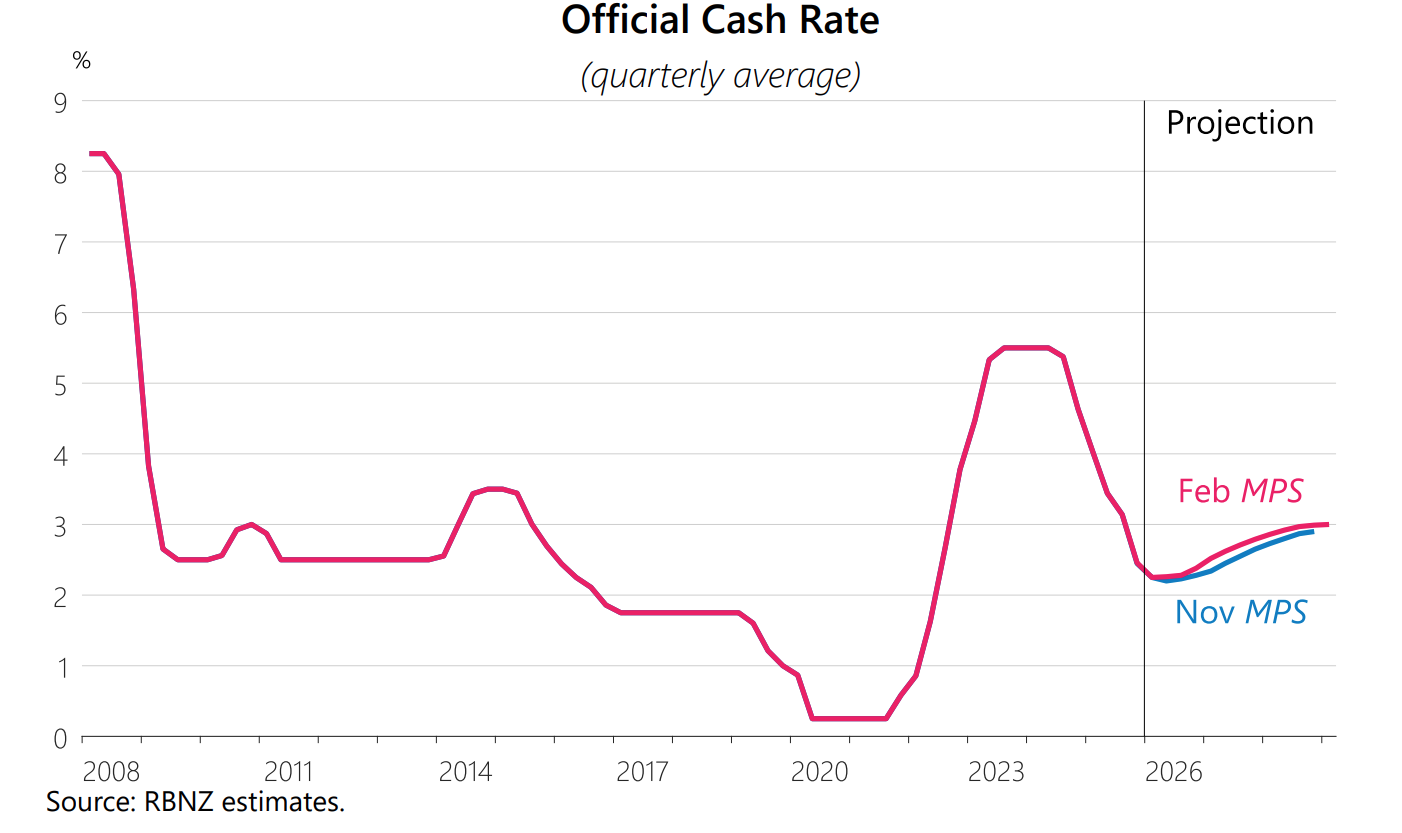

The RBNZ kept rates unchanged at 2.25% in the February meeting and signal they will be on hold for a while. The RBNZ continue to see current overshooting inflation transitory from food, international airfares, and overseas accommodation. They believe inflation will return to target range in Q1 2026 and reach mid point in Q1 2027. The February OCR forecast is little changed from the November forecast, pointing towards the first hike in Q4 2026.

Some key takeaways:

Balance Inflation Outlook: Despite the current overshoot, the RBNZ see inflation risk to be balanced. Both underlying and transitory pressure are considered, so as domestic and global demand. The forecast is suggesting all sides are balanced.

Spare Capacity: The RBNZ highlight "spare capacity" in their statement while signaling economic activity has recovered. They see spare capacity remains as unemployment rate increases but partial caused by increasing labor forces. Yet, "The economic recovery has been uneven across sectors and regions. Stronger activity has been observed in the rural economy and in the primary sector." suggest economic activity still need some more traction.

Global Outlook Uncertain: The RBNZ believe the global economic outlook to be highly uncertain, especially regarding trade policies, AI valuations and geopolitical tension. They also highlighted China's weak domestic demand and excess upply could be disinflationary.

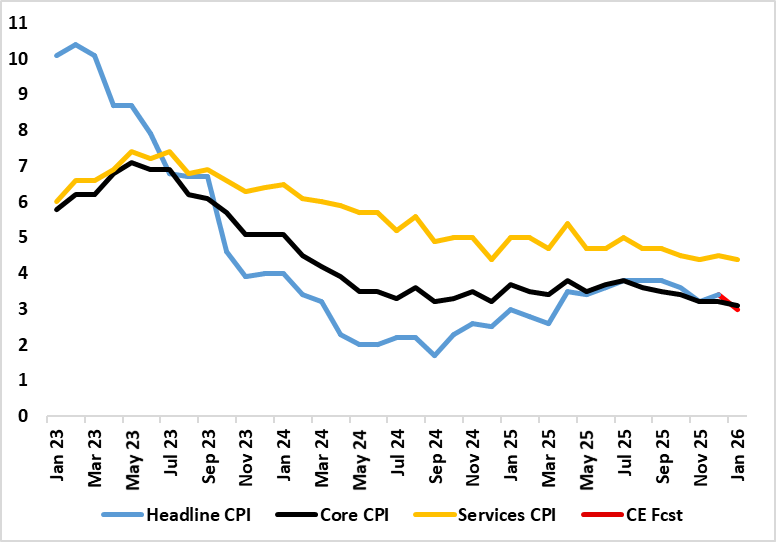

Figure: Headline Falls Clearly

Although most aspects of the January CPI came in a notch above BoE thinking, the clear fall in the headline rate and further looser labor market messages still point to a BoE rate cut next month, not least given the likely return to the 2% target by April. These projected falls started with these January numbers (Figure) where airfare distortions which pushed up the December outcome unwind, and where base effects helped reduce food inflation – albeit where PPI numbers also point to softer such price pressures. As a result, the headline CPI rate fell from December’s 3.4% to 3.0% (a 10-mth low). Services and the core rate fell both 0.1 ppt to 4.4% ad a new cycle low of 3.1% for the latter. Notably such declines have been signalled for some time by adjusted m/m data, with already-soft wage figures likely to result in lower underlying inflation ahead.

Admittedly, not all aspects of the CPI data are reassuring, with a further rise in catering services inflation, often seen as an indicator of price persistence given that the sector’s cost base is very much wage related. Even so, the evidence on this is mixed with HMRC pay data very clearly slowing as slowing in wage inflation for accommodation and food services. Regardless there are very clearly reassuring aspects most notable in even lower rental inflation which at just over 3% has more than halved in the last year, surely an added sign that the housing market is in the doldrums. There is also a further slowing in non-energy goods inflation which probably reflects both weak global demand and dumping of goods by China produce once destined for the U.S.

Although we have been flagging a fall in CPI headline inflation rate down to the 2% target sometime in the spring, this line of thinking is becoming more widespread, helped by some recent Budget measures. Notably the BoE is now suggesting that inflation will fall to 2.1% by April, partly reflecting base effects and largely stay there through Q2. We see a similar drop but (unlikely the BoE’s anticipated more modest drop) also that this will be accompanied by a fall in the core rate to just over 2% by mid-year.

The US–India interim trade pact lowers tariffs after a bruising 2025 dispute, offering relief to Indian exporters while committing New Delhi to expanded market access for American goods. Washington is presenting the deal, including India’s stated intent to import up to USD 500bn in US energy and industrial products over five years, as a strategic and economic win. For India, the agreement stabilises trade flows and strengthens geopolitical alignment with the US, but it raises domestic political sensitivities around agriculture, energy autonomy and trade balance risks. The pact is best viewed as a de-escalation mechanism rather than a full trade settlement, with harder negotiations still ahead.

The US and India have agreed an interim trade framework that pulls both sides back from last year’s tariff escalation, offering relief to exporters while leaving deeper structural frictions unresolved. The agreement, announced in earlier this month, reduces US tariffs on Indian goods to roughly 18%, down from punitive levels that had climbed towards 50% in 2025 amid disputes over market access and energy ties. In return, New Delhi has committed to lowering or eliminating duties on a range of American industrial and agricultural products and signalled its intention to step up purchases of US energy, technology and capital goods over the coming years.

For Washington, the deal is being presented as proof that pressure works. President Donald Trump has cast it as a recalibration that pries open India’s protected market while reinforcing supply-chain diversification away from China. US officials argue that American exporters, from farm producers to machinery manufacturers, will gain greater access to one of the world’s fastest-growing large economies. New Delhi’s framing is more guarded. Indian ministers describe the pact as a stabilisation mechanism rather than a sweeping free trade agreement. They stress that politically sensitive farm segments, including key staples and dairy, remain shielded, and that the framework is “interim”, designed to de-escalate tariffs while negotiations continue towards a more comprehensive bilateral trade agreement.