This week's five highlights

Tariff Man In the Spotlight But Inflation may be the biggest worry for the U.S.

The Potential EZ/EU Response for U.S. Tariffs

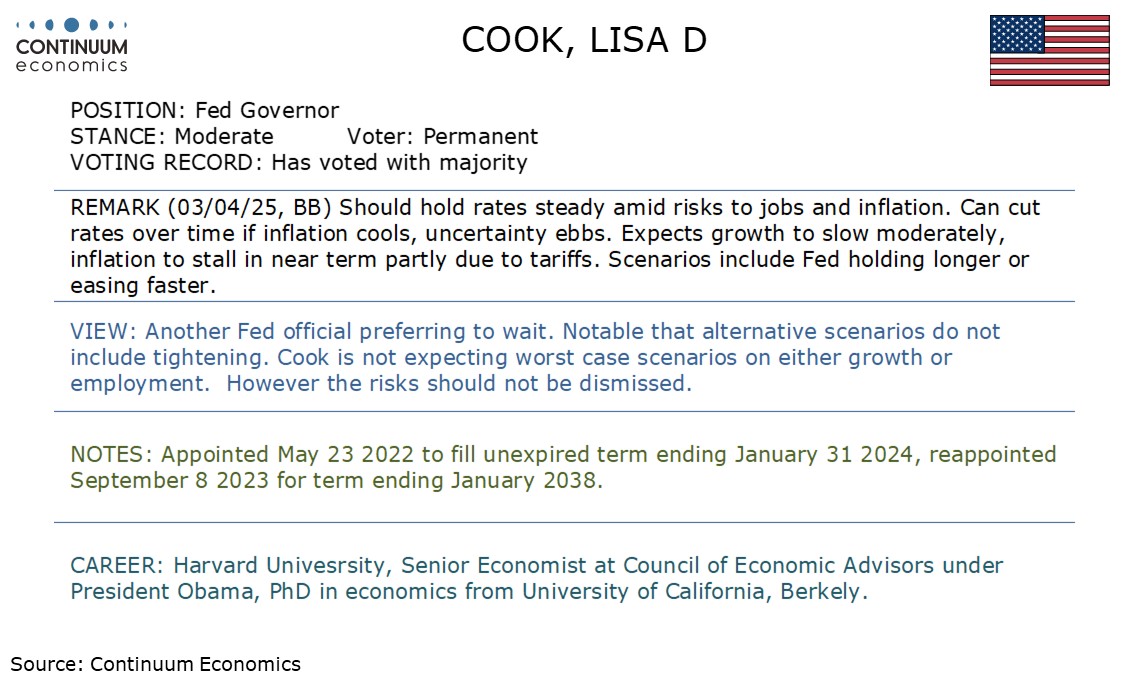

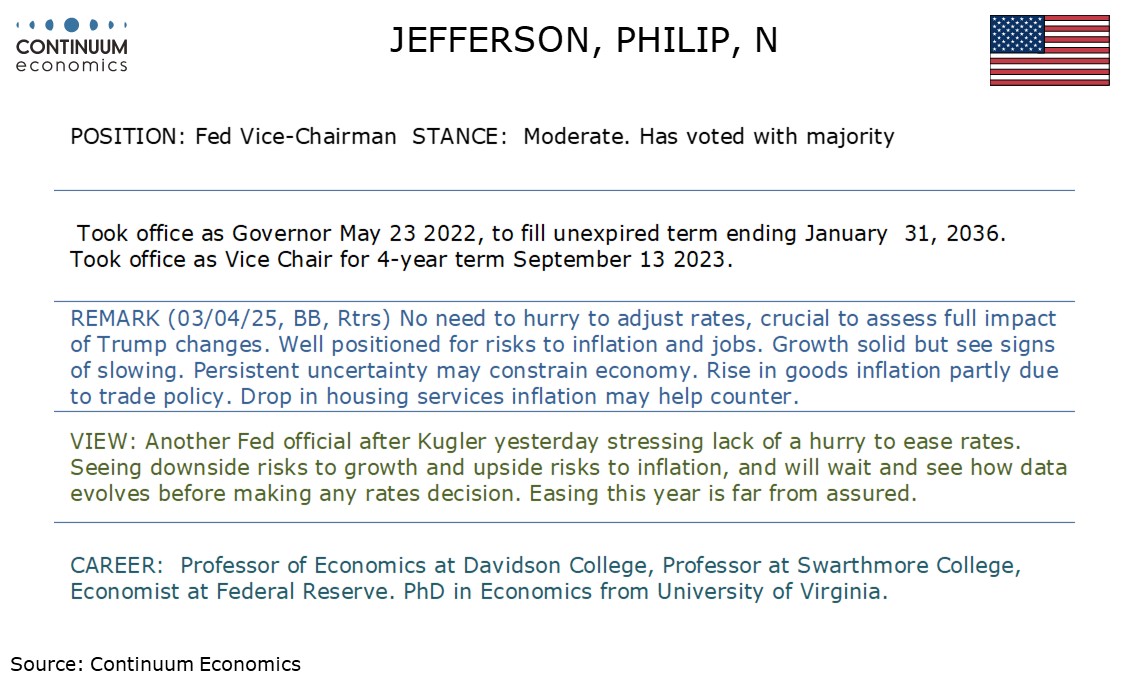

Fed Speakers' Views

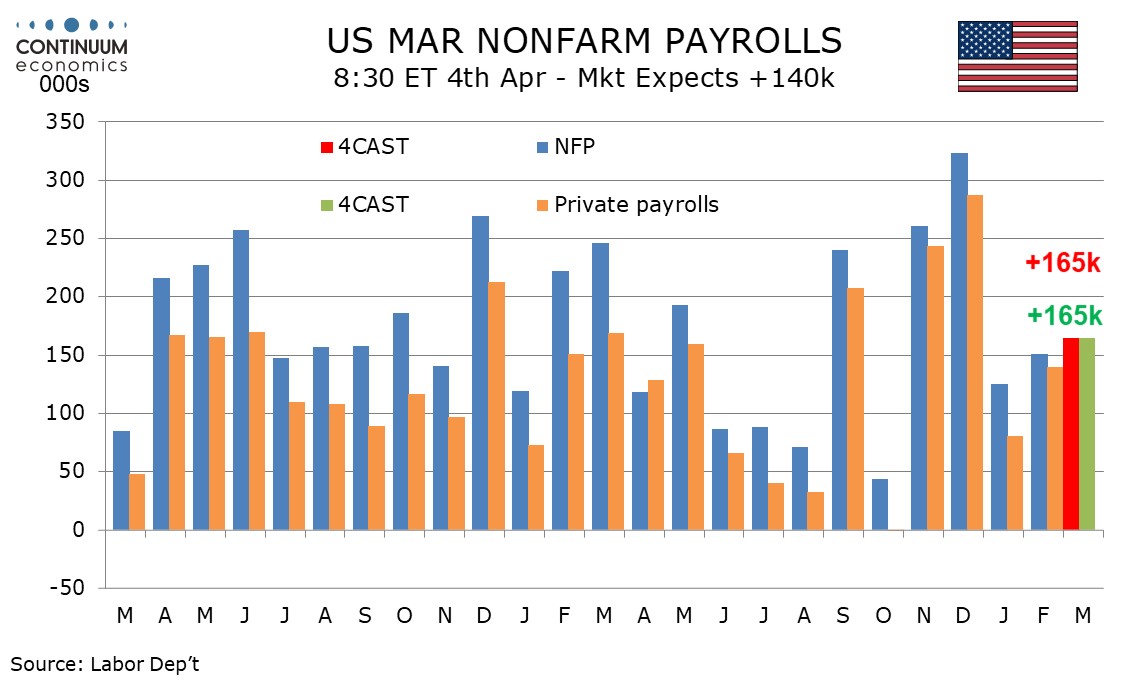

U.S. March Non-Farm Payroll Stronger than January and February

RBA Kept Rates Unchanged

While surprising the market in their intensity, Trump’s “reciprocal” tariffs were in line with previous threats on most countries, and with Canada and Mexico being treated less harshly that feared, the net surprise is modest to us. However we do feel that inflationary risks have increased further, which questions bets on Fed easing. This, and a general impression of unprofessionalism on such a key policy event, justifies equity weakness. Canada and Mexico were hit with 25% tariffs in early March but soon got an exemption for USMCA compliant goods, and that still stands. While tariffs on autos, steel and aluminum, plus those on non-USMCA compliant goods mean Canada and Mexico still face substantial tariffs, they will now face average tariffs below a global average which appears to be above 20%. This is a contrast to the early days of Trump’s term, when Canada and Mexico seemed to be at the top of his hit list, alongside China.

There was no relief for China, with an additional 34% of tariffs imposed, taking the total to an extreme 54%. A 20% tariff on the EU should not come as too much of a surprise given the tone of Trump’s rhetoric, and that the EU gets treated more harshly than the UK, which sees a 10% tariff, is also no surprise. The main offset to the positive surprises regarding Canada and Mexico came in Asia, with tariffs on Japan at 24%, South Korea at 25%, Taiwan at 32% and Vietnam a massive 46%.

Goods imports make up around 12.5% of GDP, so a full pass through of 20% tariffs could add 2.5% to inflation. While the lift may not be as much as that, it could now be significantly above 1%, and we could see some alarming inflation reports in Q2. Auto prices look sure to rise significantly with prices of imported competition and supplies set to rise, and while domestic production could be stimulated, it will take time. Heavy tariffs on Asian counties, notably Vietnam, which has gained business from China, will mean higher prices of items such as t-shirts and toys. The US is ill-equipped to step up production here, industries which are very different from the high-wage traditional sectors such as autos and steel which Trump portrays as the likely main beneficiaries from his tariffs.

We are more inclined to revise up our inflation forecasts than to revise down our growth forecasts, though we do except GDP growth to slow below potential as a consequence of the tariffs. If the economy is not in recession, and inflation, already above target, bounces by over 1%, the Fed is not going to be in a hurry to ease. While Trump was speaking, Fed Governor Adriana Kugler stated that rates should be held as long as upside inflation risks continued, and was blunter than many about the source of those risks, citing government policy changes, if not explicitly tariffs.

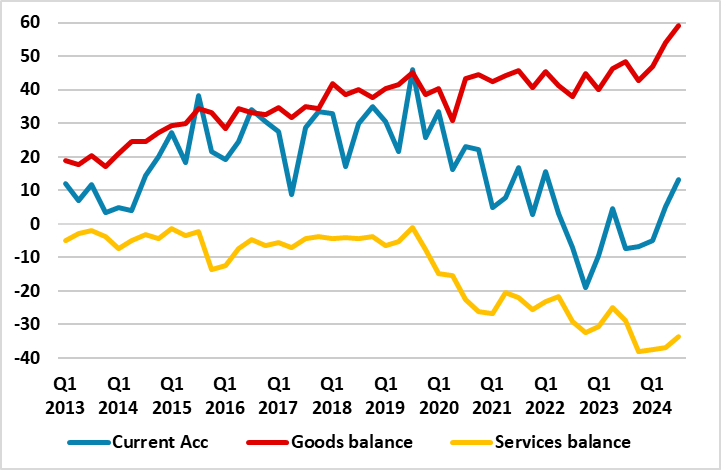

Figure: Bilateral Current Account Gap with U.S. Barely Visible

The U.S is imposing a widespread tariff on the EU of 20%, higher and broader than expected, this based on U.S. calculation of an effective tariff rate of in effect 39 per cent, a figure the EU puts at about 1 per cent. Moreover, rather than including factors such as VAT, and hygiene restrictions on imports, the US tariff estimate seems more indicative of trade in goods imbalances than genuine estimates of barriers to trade, if so, this may be a means through which negotiation can take place and possible with some success. Regardless economic damage is likely to be sizeable, and as far as the EZ is concerned but clear downside to out already anaemic sub-1% GDP estimate for this year, albeit the extent complicated by both how and when the EU will retaliate and global trade diversions, possibly leading to export dumping into the EZ. One worry is that the EU may spread the breath of tariffs via steeper tariffs on digital services, even though the UK has suggested doing the opposite, all threatening a far from concerted response to the U.S. at least from Europe.

In regard to negotiations, the EU has given itself a four-week pause before any retaliation is decided, albeit possible outlining what it is considering beforehand as it hopes to negotiate a solution and/or where the US president could do U-turn before then, as he has before. But a foretaste is already in the offing as the EU is now ready to impose duties on up to EUR 26bn of US goods in response to steel and aluminium tariffs but also has yet to identify how it will retaliate against 25 per cent tariffs on car exports announced last week.

We expect a 165k increase in March’s non-farm payroll, both overall and in the private sector, to show the labor market remains healthy despite growing downside economic risks. We expect the unemployment rate to slip to 4.0% from 4.1%, and an in line with trend 0.3% increase in average hourly earnings. A 165k increase would be stronger than February’s 151k and January’s 125k, both of which were probably restrained by unusually cold weather. Weather was mostly mild in March though storms in the South provide some downside risk. While survey evidence is showing signs of weakness hard data generally remains solid, particularly weekly initial claims.

Leisure and hospitality is a sector to watch for a bounce after two straight declines that may have been weather-influenced, though there is also a risk that the sector is being hit by reduced tourism, particularly from Canadians who have been refusing to holiday in the US due to the trade dispute. We expect 30k in layoffs of Federal government workers, up from 10k in February, but this is likely to be offset by continued hiring and the state and local level. A flat total from government would be the weakest month since a decline seen in May 2024, a fall that corrected two particularly strong months. A fall in unemployment to 4.0% from 4.1% would reverse an increase seen in February. The household survey, which calculates the unemployment rate, showed employment and the labor force falling, and a correction higher in both is likely. However reduced immigration may see the labor force seeing the smaller gain.

The RBA has kept the cash rate unchanged at 4.1% in the Apr 1 meeting as they see upside risk to inflation after headline moderates below 2.5% y/y. They acknowledge progress in moderation of CPI but are looking for it in a sustainable manner. Their forward guidance did not change by indicating data dependency approach. Our view has not changed and see two cuts in 2025 to 3.6% and 3% in 2026. The timing of the first cut could be as early as June if CPI further moderates. With their data dependency approach and favors inflation sustainably in mid range, it seems to suggest they are looking for the trimmed mean CPI to reach 2.5% before their next cut.

While it looks like baby steps, the RBA is optimistic about the recovery in domestic demand, along with higher real wage. The latest weakness in headline employment data has also been watered down but they are still seeing slower growth in wages. The economic outlook, both domestically and globally, remains uncertain. Sluggish consumption growth and worse deterioration of labor market are cited to be critical factors for deviation in domestic outlook forecast. Obviously, Trump's tariff policies and geopolitical tension are not missed out in RBA's mind.