U.S. Initial Claims stable but Continued Claims moving higher

Today we saw the non-farm payroll for September, as well as eight weeks of initial claims that take us to the survey week for November’s non-farm payroll. Initial claims remain low, though continued claims have been rising in recent weeks, hinting at downside risks for non-farm payrolls in October and November.

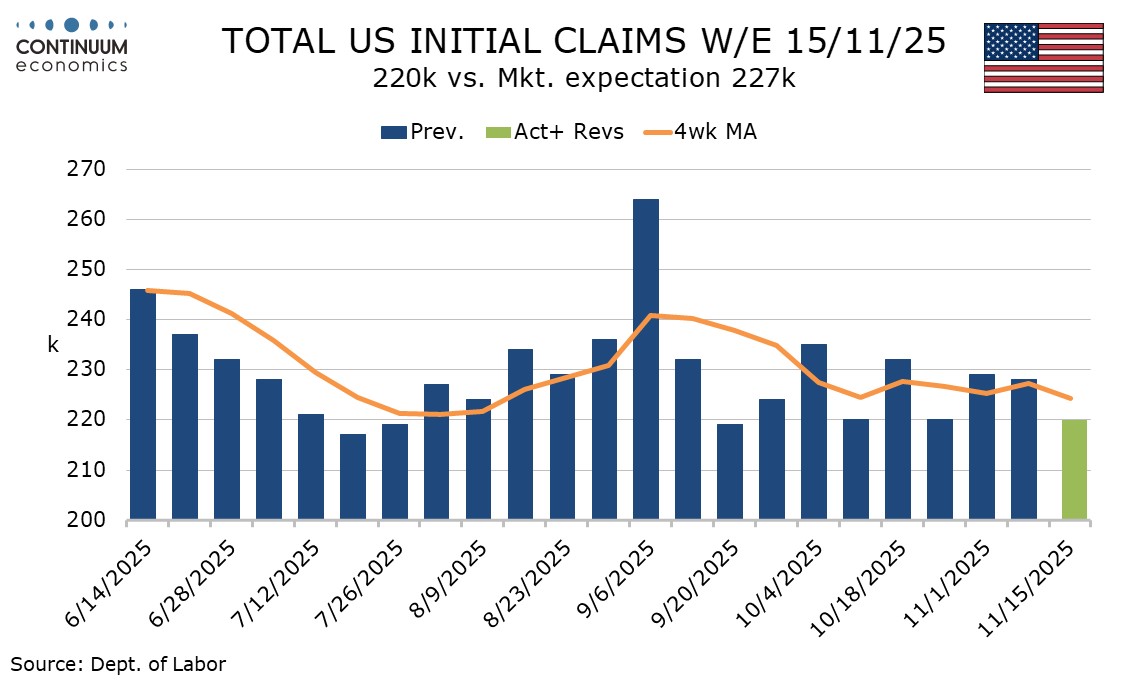

Initial claims at 220k in the week to November 15 are very similar to a 219k seen in the week to September 20, the last release before the government shutdown. Both those releases are on the low side of trend, with the high in the last eight weeks being 235k in the week to October 4.

The 4-week average in November’s payroll survey week is 224.25k, almost unchanged from 224.5k in October’s. This is lower than the 240.25k seen on September’s survey week though that was inflated by one particularly high week. The 4-week average in August’s payroll survey week was 226k.

While initial claims have been very stable, continued claims, which in the last available release for September 13 at 1.916m were at their lowest since May have since risen to 21.974m, the highest since April, covering the week to November 8, one week before the latest initial claims data. Falling continued claims into mid-September did coincide with a stronger September non-farm payroll, so the rise in continued claims since then can be seen as a negative signal. Both October’s and November’s non-farm payrolls will be released on December 16.