Published: 2024-12-17T15:35:33.000Z

Preview: Due December 19 - U.S. Final (Third) Estimate Q3 GDP - Marginally stronger still

1

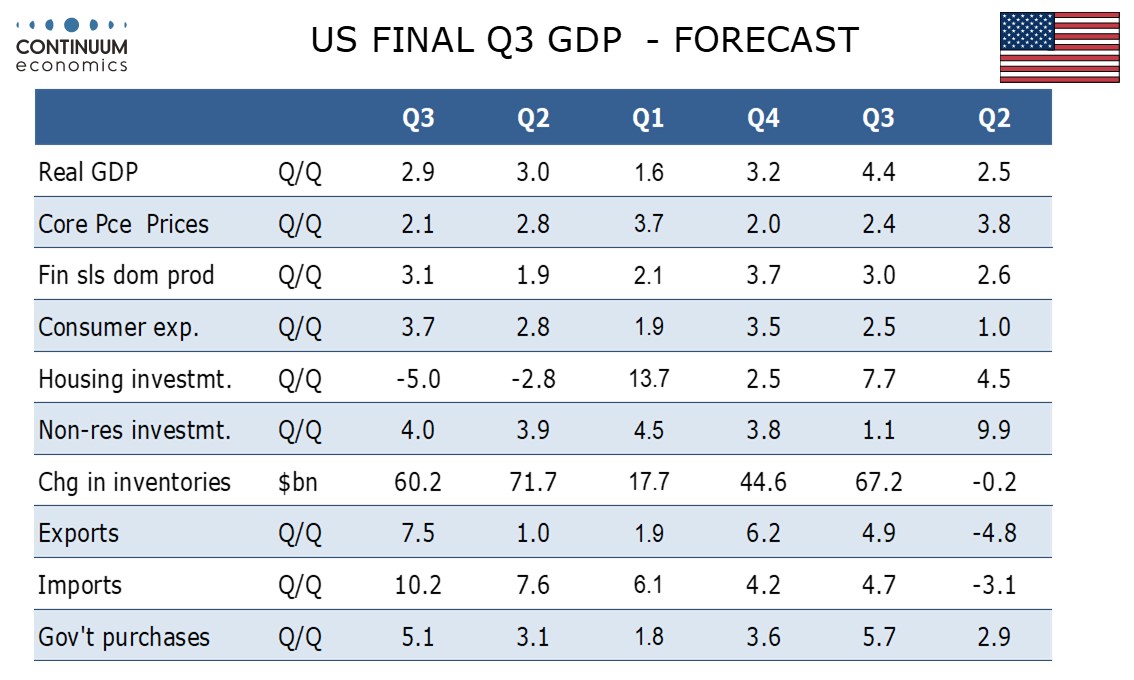

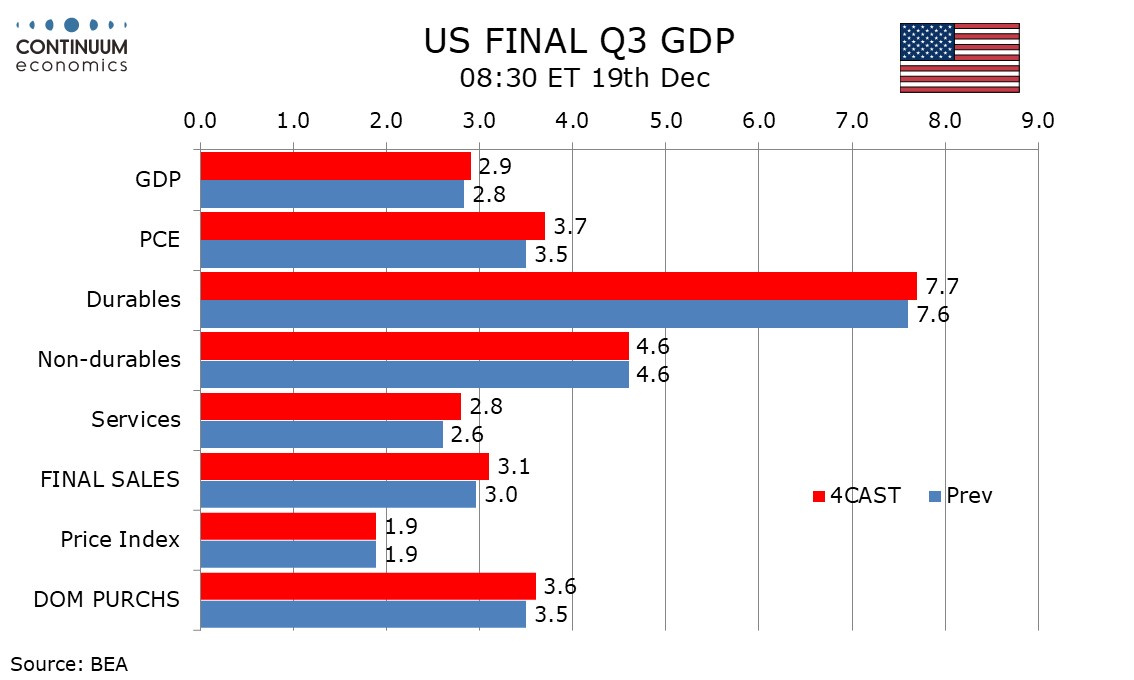

We expect a marginal upward revision to 2.9% in the third (final) estimate of Q3 GDP from an already healthy second (preliminary) estimate of 2.8%.

The upward revision is likely to be led by consumer spending, particularly services, with a modest contribution from retail.

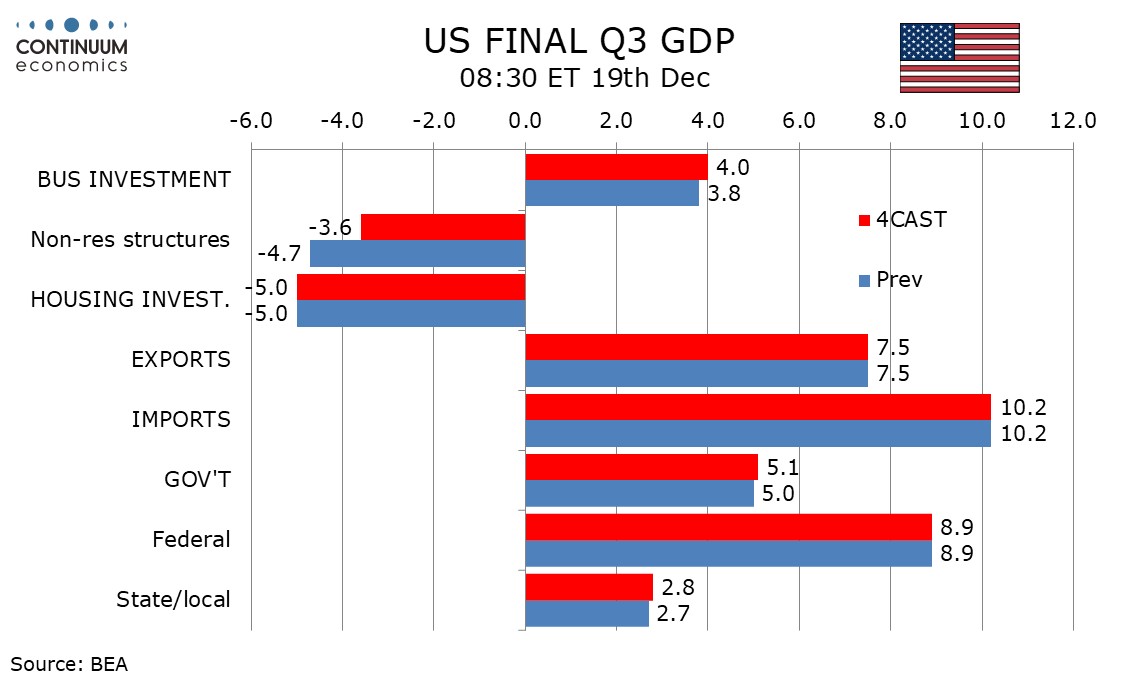

Upward revisions are also likely in non-residential construction, both private and public, but this will be partially offset by a downward revision to inventories.

We do not expect any revisions to the price indices, of 1.9% for GDP, 1.5% for PCE prices and 2.1% for the core PCE price index.