FX Daily Strategy: Europe, March 18th

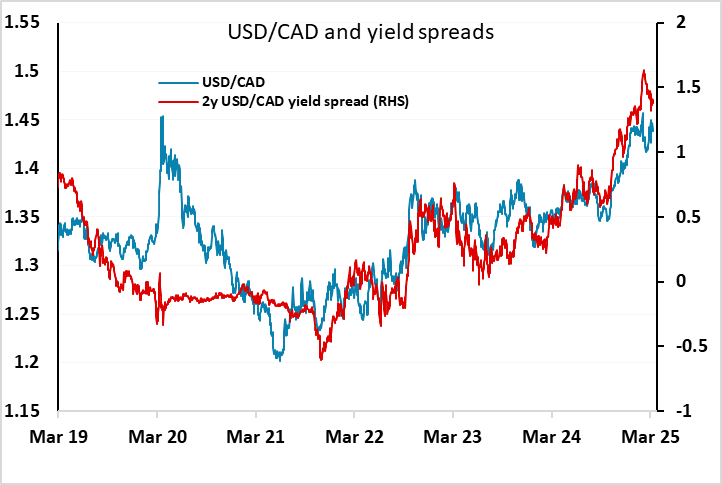

CAD more focused on policy than CPI

USD remains generally soft

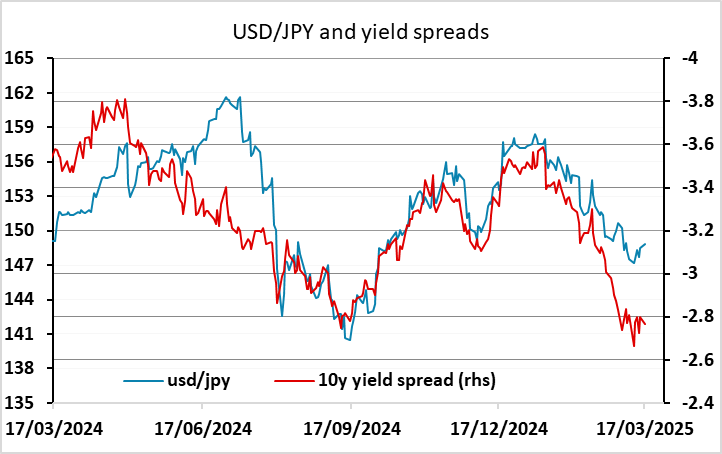

JPY still looks to have the most potential for gains

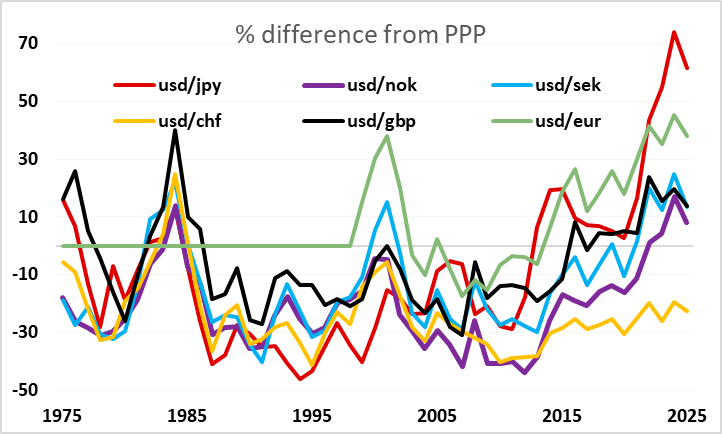

NOK may be starting big picture recovery

CAD more focused on policy than CPI

USD remains generally soft

JPY still looks to have the most potential for gains

NOK may be starting big picture recovery

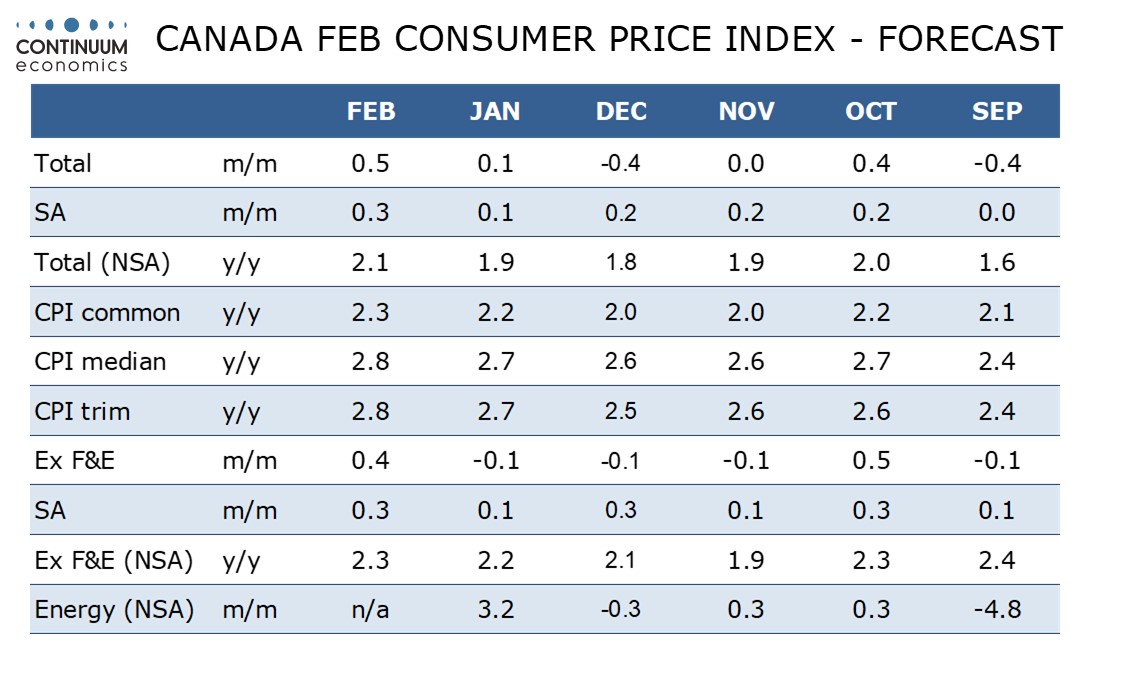

Canadian CPI and US housing starts and industrial production are the main data releases due on Tuesday. We expect Canadian CPI to increase to increase to a 7-month high of 2.1% yr/yr from 1.9% in January. We also expect the Bank of Canada’s core rates to move higher, moving further above the 2.0% target. A sales tax holiday which ran from mid-December through mid-February will start to unwind in this report. The holiday depressed CPI less than was expected, probably because of CAD weakness, but its ending still means upside risk in February and March. Our forecasts for the core rates are slightly above market consensus, but the market median is also for a 2.1% headline rate.

For the CAD, there is less focus on this data than there might have been before the US imposition of tariffs. BoC policy is now less likely to be focused on the minutiae of current inflation trends and more concerned with the impact of tariffs – both US and Canadian – on future inflation and growth. Macklem’s comments after the last BoC meeting suggested that the BoC see risks in both directions for rates, with higher inflation likely to be accompanied by significantly weaker growth – perhaps even recession. So it’s unlikely we will see market pricing move far on the back of the CPI data. USD/CAD remains a little below the level suggested by current yield spreads, and with the market still pricing in more Fed than BoC easing over the rest of this year, the risks from a yields spread perspective may be to the USD/CAD upside. But the USD is also showing some general weakness, and if this continues the CAD should at least hold its own. For now, USD/CAD moves look more likely to depend on general USD sentiment, determined by the US economic data and expectations about the impact of tariffs, than the CPI data.

The US housing starts and industrial production data are unlikely to have much impact, with the housing numbers very much impacted by the weather. The USD remained generally under pressure on Monday, with the riskier currencies outperforming helped by a better equity market tone, but there was also a generally lower yield profile in the US and Europe, and this suggests that the JPY is still likely to outperform.

On the day, one of the best performers was the NOK, and it does look as if the NOK weakness seen through 2024 is starting to reverse on a broad front. The weakness over the last year is most obvious in NOK/SEK, which failed to recover despite rising yield spreads. However, from a bigger picture perspective, CHF/NOK looks the most clearly out of line, as this is up 150% (!) since the beginning of 2008, and 70% in real terms over the same period. While the NOK was certainly expensive in 2008, so was the CHF. The CHF is still expensive now, but there is little fundamental reason to prefer it to the NOK.