FX Weekly Strategy: Asia, March 9nd-13th

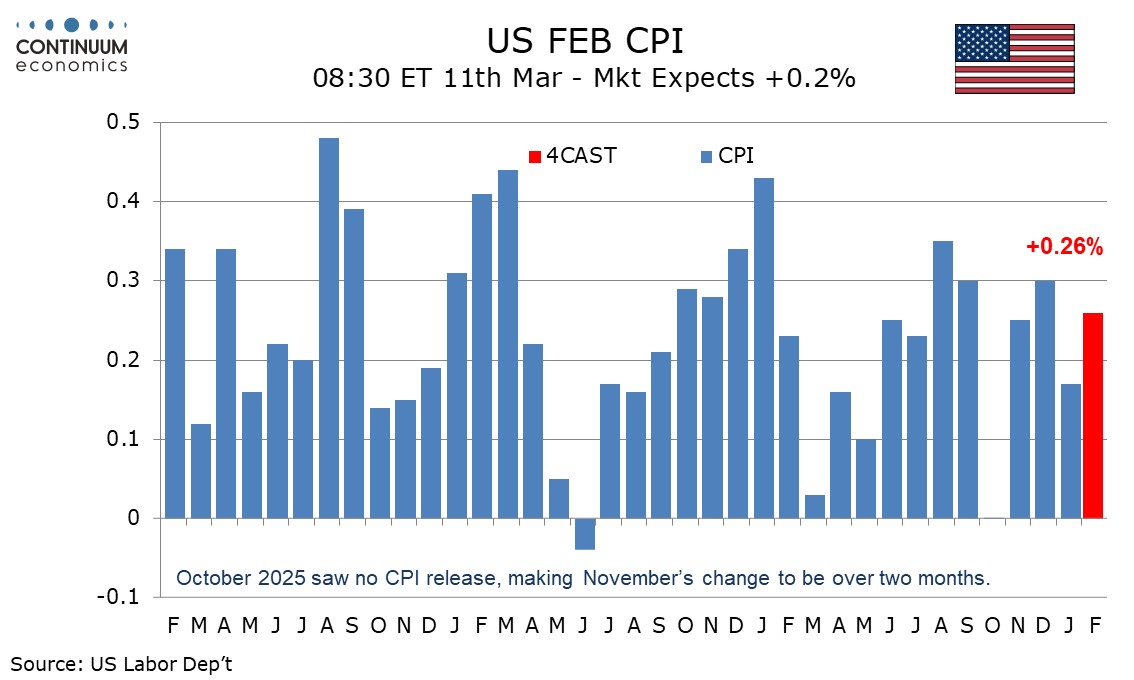

U.S. February CPI A moderate gain

And other U.S. Data

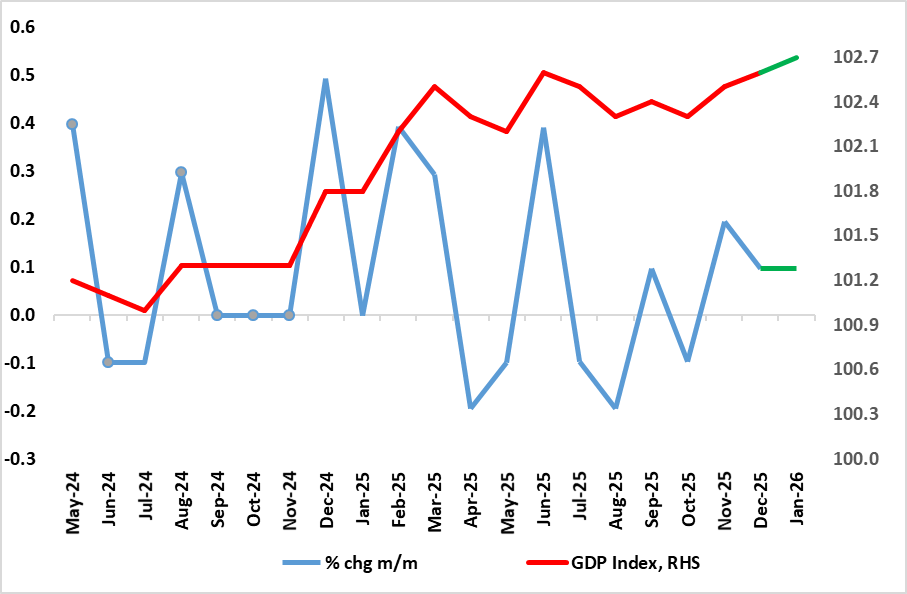

UK GDP Getting Better?

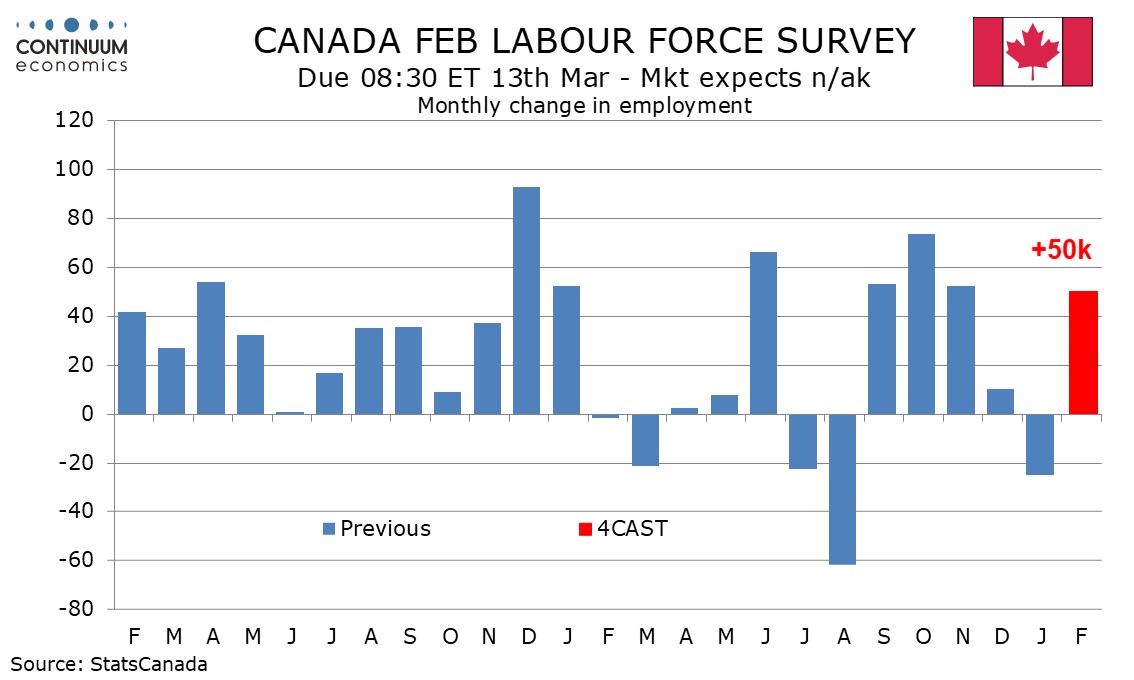

Canada February Employment due for a rebound

We expect February’s CPI to increase by 0.3%, with a 0.2% increase ex food and energy. Before rounding we expect the gains will be similar, with the overall CPI rounded up from 0.26% and the core rounded down from 0.24%. CPI has slowed, but it is too soon for the Fed to declare victory. Boeing orders suggest aircraft will slip further from an exceptionally strong November, leading a 3.0% decline in transport, but they will remain at a firm level. We also expect a weak month from autos and a correction lower in defense, which has a strong overlap with transport, from a strong December, but the outlook for defense orders remains positive. We expect orders to fall by 0.3% ex defense.

January’s core CPI increase of 0.3% was the strongest since August and with January having a tendency for volatility as new year pricing decisions are made, we would be surprised if February was quite as strong. Still, it is too early to declare inflation defeated with PCE prices having unusually exceeded the CPI in Q4 and core PPI having seen a strong gain in January. We do not expect a very soft February core CPI.

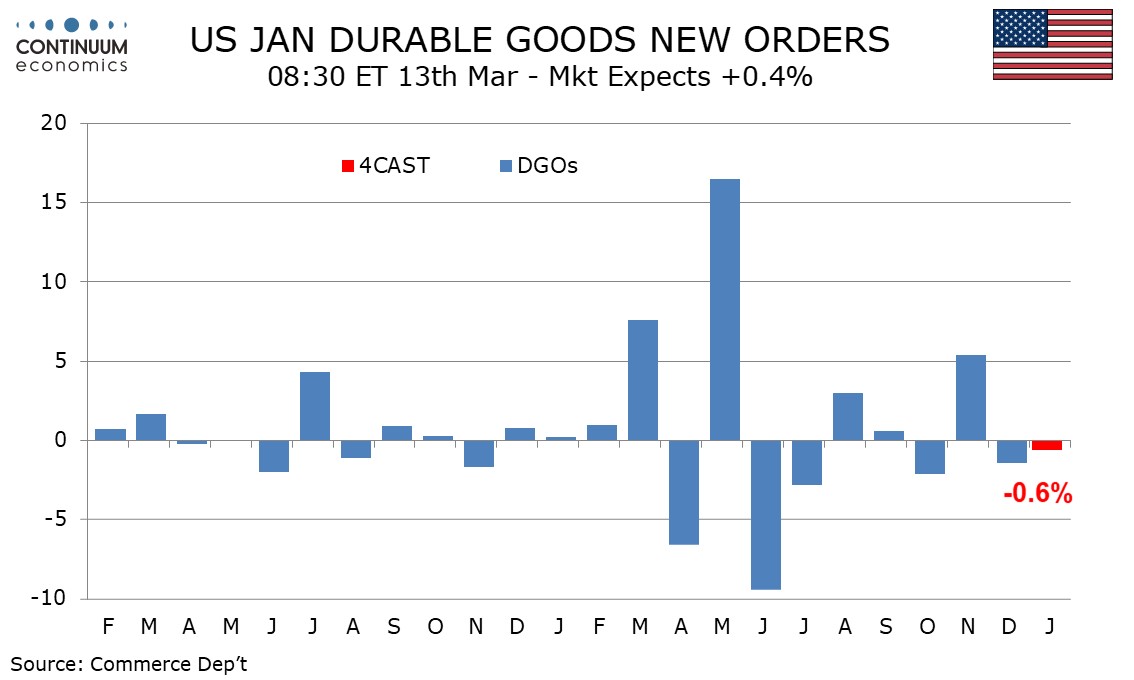

We expect January durable goods orders to see a second straight moderate decline, of 0.6%, as a November surge in aircraft orders continues to correct, but ex transport we expect continued underlying strength to be shown, with a rise of 0.7%. Boeing orders suggest aircraft will slip further from an exceptionally strong November, leading a 3.0% decline in transport, but they will remain at a firm level. We also expect a weak month from autos and a correction lower in defense, which has a strong overlap with transport, from a strong December, but the outlook for defense orders remains positive. We expect orders to fall by 0.3% ex defense.

ISM manufacturing new orders saw a sharp pick up in January and manufacturing output was firmer in January, suggesting ex transport orders will maintain a strong trend. A 0.7% increase would be a ninth straight rise but not quite as strong as December’s 1.0%, with a 3.1% December increase in computers and electronics looking difficult to repeat.

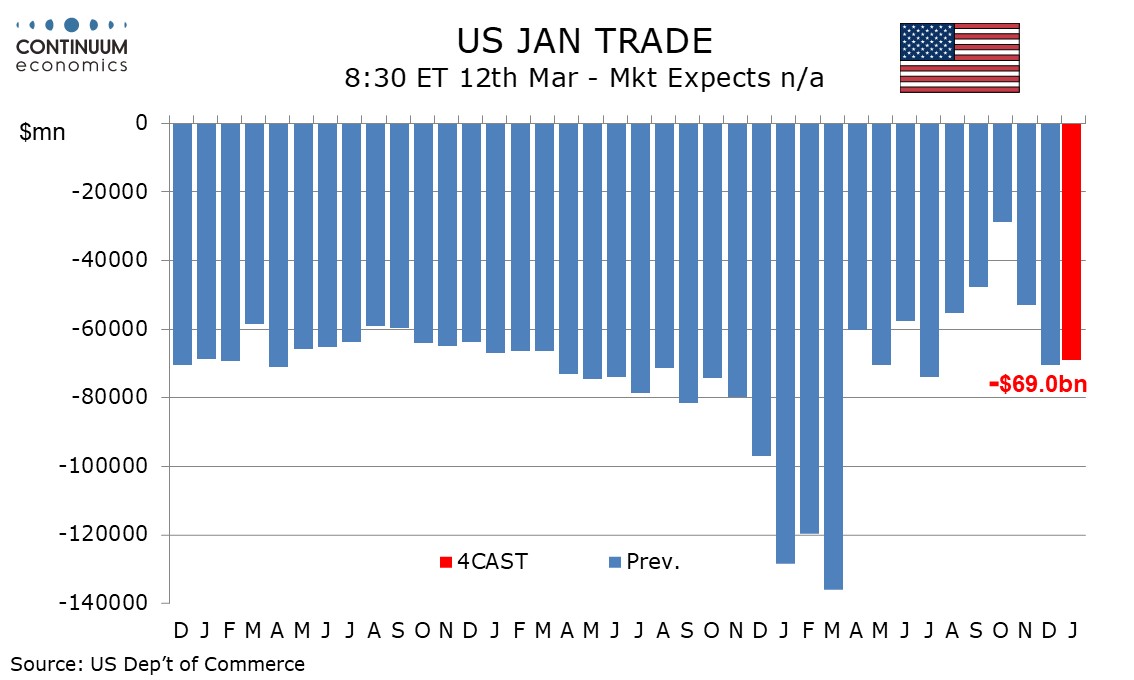

We expect a January trade deficit of $69.0bn, which would be only a marginal correction from December’s $70.3bn which was the widest since July, though still well below the record $136.0bn deficit seen in March of 2025 shortly before the tariff announcement. Despite the huge volatility in monthly trade data caused by policy changes, the average monthly deficit in 2025 of $75.1bn was almost exactly the same as that for 2024 at $75.3bn. December’s trade deficit may represent a return to normalization, implying little change in January should be expected.

Figure: GDP Growth Better But Hardly Strong?

Belatedly, some good news; the UK economy grew for a second successive month in December, something not seen for almost a year. Even more encouragingly, it may very well enjoy a further rise in the looming January data, thereby providing the best three-month showing in two years. But as is familiar with recent UK real economy data, there is a negative flip side with the positive growth rates still feeble so that the economy grew by 0.1% q/q in Q4, less than consensus and BoE thinking but matching the feeble gain of the previous quarter. Moreover, any improvement in activity and sentiment will, of course, be hit by events in the Middle East, implying that even if a base effect induced pick-up in GDP growth to 0.2% this quarter does occur, it will be fleeting. Even without the Middle East impact we were suggesting a sub-consensus 2026 GDP picture of 0.8% which now has even greater downside risks attached.

Activity in December was impaired by fresh weakness in manufacturing, utilities and construction. The data seemingly reinforced the demand worries of what now seems to be an emerging majority on the MPC; six members of the MPC appear worried about the disinflationary impact from a weak economy - four of whom actually voted for a 25bp cut at last month’s meeting.

We expect Canadian employment to increase by 50k in February, more than fully reversing a 24.8k decline in January to keep trend modestly positive. However we expect an even stronger rebound in the labor force from a decline in January to lift the unemployment rate to 6.6% from 6.5%, while remaining below December’s 6.8%. January’s 24.8k decline in employment was more than fully explained by a 66.5k decline in Ontario. January also saw a fall of 119k in the labor force, which was more than fully explained by a decline of 136k in Ontario. That January’s slippage was more than fully explained by Ontario hints at temporary factors, probably weather, which will be corrected in February, though there are risks of continued negative weather distortions in February.

We expect February’s employment gain to come fully in part time work, correcting from two straight declines, while full time work pauses after two straight strong gains. Job gains are likely to be led by components that slipped in January, notably manufacturing, education and retail/wholesale.

For the Week Ahead

UK

Released alongside monthly production and visible trade data come January GDP figures (Fri). Belatedly, and reflecting some good news; the UK economy grew for a second successive month in December, something not seen for almost a year. Even more encouragingly, it may very well enjoy a further rise in the looming January data, thereby providing the best three-month showing in two years. Indeed, we see a 0.1% m/m rise likely to be based around already-released better retail sales data, albeit offset by what may be more (vehicle-based) manufacturing weakness and possible marked drop in the housing market

But the week starts with survey data suggesting more weak labor market signs with the REC figures (Mon). Tuesday also sees BRC sales while Thursday sees what may be more soft hosing market survey data from RICS.

Eurozone

There is little of note data wise with EZ industrial production numbers due Friday, with an insight likely from German such data (Mon) and where more weakness is expected. There is an array of ECB speakers including hawk Schnabel (Wed).

Rest of Western Europe

Sweden sees monthly production and orders figures, as well as the GDP indicator (Tue) and the details of (soft) February CPI numbers (Thu). Norway sees what may be significant (for markets) CPI figures (Tue) which may see the CPI-ATE rate down to 2.9% compare to January upside surprise of 3.4% outcome, albeit still well above the Norges Bank projection of 2.6%.

USA

The calendar starts quietly on Monday and Fed officials will be quiet ahead of the March 18 policy decision. On Tuesday we expect February existing home sales to fall by 0.8% to 3.88m, which would be the lowest since October 2010. The key release of the week will be Wednesday’s February CPI, where we expect a 0.3% rise overall with the core rate ex food and energy up by 0.2%, though before rounding we expect the gains to be similar at 0.26% overall and 0.24% ex food and energy. Later on Wednesday February’s budget statement is due.

On Thursday we expect January’s trade deficit to correct only marginally lower to $69.0bn after a significantly wider December deficit of $70.3bn. We expect February housing starts to fall by 6.0% to 1.32m after a 6.2% January increase while permits fall by 5.2% to 1.38m after 4.8% January increase. Weekly initial claims are also due. On Friday we expect a strong 0.4% increase in January’s core PCE price index and a 0.6% increase in personal income. We expect January durable goods orders to slip by 0.6% but with a 0.7% increase ex transport. A revision to Q4 GDP is also scheduled, followed by the preliminary March Michigan CSI and January’s JOLTS report on labor market turnover.

CANADA

Canada’s data highlight comes on Friday, with February’s employment report. We expect a 50k increase but a rise in unemployment to 6.6% from 6.5% as both employment and the labor force rebound from January dips that were fully concentrated in Ontario. Thursday sees January data for the trade balance, building permits and wholesale sales, for which the preliminary estimate was for a 0.6% decline ex petroleum. Friday also sees Q4 capacity utilization and January manufacturing shipments, for which the preliminary estimate was for a 3.3% decline.

JP

Before Tuesday’s GDP, we have Labor Cash Earning on Monday. Wage growth has resumed above 2% and should see momentum to be continued. The data remain critical as it is the cornerstone of sustainable inflationary pressure. With headline inflation moderating, a beat in wage growth could attract speculation of an earlier hike from the BoJ and supports the JPY. The preliminary GDP data has been soft and the official release could see the numbers slightly tweaked higher. However, given the proximity to no growth, there is a slim chance Q4 GDP fall back into contraction, which will be greatly unfavorable for the BoJ. We also have household spending on the same day and should see improvement from the contracting December.

AU

Consumer confidence on Tuesday and consumer inflation expectation on Thursday are unlikely to move the Aussie by large and sustainably.

NZ

Only Business PMI on Friday.

Recap of the Week

Markets and the Iran War

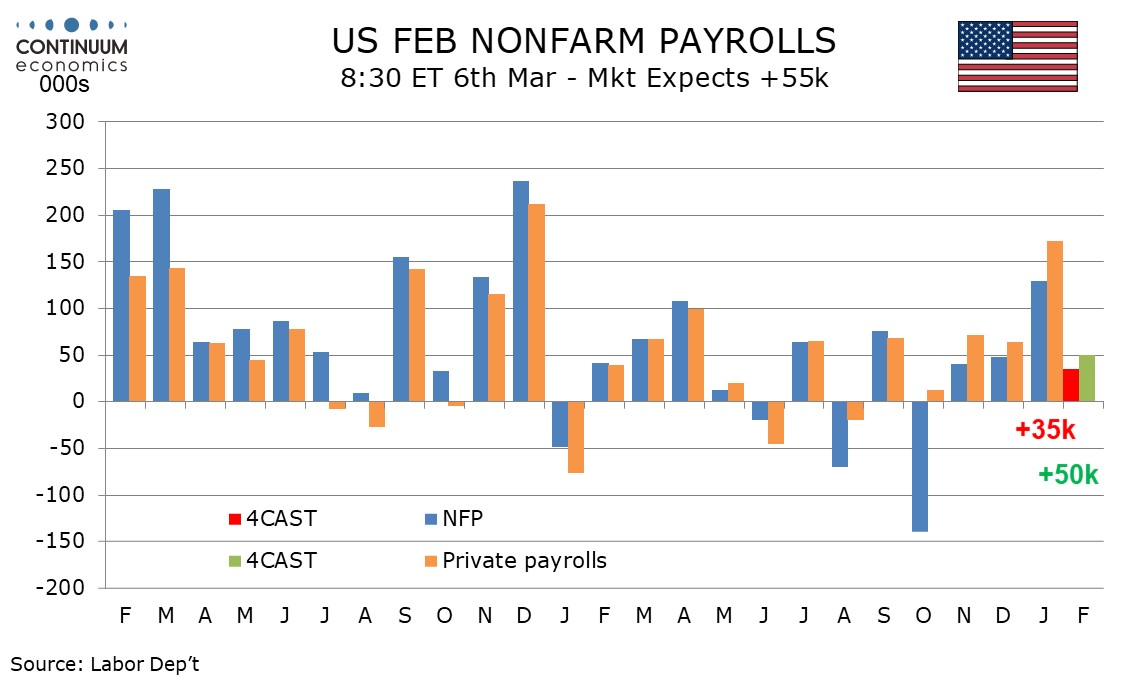

U.S. February Employment Not as strong as January

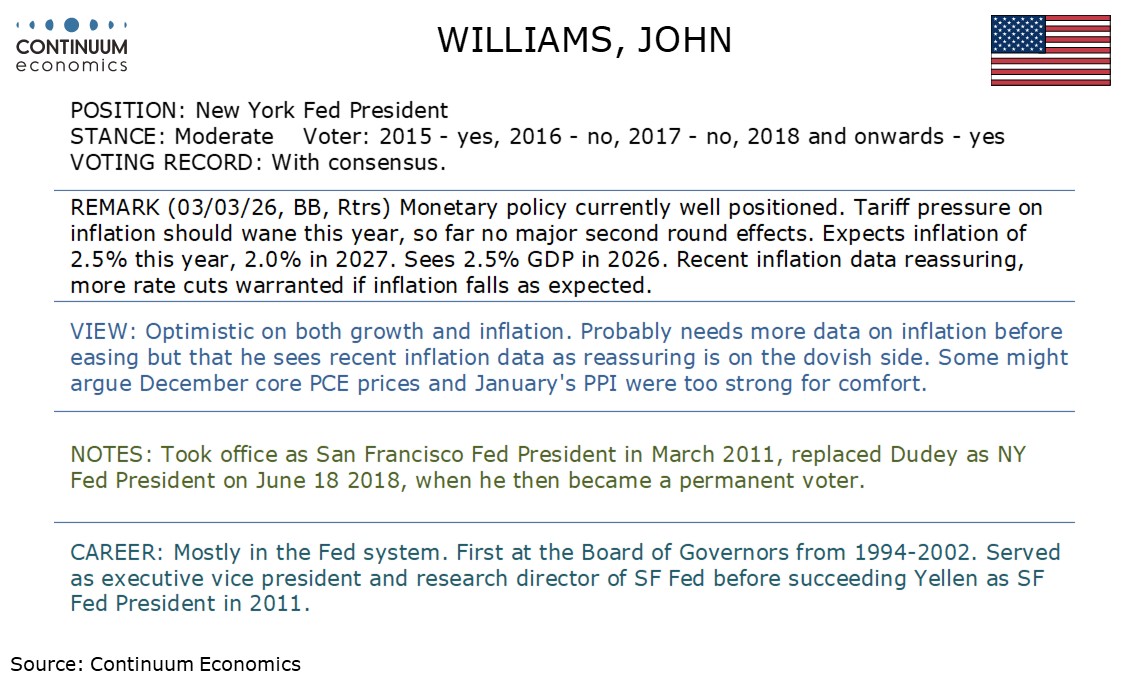

This Week's Fed Speakers

China Aims 4.5-5.0% GDP Growth

DXY Choppy in range

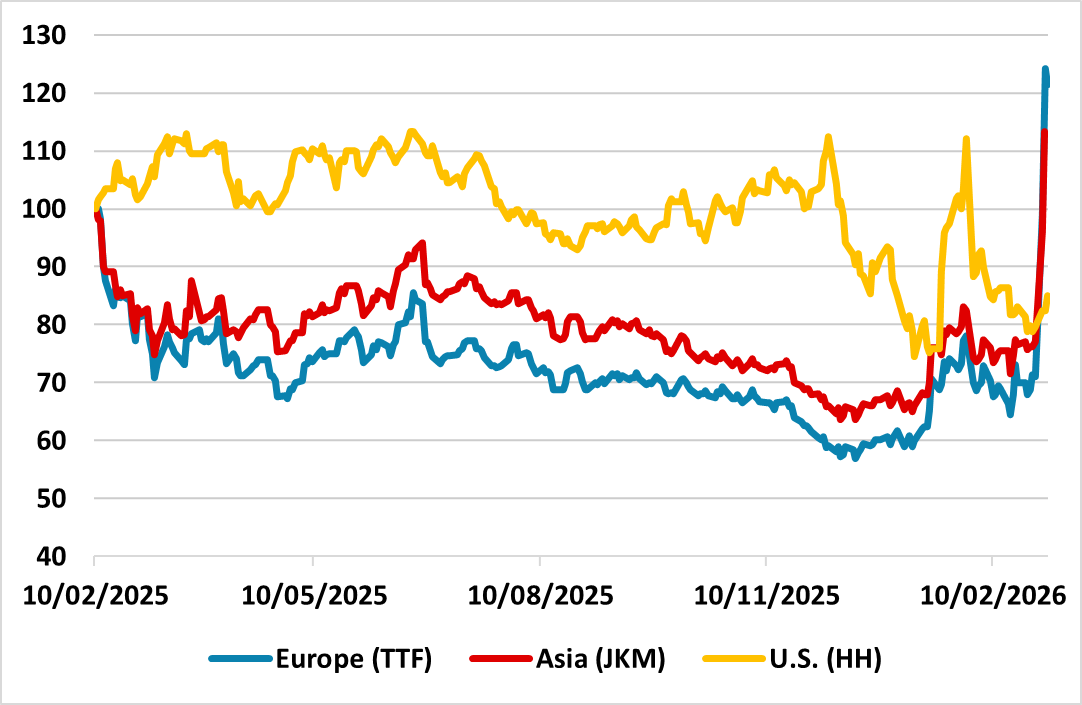

Figure: Global Gas Prices (Feb 2025 = 100)

The Trump administration’s objective appears to be pivoting from regime change to hurting Iran ballistic missile capabilities, which argues for a 2-4 week war rather than a prolonged war. However, the most intense missile battles will likely occur in the next one week and markets are hyper sensitive to oil or gas production or export facilities being hit and how long they will stop production/exports. Uncertainty also exists whether enough Gulf countries interceptor missiles exist for Iran drones. Risk off has not finished yet.

The initial reaction has been a parallel shift upwards in yield curve on fears that the inflation shock could have some 2nd round effects and mean that DM central banks (Fed and BOE) cannot cut interest rates in the coming months and that easing over the next 12 months could be smaller. However, central banks are likely to look through the increase in oil and gas prices on the view that they will be temporary and with only modest economic momentum argues against the idea of rate hikes (except those already planned in Japan and Australia). This could mean that the front-end of some DM curves attract interest in U.S./UK, especially if remaining Iran officials were to become open to the idea of restarting talks with the U.S. (the shift of view could come as early as next week, when Iran missile stocks become low and though of survival prompt regime transformation). Other traditional safe havens have been mixed with gold in favour, but the Japanese Yen out of fashion. However, the JPY has become so undervalued, that a snap higher could be seen on a worsening of the Iran war and hints that the worst could be over.

We expect February’s non-farm payroll to rise by 35k overall and by 50k in the private sector, both four month lows and significantly slower than January’s above trend respective gains of 130k and 172k. We expect unemployment to edge up to 4.4% from 4.3%, reversing a January dip, and average hourly earnings to rise by 0.3%, in line with trend. January’s strength was led by health care, which increased by 123.5k, and a significant slowing is likely in February, though the sector is still likely to fully explain February’s payroll gain, and most of that in the private sector. Revisions tend to be negative and January data may be revised lower, though probably only by around 25k, leaving the month still well above the late 2025 trend.

January’s data was supported by strongly positive seasonal adjustments, which turn negative in February. January’s data was also surveyed before some bad weather in late January, which would weigh on February data, though initial claims were back to normal in February’s payroll survey week after a bounce during the cold weather spell. A clearly negative payroll looks unlikely.

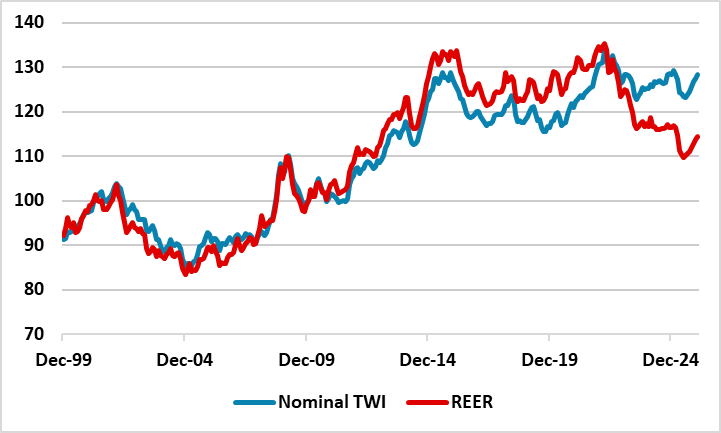

Figure: Yuan Nominal and Real Effective Exchange Rate (%)

The Yuan has continued to appreciate with no resistance from China authorities. Part of this is a willingness to allow a modest Yuan appreciation in the face of the huge China trade surplus and pressure from U.S./Europe/IMF and others over an undervalued Yuan, but appreciation is also designed to soften U.S. trade pressures and the risk of an aggressive section 301 action from the U.S. China also wants the trade truce to continue, but is reluctant to deliver Trump’s desired trade deal with China. This could make a 5% growth target difficult to achieve and a reason why China goes for a 4.5-5.0% 2026 GDP target.

China announced a central government budget deficit at 4% of GDP, which is the same as last year and points to only modest fiscal stimulus. Though investment was supported, consumption trade in programs were cut from Y300bln to Yuan250 and no new structural safety net for households have yet been announced. Consumption was the 4th priority and the 4.5-5.0% growth target is an acceptance that cyclical headwinds remain (residential property investment and modest consumption growth) and structural forces are having an impact (population aging). All of this is modest support and we see no reason to change our 4.4% GDP forecast for 2026.

USD has been favored by market participants as the go-to haven asset. It even beats Gold and JPY in the first rush of fear after U.S. strikes Iran. Going forward, as the dust settles, the greenback will likely rotate lower with market participants returning to physical haven asset, like precious metal to hedge the uncertainty. Yet, in times of turbulence, DXY could see another spike.

On the chart, the anticipated test below 99.00 has bounced from 98.67, with prices once again trading above congestion support at 99.00. Intraday studies are mixed and overbought daily stochastics are unwinding, suggesting room for further consolidation above here. But the rising daily Tension Indicator and positive weekly charts highlight later gains. Resistance is at the 99.25 Fibonacci retracement. A close above here will improve price action and extend late-January gains beyond 99.50 and the 99.68 current year high of 3 March towards congestion around 100.00. Meanwhile, any fresh tests below 99.00 should meet renewed buying interest above congestion support at 98.50.