FX Daily Strategy: Europe, February 22nd

PMIs the focus on Thursday

Eurozone PMI needs to rise to support recent firmer EUR tone

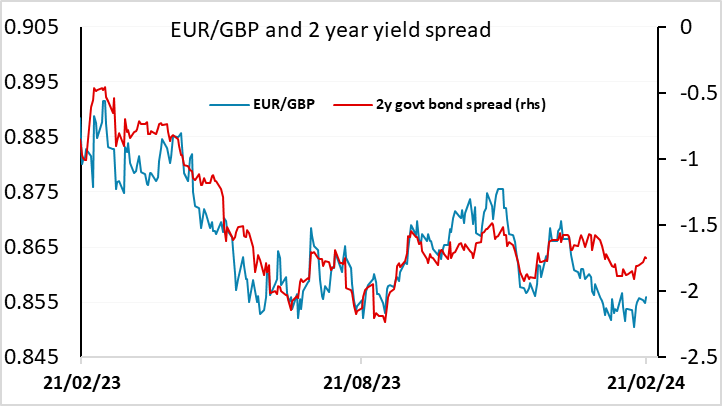

Spread between the UK and Eurozone important for EUR/GBP

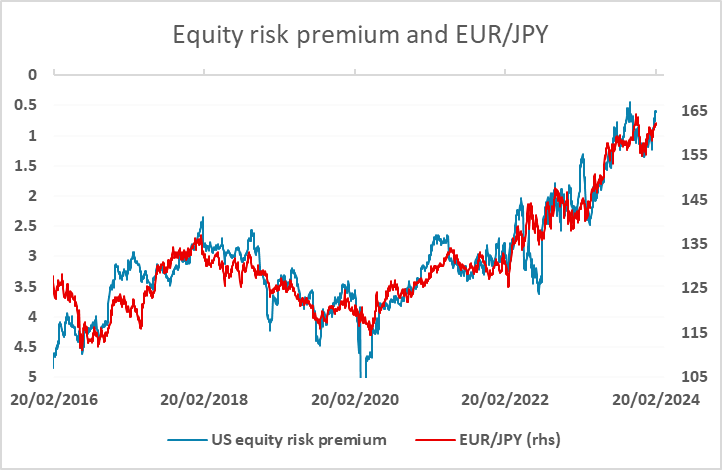

EUR/JPY remains supported while global yields rise

PMIs the focus on Thursday

Eurozone PMI needs to rise to support recent firmer EUR tone

Spread between the UK and Eurozone important for EUR/GBP

EUR/JPY remains supported while global yields rise

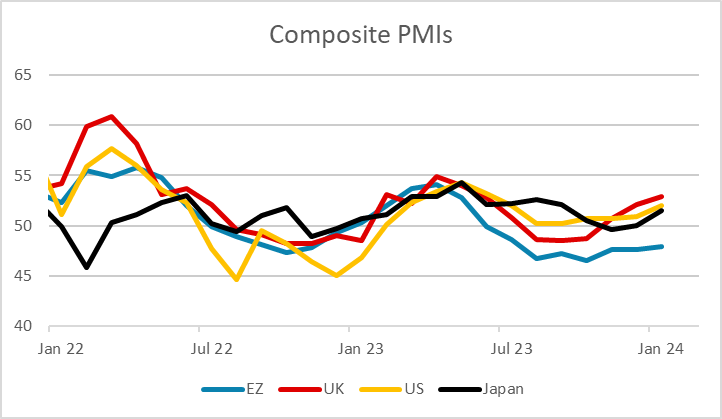

Thursday is PMI day, and after a dearth of data so far this week, we can expect the PMIs to be the prime focus of market attention. Recent PMI data has been a source of some optimism, with composite PMIs turning higher in most of the major economies in the last few months. The Eurozone has been the main underperformer, and the Eurozone and UK numbers usually garner the most attention. The mildly positive EUR/USD tone in recent days has been due to positive risk sentiment more than any real optimism about the Eurozone economy, and some support from a rise in Eurozone PMIs may be necessary to sustain the positive EUR/USD bias.

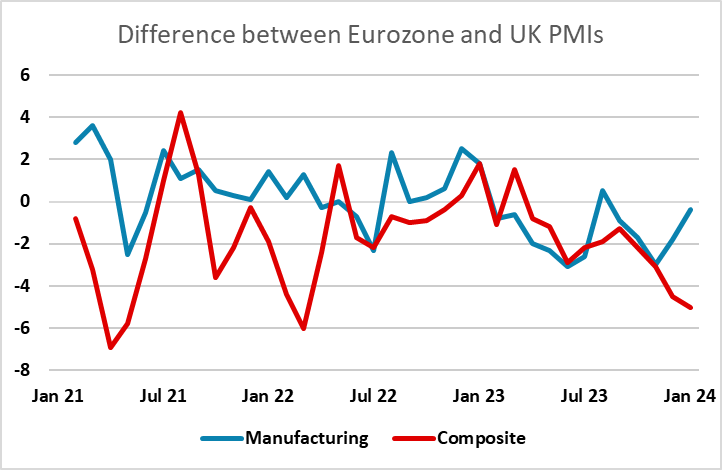

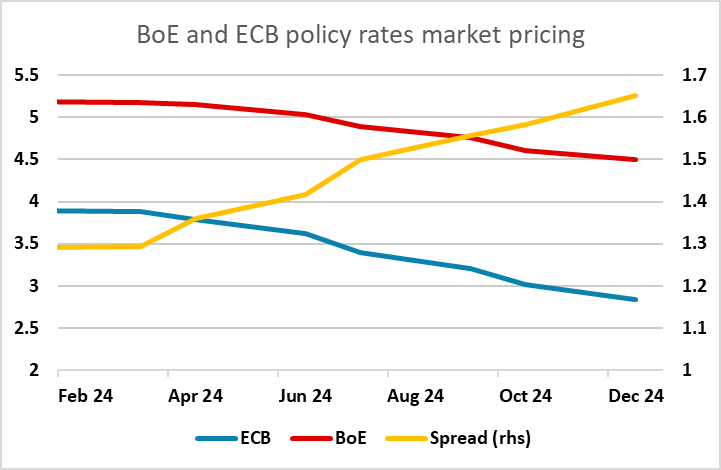

The difference between the UK and Eurozone composite PMIs in January was the largest since May 2021, but the divergence between the two in Q4 wasn’t mirrored in the growth numbers, with UK GDP underperforming with a fall of 0.3% in the quarter. While studies suggest that the Eurozone PMIs are a reasonable contemporaneous growth indicator, it is less clear that this is the case for the UK. It is both hard to see a rationale for UK outperformance, and unusual for it to persist for very long. We see some downside risks for GBP in any case, with much less BoE easing than ECB easing priced in, and EUR/GBP in any case trading some way below the level implied by yield spreads.

There is little else on the calendar that is likely to move markets, but Wednesday was another day that saw the JPY fall back on the crosses, with EUR/JPY hitting another post-November high. Strong European equity market performance looks to have been behind this as much as anything, combined with the low vol conditions that have generally favoured the high yielders. The uptrend in EUR/JPY continues to be supported by declining risk premia, and this trend is most likely to be halted by yields turning lower in the US and globally rather than equities falling back. In either case, weaker PMIs look to be needed to halt the EUR/JPY uptrend.

In the US there is likely to be more interest in the jobless claims numbers than the PMIs, with the US market still tending to be more focused on the ISM survey. Thursday’s weekly initial claims data will cover the survey week for February’s non-farm payroll, and after the strong January employment report, the market will be on watch for evidence of any slowdown. At this stage, a rising bias in US yields looks likely to persist in the absence of weaker data, which should be USD supportive albeit primarily against the lower yields.