FX Daily Strategy: Asia, July 16th

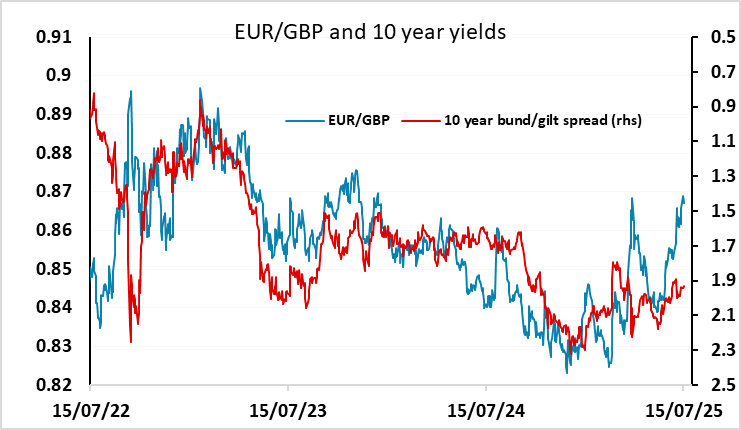

GBP risks to the upside on UK CPI...

…although longer term trend remains negative

USD strength continues, with the JPY the main victim

Strong equities underpin JPY weakness, and there is no obvious trigger for a turn despite overvaluation

GBP risks to the upside on UK CPI...

…although longer term trend remains negative

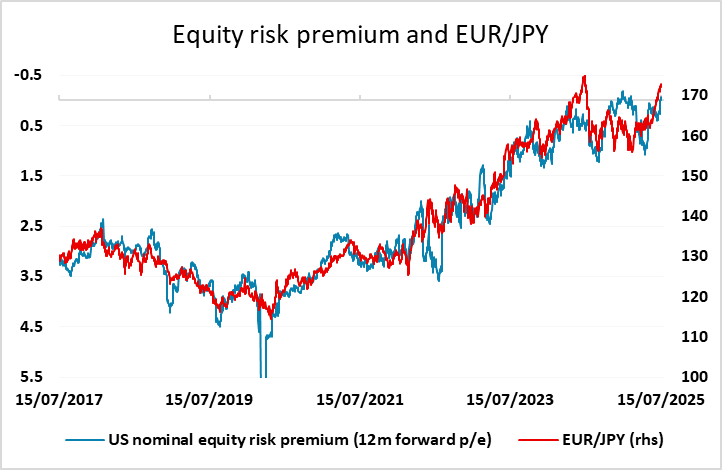

USD strength continues, with the JPY the main victim

Strong equities underpin JPY weakness, and there is no obvious trigger for a turn despite overvaluation

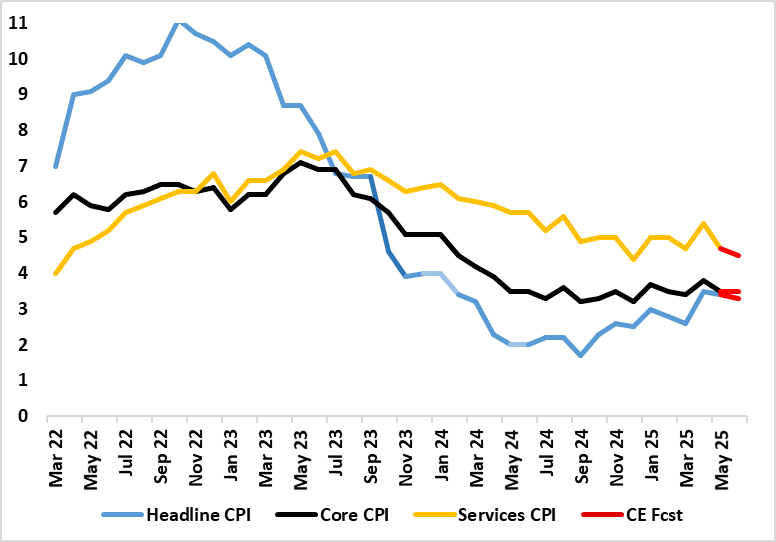

UK June Inflation to Slip Only Slightly

Source: ONS, Continuum Economics, % chg y/y

Wednesday sees UK CPI data to kick off the European session and US PPI and industrial production data in the afternoon. The market consensus has UK CPI staying at 3.4% with core at 3.5% - numbers that look too high to encourage any increased expectations of an August policy rate cut from the Bank of England. An August cut is already 87% priced into the market, so the risks seem weighted towards the market losing confidence in a cut if the CPI data comes in higher than expected. Rate cut expectations are based on real economy and labour market weakness, but food prices, amid what may be a poor UK harvest, may be a growing concern for the BoE both for its impact of spending power and on inflation. Inasmuch as any strength in inflation is related to higher food prices, it provides less of an argument against easing that strong service price inflation would.

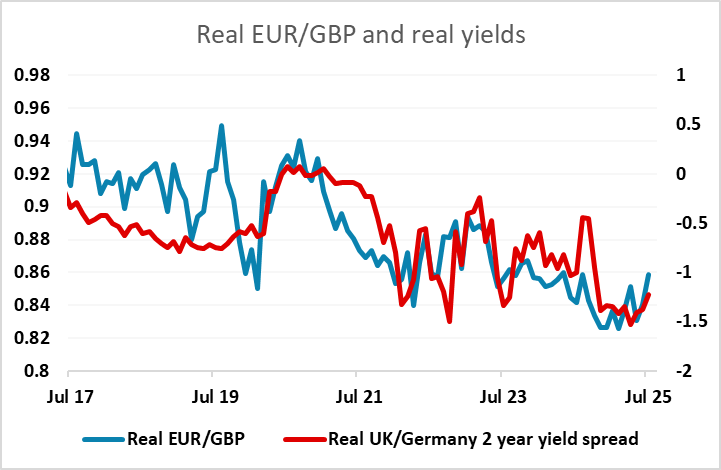

GBP has been weak in recent sessions as the market has priced in more easing in response to weaker wage data and some dovish BoE commentary. EUR/GBP may be running a little ahead of the move in yield spreads, but not much when real yields and the real exchange rate are taken into account. From a big picture perspective, we still expect EUR/GBP to move above 0.90 in the coming year or so as UK and Eurozone real policy rates converge. However, for Wednesday, the risk may be slightly on the GBP upside on the data.

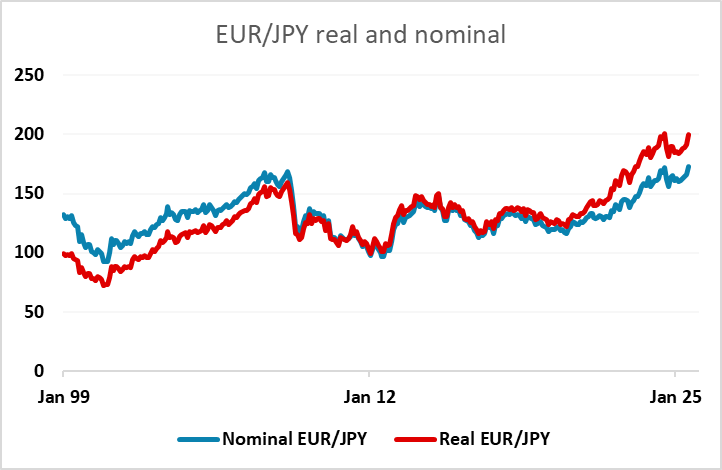

The US data shouldn’t be of any great significance after the softer than expected CPI data on Tuesday. Despite the softer data, US yields rallied after an initial dip and helped propel the USD higher across the board, helped by a strong US equity market supported by some positive earnings numbers from banks. The JPY continues to be the main victim of the USD recovery, helped by the positive equity tone and the continuing decline in equity risk premia implied by the combination of higher yields and higher equities. We are now in the eighth consecutive week of EUR/JPY gains, and the all time high of 175.42 from July last year is under threat. It continues to look like a turn lower in equities will be required to halt JPY weakness, and there is currently no obvious trigger for this, although equities are increasingly overvalued.

However, the USD was also generally stronger on Tuesday, bolstered by positive equity sentiment and a general belief that the tariff increases aren’t going to derail the US economy. The modest feedthrough so far is part of the reason for this, but there is also a general belief that the threatened tariffs against the EU and Mexico will in the end be well below the threatened 30%. Evidence that tariffs are being negotiated lower may even be seen as a reason for further equity market strength. We continue to expect a major equity correction come the autumn, as the current level of the market prices in above trend growth which, even without the threat of tariffs and the existing evidence of slowdown, would make little sense in an economy that is already at near full employment. But, as Keynes said, the market can stay irrational longer than you can stay solvent, so at the moment opposing the positive trend is only for those with deep pockets.