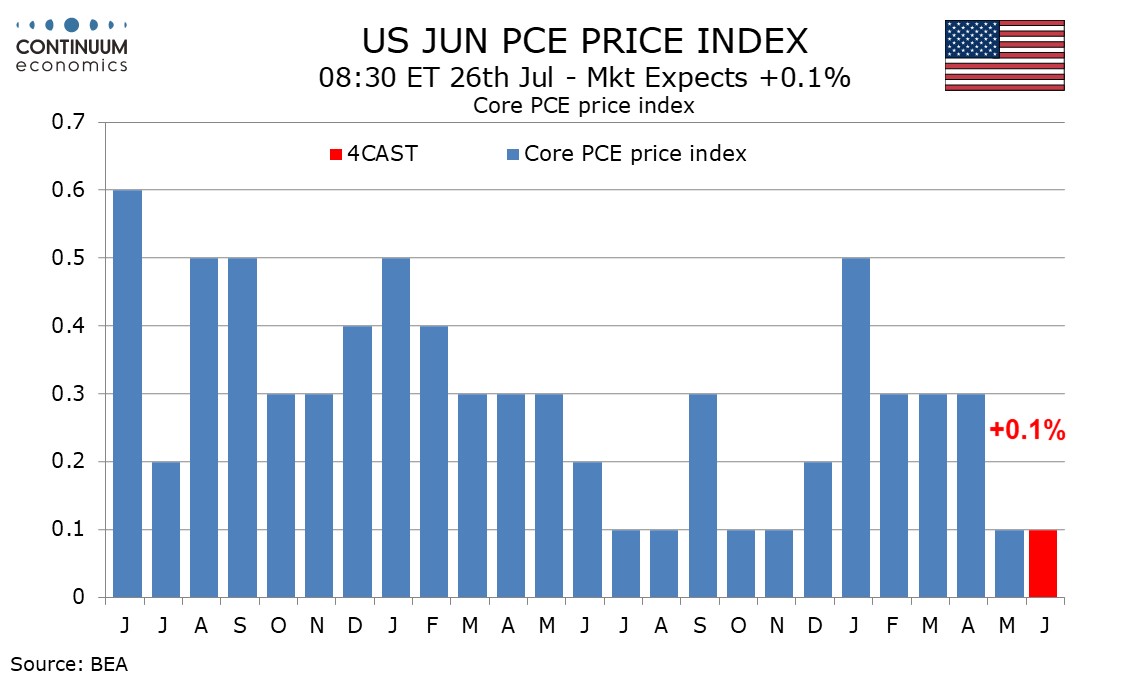

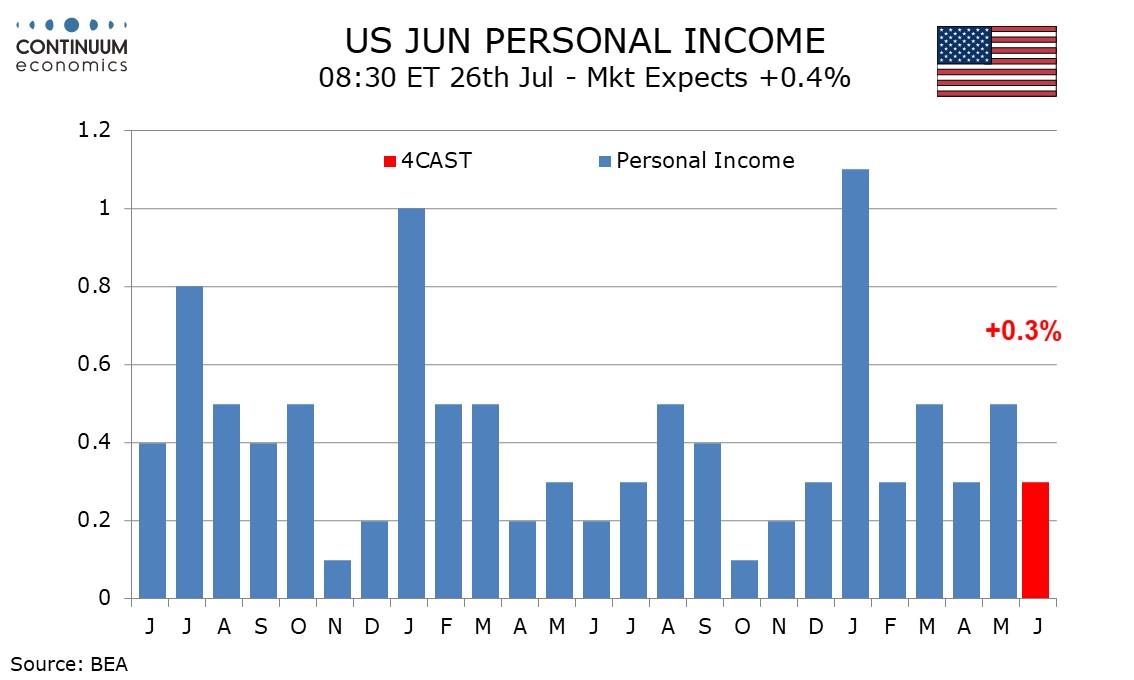

Preview: Due July 26 - U.S. June Personal Income and Spending - Another soft Core PCE Price Index

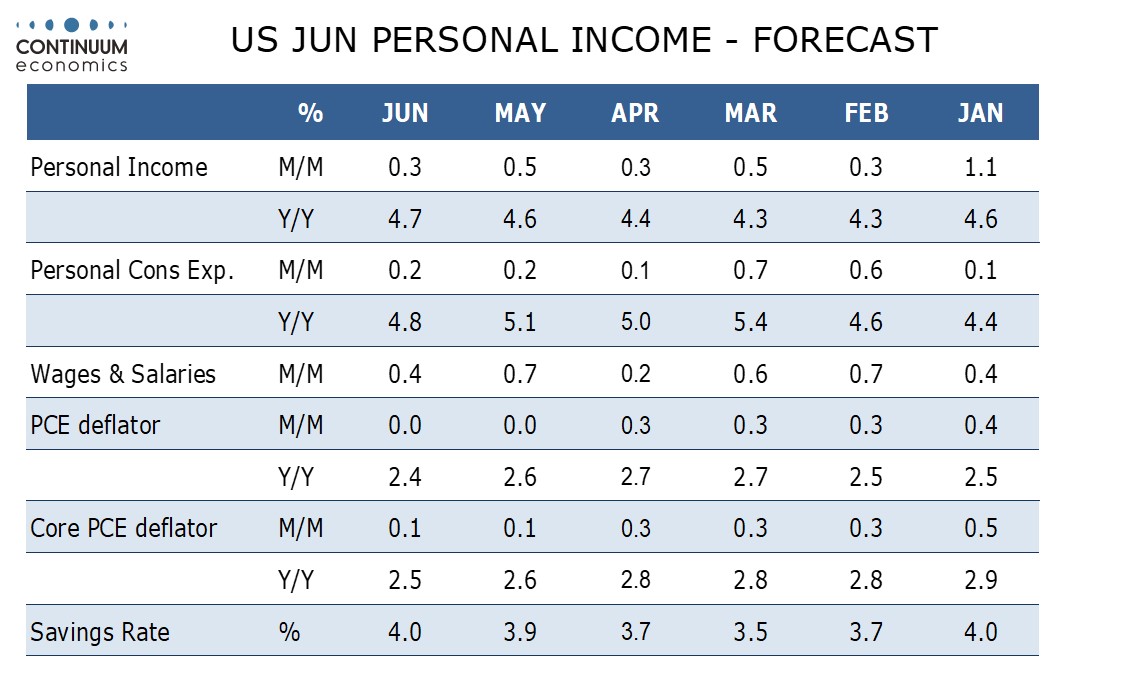

We expect a second straight 0.1% increase in June’s core PCE price index, this time consistent with June’s core CPI which followed a 0.2% increase in May. We also expect moderate gains of 0.3% in personal income and 0.2% in personal spending. The data will contain only a limited amount of fresh information, with Q2 data due in the GDP report on July 25.

June’s core CPI was below 0.1% before rounding and we do not expect the core PCE price index to be quite that soft, following May data in which core PCE prices underperformed the core CPI, but a second straight subdued outcome looks likely.

We expect overall PCE prices to be unchanged for a second straight month. This would see yr/yr PCE prices slipping to 2.4% from 2.6% with the core rate at 2.5% from 2.6%. This would be the lowest yr/yr core rate since March 2021.

We expect overall PCE prices to be unchanged for a second straight month. This would see yr/yr PCE prices slipping to 2.4% from 2.6% with the core rate at 2.5% from 2.6%. This would be the lowest yr/yr core rate since March 2021.

A slightly less strong non-farm payroll breakdown implies a 0.4% increase in wages and salaries after a 0.7% rise in May. We expect other components of personal income to continue a tendency to slightly underperform personal income, which we expect to rise by 0.3%.

A slightly less strong non-farm payroll breakdown implies a 0.4% increase in wages and salaries after a 0.7% rise in May. We expect other components of personal income to continue a tendency to slightly underperform personal income, which we expect to rise by 0.3%.

Retail sales were unchanged in June though strong outside a dip in autos and price-induced slippage in gasoline. Industry data hints at the auto dip might be slightly larger in the personal spending report. We expect a 0.4% increase in services, up from 0.3% in May which was the slowest since August 2023, leaving overall spending up by 0.3% in June.

Retail sales were unchanged in June though strong outside a dip in autos and price-induced slippage in gasoline. Industry data hints at the auto dip might be slightly larger in the personal spending report. We expect a 0.4% increase in services, up from 0.3% in May which was the slowest since August 2023, leaving overall spending up by 0.3% in June.