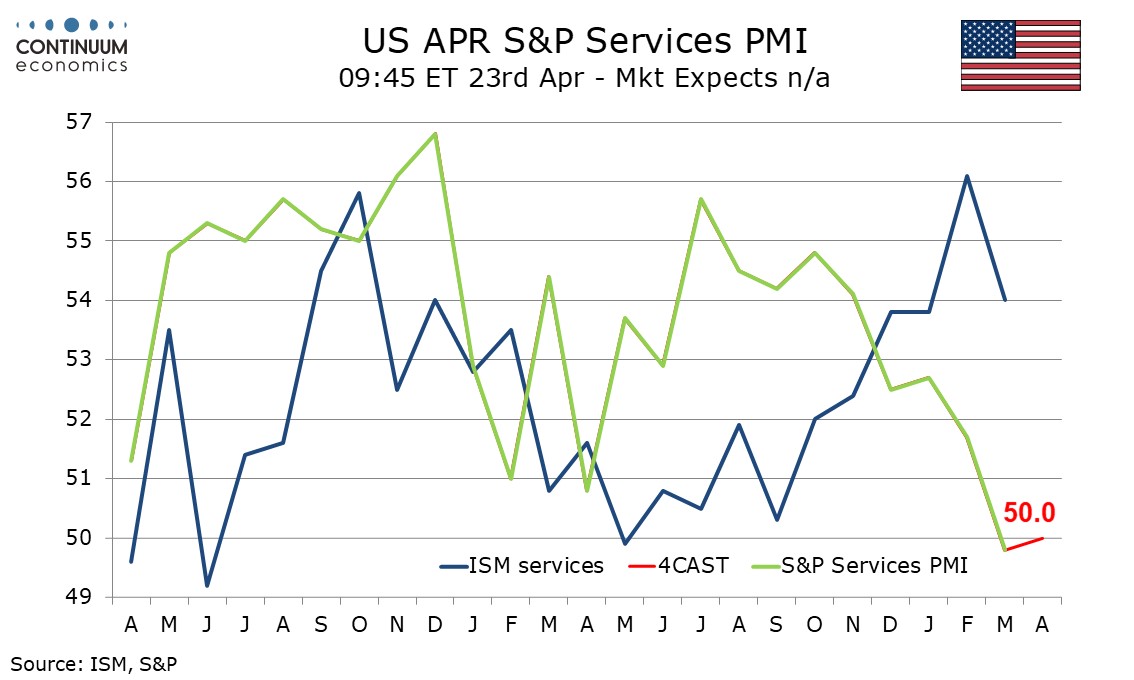

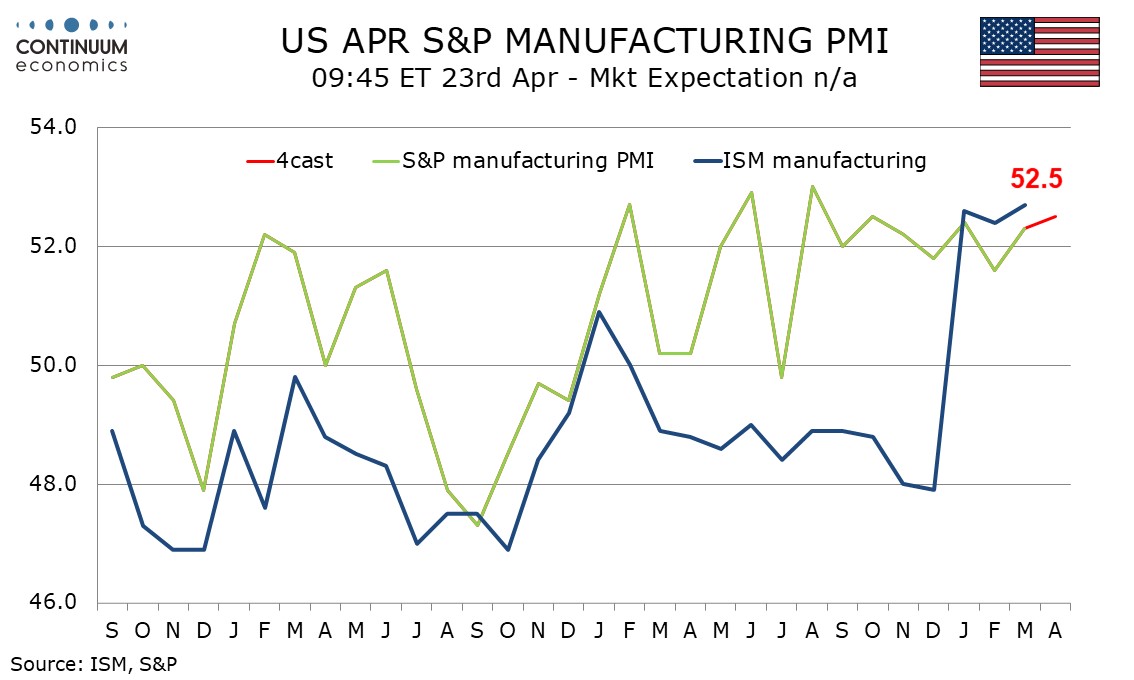

Preview: Due April 23 - U.S. April S and P PMIs - Slightly firmer despite Middle East risk

We expect modest increases in April’s S and P PMIs, manufacturing to a healthy 52.5 from 52.3 and services to a neutral 50.0 after March’s 49.8 fell below neutral for the first time since January 2023.

Improved Empire State and Philly Fed manufacturing surveys in April are positive signals for S and P manufacturing, though March manufacturing output lost a little momentum, contrasting strong ISM data. The scale of the ISM’s Q1 improvement may be a little overstated, but the S and P’s manufacturing index has been stable at a healthy level for significantly longer, and looks set to remain solid in April despite the risks coming from the Middle East.

The S and P services index probably sees more risk than manufacturing from the situation in the Middle East, with consumers already having looked vulnerable even before the gasoline price surge. However, we feel a stabilization near neutral is more likely than a further move into negative territory. The slowdown in the S and P services index has significantly underperformed ISM services data, though the two series are not well correlated.