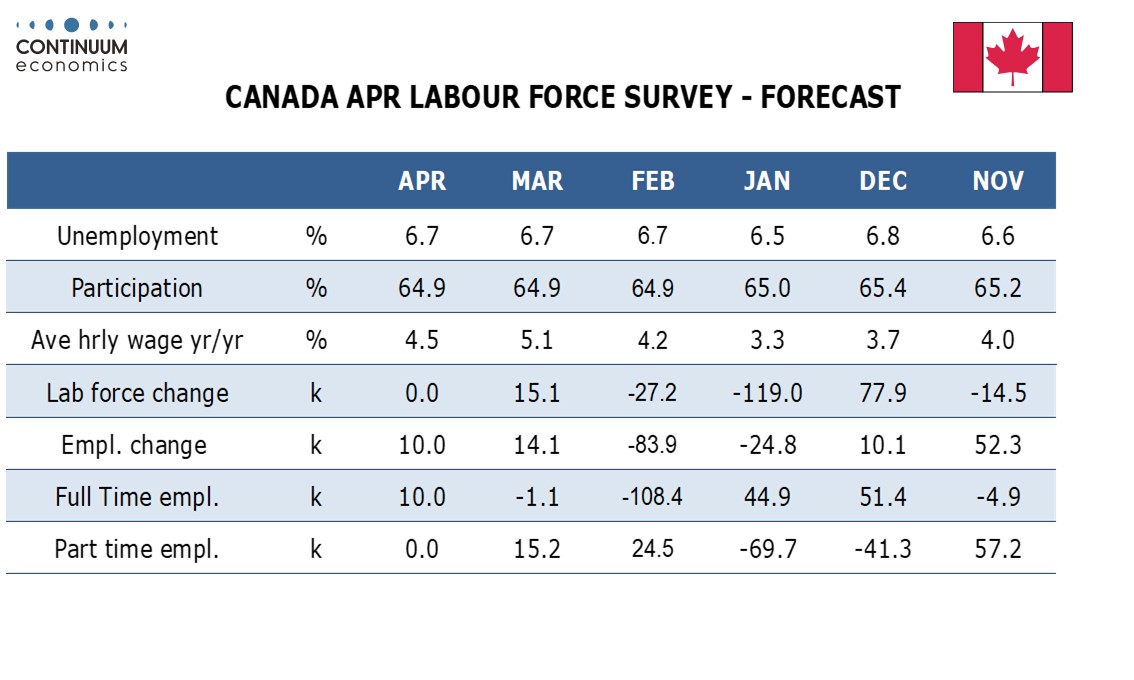

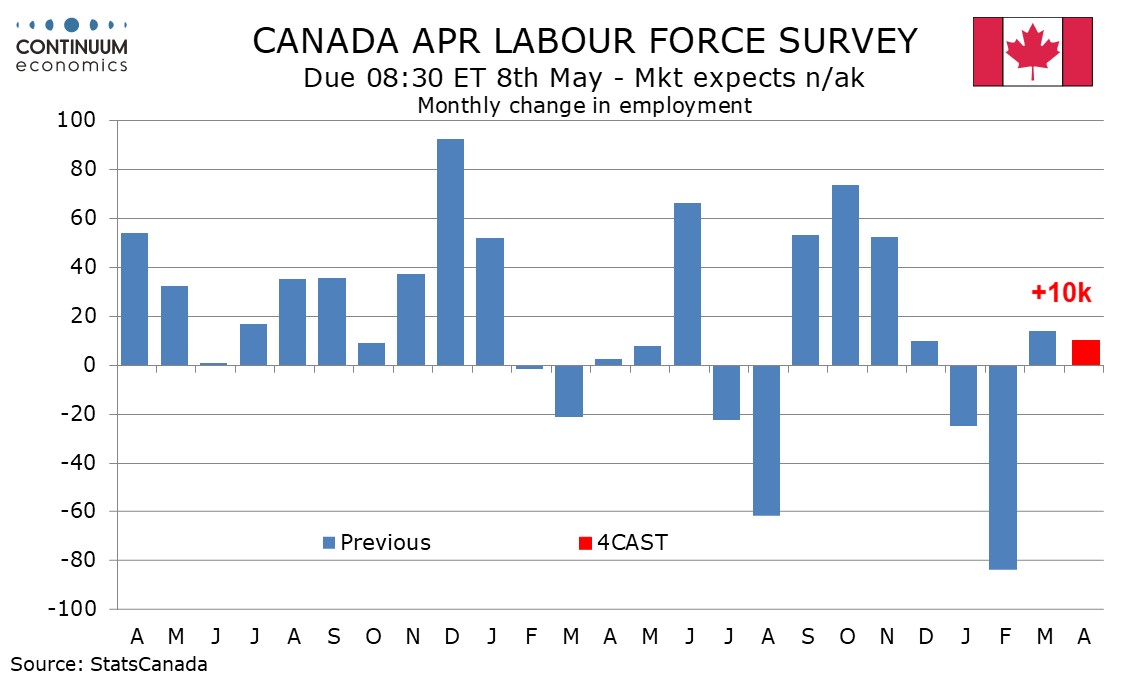

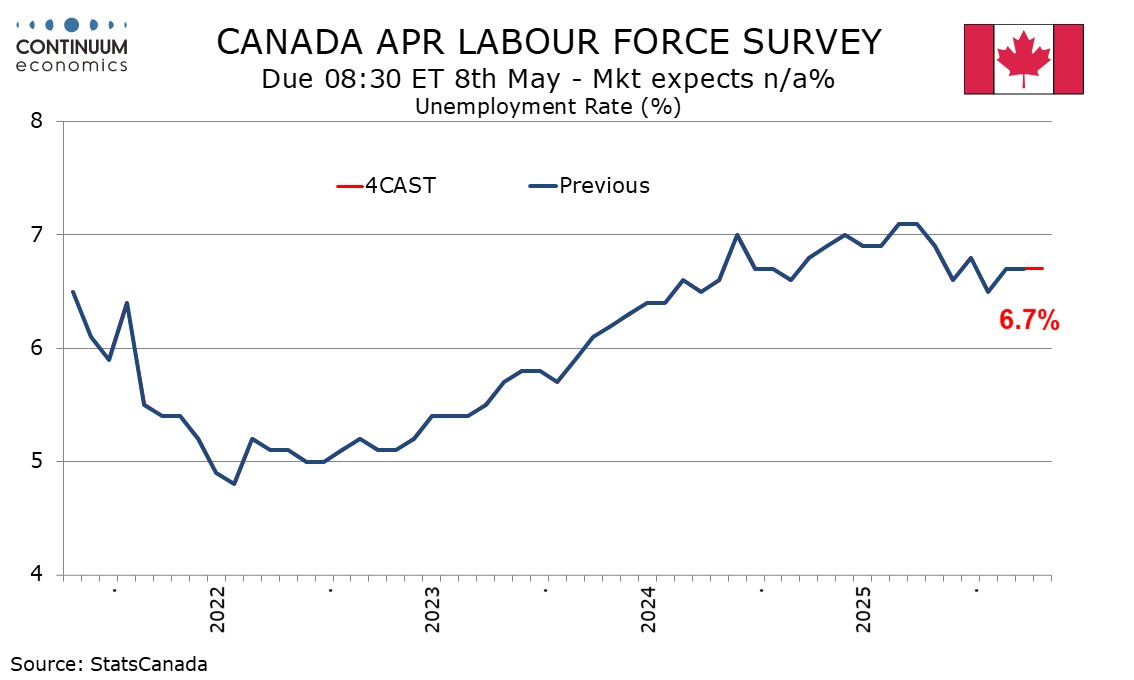

Preview: Due May 8 - Canada April Employment - A modest gain with stable unemployment

We expect Canadian employment to increase by 10k in March, a second straight modest rise to follow a gain of 14.1k in March, still not close to erasing the steep loss of 83.9k in February which extended a substantial 24.8k decline in January. We expect a 6.7% unemployment rate for a third straight month.

This would be consistent with an economy entering Q2 with only modest momentum, growing but struggling to make a significant dent in the output gap. The hit from tariffs is fading while higher energy prices will have a mixed impact on Canadian GDP, but will probably act as a net restraint on job growth. January and February weakness was probably influenced by weather but can also be seen as corrective from overstated gains in September. October and November of 2025, each of which exceeded 50k.

We expect modest April job growth to be evenly split between goods and services, with goods likely to be led by mining, though the lift to oil from higher prices will be modest at this point. March’s service breakdown saw no component with a strong move in either direction, suggesting none is due for a big move in April. We expect the job growth to come fully in full time work, correcting from February and March data when part time employment outperformed.

Trend in the labor force is marginally weaker than that of employment suggesting a slight fall in unemployment, though our call for an unchanged labor force means a marginal fall visible only before rounding, to 6.67% from 6.71%. We see participation at 64.9% for a third straight month. March saw a surprising acceleration in hourly wage growth for permanent employees, to 5.1% yr/yr from 4.2%. A correction is likely, we expect to 4.5%, though March’s bounce was exaggerated by year ago weakness. April 2025 saw no strong rebound, suggesting March’s yr/yr bounce will not see a full reversal.