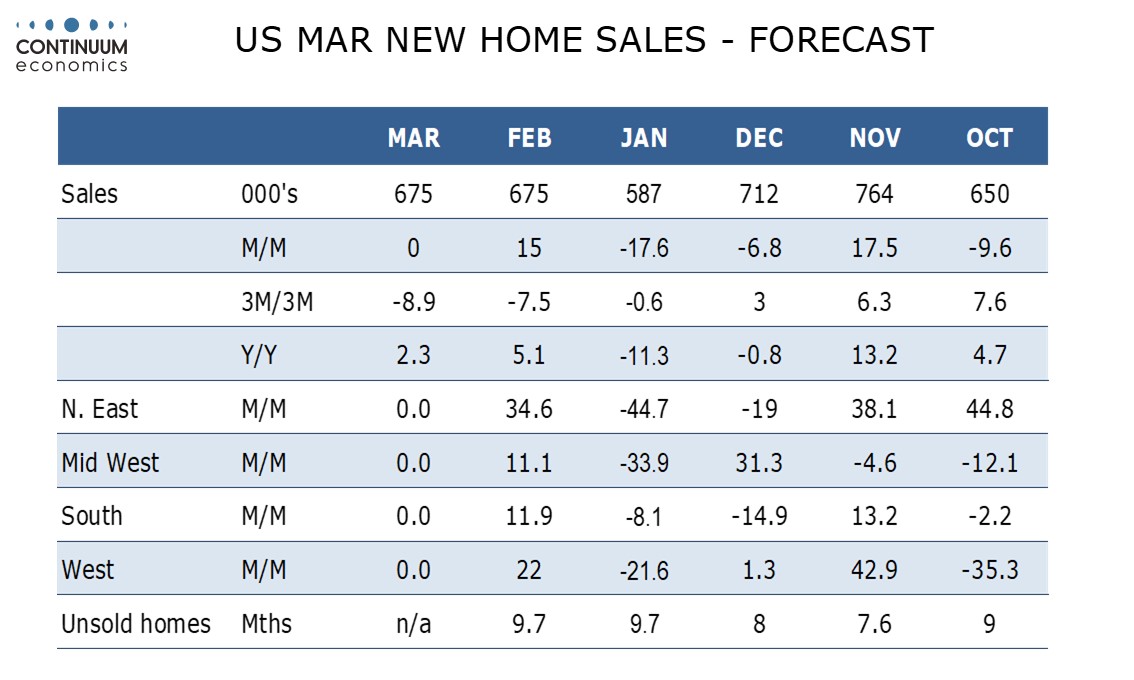

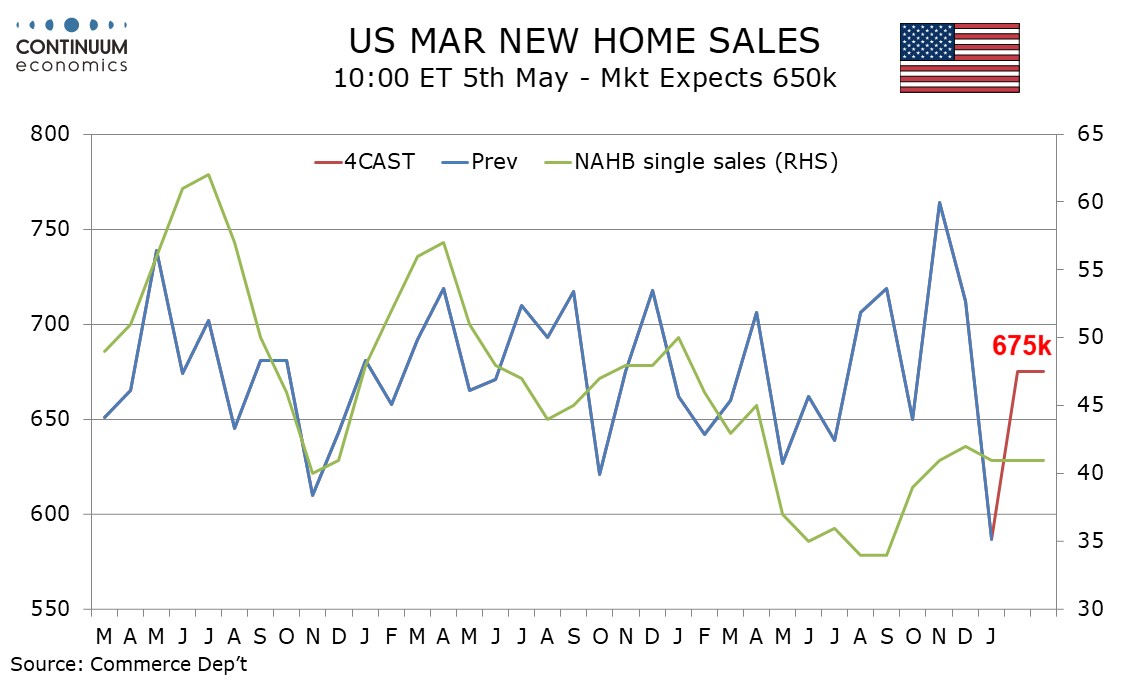

Preview: Due May 5 - U.S. February and March New Home Sales - Trend subdued, but January was below trend

New home sales for both February and March will be released on May 5. We expect a level of 675k in each month, which would be up by 15.0% from January’s 587k, which was the lowest level since October 2022. January’s data was well below recent trend and may have been weather-impacted. We would not be surprised to see January revised higher.

Pending home sales saw gains in both February and March after hitting a record low in January but a modest rise in February existing home sales after a weak January was more than fully erased in March. The NAHB homebuilders’ survey was already off a December high through Q1 and slipped further in April. Overall the housing picture looks quite subdued as hopes for further Fed easing are pushed further into the future but January new home sales appear to have fallen well below trend.

We expect upward corrections in both the median and average prices on the month in February, the median by 1.0% and the average by 2.0%, before unchanged outcomes in March. This would see yr/yr data showing the median at -2.0% in March and -2.6% in February, versus -6.8% in January, and the average showing growth of 0.1% in March and 2.1% in February, up from -3.6% in January that was the first negative since July.