FX Daily Strategy: Asia, March 3rd

Broader Risk Sentiment Dominated by U.S.-Iran

Aussie May be Benefiting

EZ Goods May Soon Take Core HICP Below Target

The broader risk sentiment will be dominated by headlines between U.S.-Iran. The next focus should be on Iranian retailation. With the Supreme leader and top level military officials down, it may take a bit more time for a coordinated attempt, if any. So far, Iran has been launching missiles towards U.S. and Middle East allies but has not done significant damage. Then, risk aversion will grasp the market and will push haven asset like Gold and JPY higher.

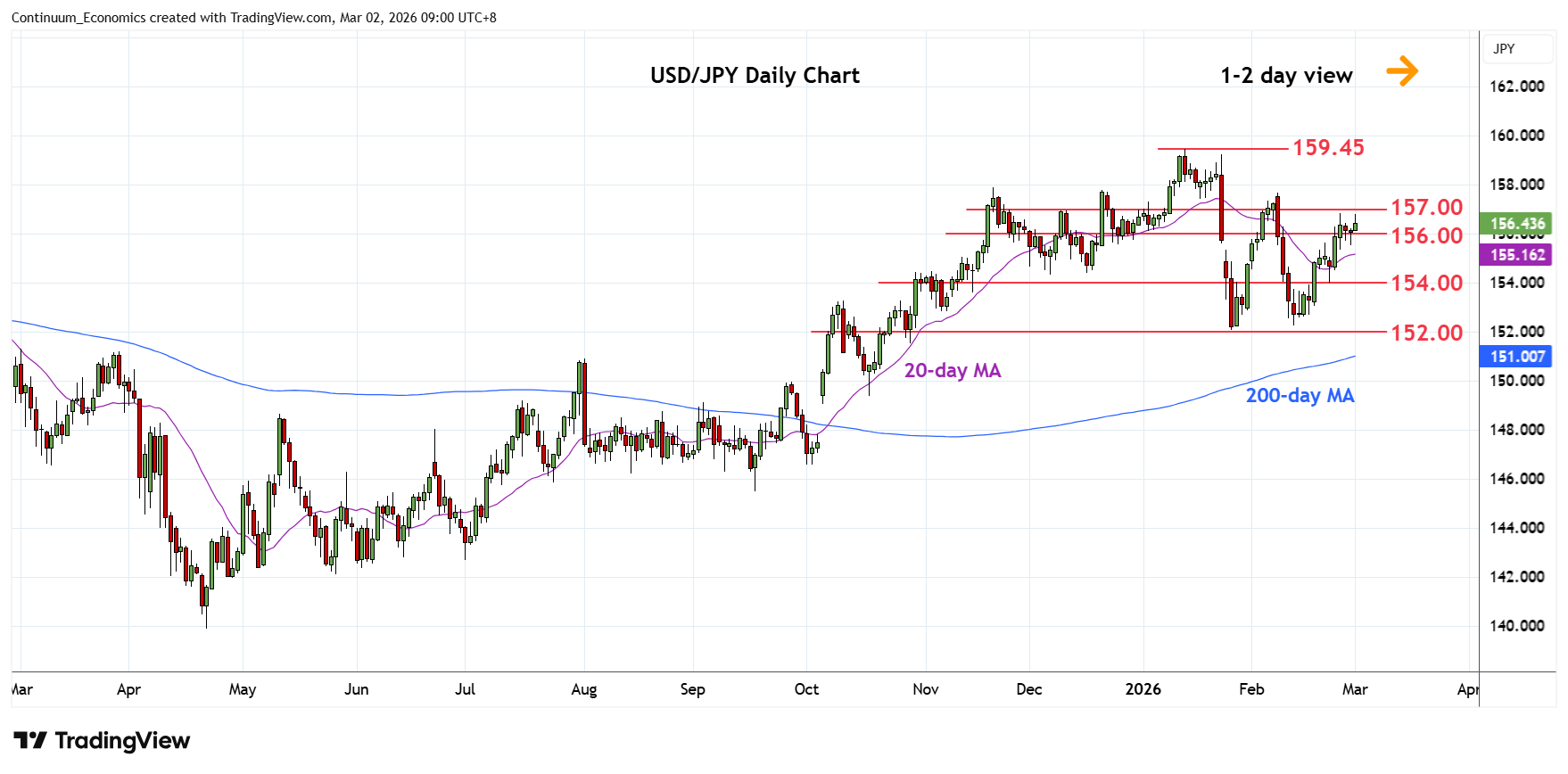

On the chart, it is firmer in range to retest 156.82 high of last week and break here will see scope to extend gains from the 152.27 low of 12 February. However, intraday and daily studies are overbought and suggest gains likely limited for now. A later break cannot be ruled out, clearance will open up room for retest of resistance at 157.65 and the 157.75/157.90 December and November highs. Meanwhile, support remain at the 156.00/155.00 congestion area which should underpin. Would take break here to to fade the upside pressure and open up room for deeper pullback.

Commodities are riding the wave of war. Gold and Oil are the outliner, with the first being haven's favorite and later being disrupted physically. The Australian Dollar maybe a benefiter as it has been rising along the precious metal for the past months. However, in case of strong risk aversion, the Aussie may be dragged by USD bids. Yet, it has not been the case without critical strikes from Iran or further escalation.

On the chart, the pair is lower at the open as prices gives way to selling pressure beneath the .7147 current year high. Pullback see room for retest of the .7015 support and break here and the .7000 level will open up room for deeper pullback to retrace recent bounce from strong support at the .6900 level. Meanwhile, resistance at the .7100 congestion and extending to the .7147 high is expected to cap. Would take break here to extend the bull trend from the April low.

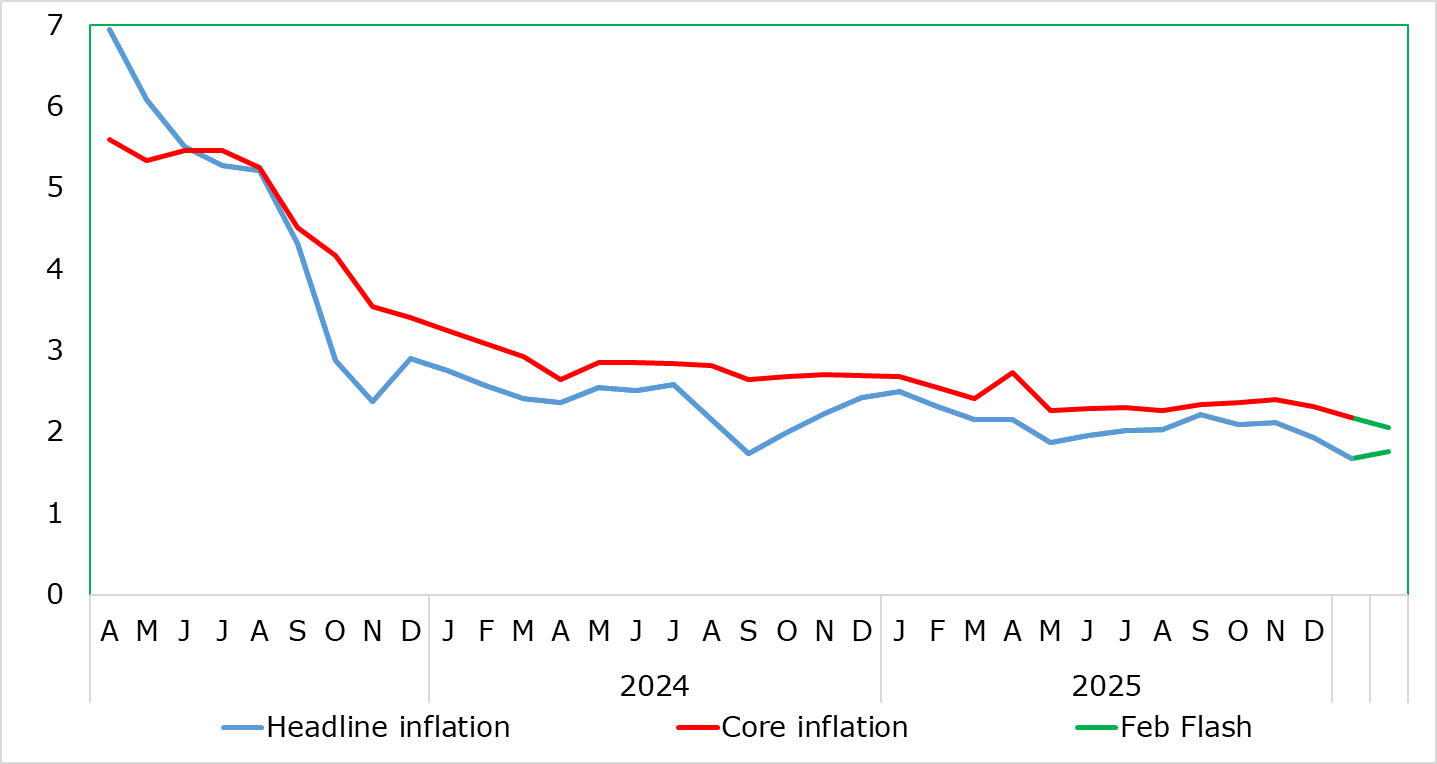

Figure: Headline and Core Converge?

Having dropped to 1.7% in the January data, thereby matching expectations and the short-lived Sep 24 outcome, it is possible that the headline HICP rate may not be any lower through this year and into next. Indeed, we see the headline rate edging up to 1.8% in the February flash mainly due to energy. But the core could drop another notch from January’s 2.2%, that being the lowest in over five years and hinting at a clear undershoot of the ECB’s Q1 2026 projection. Partly this reflects a further slowing in services inflation, but also even weaker non-energy goods prices (NEIG). To a large extent, this expected fall in the latter reflect softer import prices. But while inflation is not much of an issue for the ECB given its proximity to target, more weakness in services allied to possibly NEIG inflation may cause fresh concern at the ECB is (as we forecast) it soon results in core inflation undershooting target.

As of the January numbers updated today, several methodological changes take effect in the HICP. Over and beyond the usual annual reweighting of the components, the index will also now be compiled according to the new classification. What is clear is that with (hitherto relatively resilient) services now having seen an increase in its weighting in the last four years this has acted to push up recorded overall inflation. Admittedly, this reweighting has not prevented the fall in services inflation in the last few months, instead reflecting weak demand paring back the ability of companies to raise prices, particularly those typically made at the start of each year!