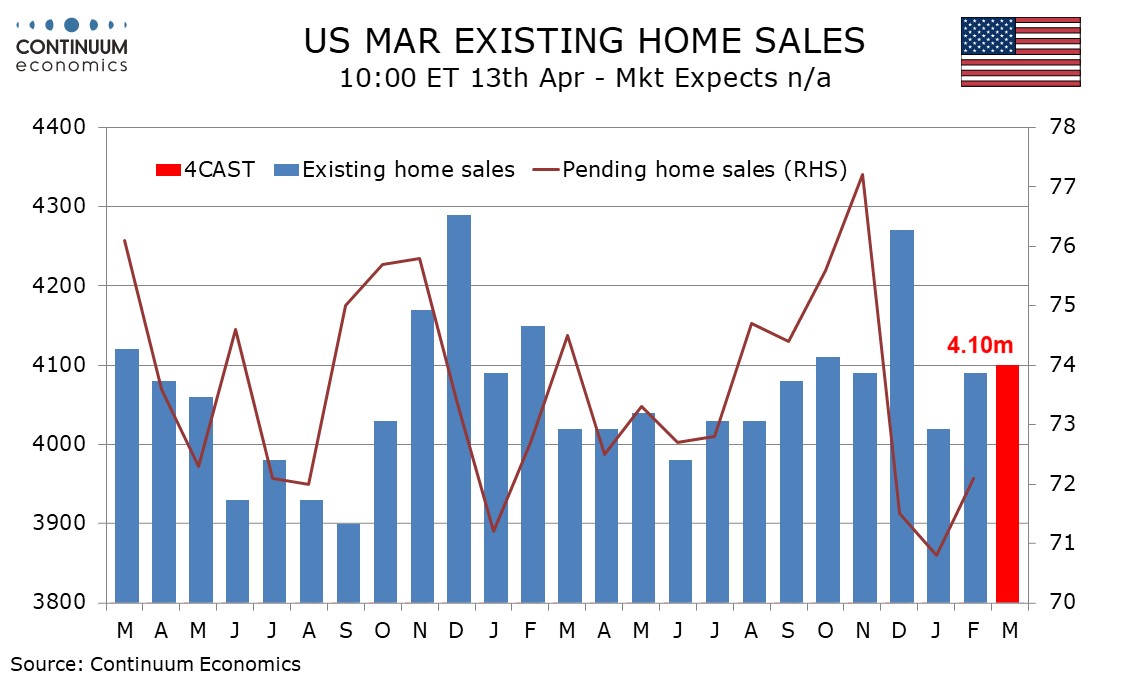

Preview: Due April 13 - U.S. March Existing Home Sales - Trend near flat, downside risk in Q2

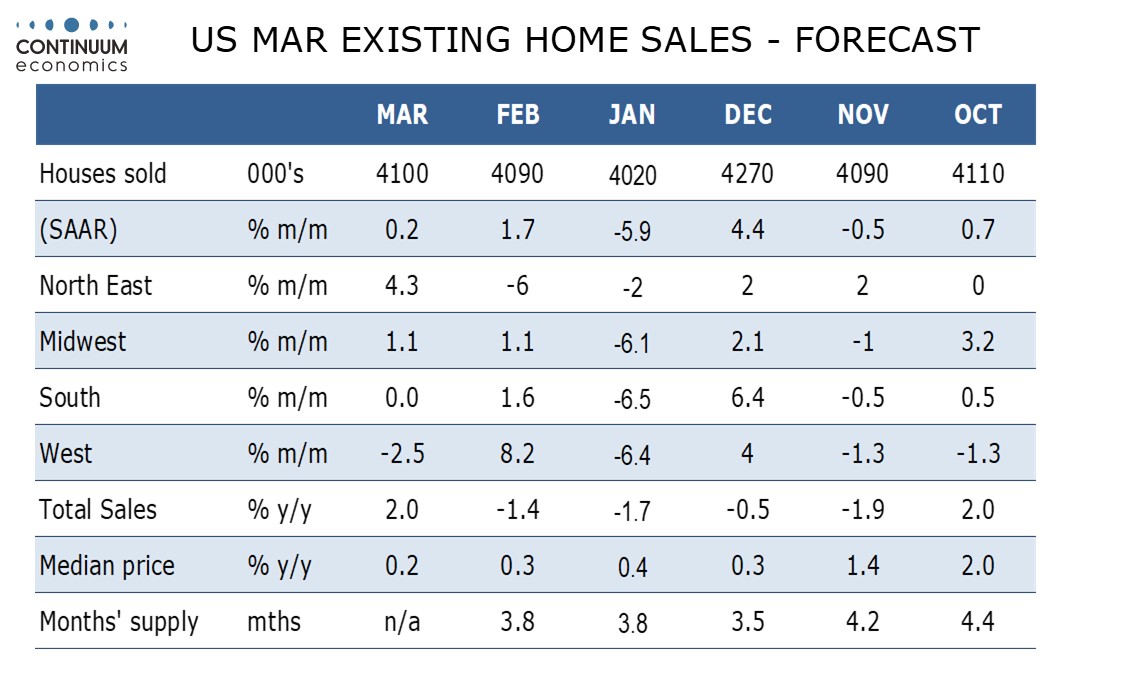

We expect a marginal 0.2% increase in March existing home sales to 4.10m leaving trend with little direction. Going forward, the Iran war poses downside risks in Q2, depending on its duration.

This level would be similar to October and November as well as February, if slightly below the average of December’s stronger 4.27m and January’s weaker 4.02m.

Pending home sales picked up from a record low in February but do not imply much upside for March existing home sales. March survey data from the NAHB and MBA showed marginal improvement, but the weekly MBA data lost momentum later in the month, possibly related to rising mortgage rates as the Iran war fueled inflation and Fed policy concerns.

We expect sales to pick up in the Northeast and Midwest assisted by improved weather but to slip in the West in a correction from a strong February increase. We see sales unchanged in the South, the largest region. We expect a 1.5% monthly rise in the median price but this will be seasonal. Yr/yr growth would then slip to 0.2% from 0.3%, leaving it little changed for four straight months.