This week's five highlights

FOMC leaves rates unchanged

A Placeholder Meeting for BoJ

BoE Being Careful Amid Data Conflicts

Everything Unchanged for Riksbank

SNB 25 bp Cut Likely To Last

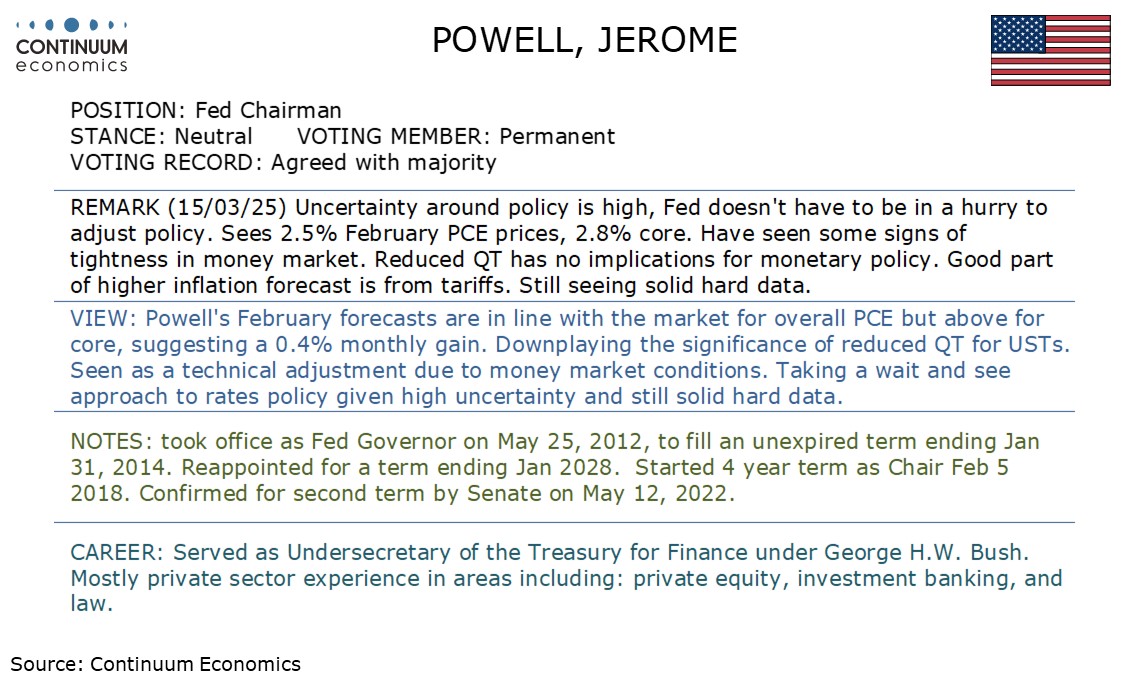

The FOMC has left rates unchanged at 4.25-4.5% as expected. The median dots are unchanged but economic activity forecasts are weaker and the inflation forecast for 2025 is significantly stronger showing concern over the impact of tariffs. The statement notes increased uncertainty and announced a slowing of the pace of Quantitative Tightening in April. The Median dots still look for 50bps of easing in 2025, 50bps in 2026 and 25bps in 2027, taking the 2027 Fed Funds target to 3.125%, slightly above an unrevised 3.0% long run-neutral estimate. However the skew is now upwards, with the 2025 dots showing eight respondents above the median and only two below, contrasting December when five were below the median and four above.

This reflects increased worries over inflation, with 2025 core PCE prices seen at 2.8% rather than 2.5% though 2026 is still seen at 2.2% and 2027 on target at 2.0%, showing the tariff boost to inflation is seen as a one-time lift. 2025 GDP has been revised lower to 1.7% from 2.1% and 2026 and 2027 have been revised lower too, suggesting tariffs could cause a more sustained damage to growth prospects. The statement has left the assessment of the economy unchanged from December but instead of stating that risks are balanced now states that uncertainty has increased. Quantitative Tightening is to be scaled back, as was hinted at in January minutes which noted debt ceiling concerns. Beginning in April the monthly redemption cap for USTs will fall quite sharply to $5bn from $25bn, though the cap on agency debt and mortgage-backed securities will remain at $35bn. That only USTs has seen a change in the QT plans is a sign that debt ceiling concerns are playing a key role in the decision. Fed Governor Waller dissented from the decision to slow the pace of QT but backed the unchanged rates decision.

The BoJ has kept rates unchanged at 0.5% in the March meeting with little forward guidance. While the January and February inflation remains strong, the BoJ is likely waiting for the result of spring wage negotiation and Trump's tariff policy before the next step. Early results are seeing a solid wage growth (more than 5%) for large enterprises but SMEs are likely finding it difficult to catch up the pace given their slower adoption of changes in the price/wage setting and could be a drag for the BoJ's next step. The soft private consumption is likely to be be their mind as the current constitution of inflation is still largely cost based.

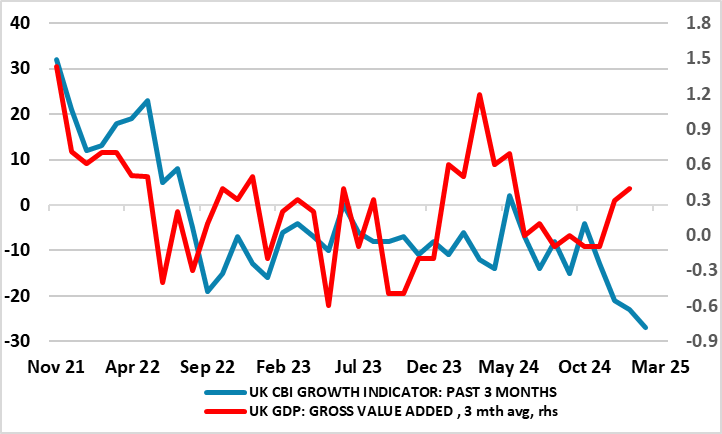

Figure: Surveys Pointing South

Even amid a BoE rate cut last month that was delivered with a clear(er) degree of action, all MPC members opting for easier policy. Even so, it was clear there were still MPC divisions that probably reflected increased uncertainty enough for the BoE to have altered its rhetoric somewhat to stress the need for policy to be framed carefully as well as gradually, wording reused this time around. Indeed, this shift very much pointed to what has turned out to be stable policy (Bank Rate still at 4.5%) at this March meeting, with it increasingly likely that the MPC majority envisages rate cuts no faster than every quarter this year and a little further into 2026 but with no pre-set path being considered – at least openly. The BoE still believes that policy needs to remain restrictive, with the appropriate degree of restrictiveness to be decided at each meeting.

Given what we think is a flailing real economy backdrop, which growing global trade tensions may only accentuate, BoE easing may yet come faster and further as the BoE reassess its optimism about growth and upgrades its estimate extent of slack – particularly in the labor market (Figure 1). Indeed, the likelihood is that additional fiscal and trade details due by the May MPC meeting, alongside the already frail real economy backdrop, may persuade the BoE into a further growth downgrade. Thus we see at least three more moves this year and probably four.

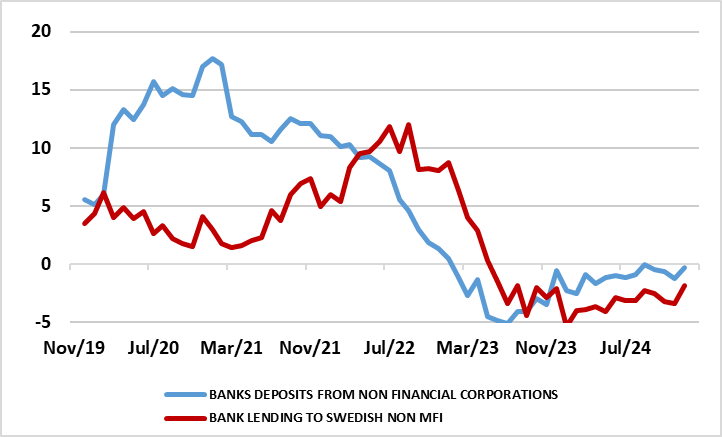

Figure: Bank Lending and Deposit Growth Still Negative – Even Nominally

Having delivered in January, the widely-expected sixth successive rate cut, the Riksbank adhered to the assessment made in December that the easing cycle has drawn to an end with the policy rate (down to 2.25%) having dropped 1.75 ppt in eight months. Especially given the recent upside CPI surprises, this very much pointed to no move at today’s (March 20) decision and with a stable policy outlook likely to be reinforced by updated projections that may continue to point to above-consensus growth this year and next. This is what occurred, again surprising few, if any. Perhaps as notable was that little otherwise changed with largely stable projections for growth, output gap and even inflation, save on the latter for a spike higher now factored into this year but with a return to target from early 2026.

But even with the fiscal situation likely to become somewhat easier into 2026, we continue to think that amid global uncertainties, and given still negative monetary dynamics (Figure 1), the Riksbank will have to make a downgrade to its real activity outlook. This is largely unchanged from the December Monetary Policy Outlook and still points to 2%-plus GDP growth for the next three years annually. We think that this above-consensus picture is too optimistic and it is noteworthy that the Riksbank has accepted a weaker consumer outlook but where the impact on GDP has been offset by a fall in import growth. Indeed, to us that 2025 outlook also comes with downside risks which encompass a consumer recovery that may be much more feeble reflecting labor market uncertainty and what may be a sustained rise in household savings. The consumer picture is made more uncertain as an unfolding sharp rise in unemployment should mean that wage growth this and next year may fall from last year’s 3.8%.

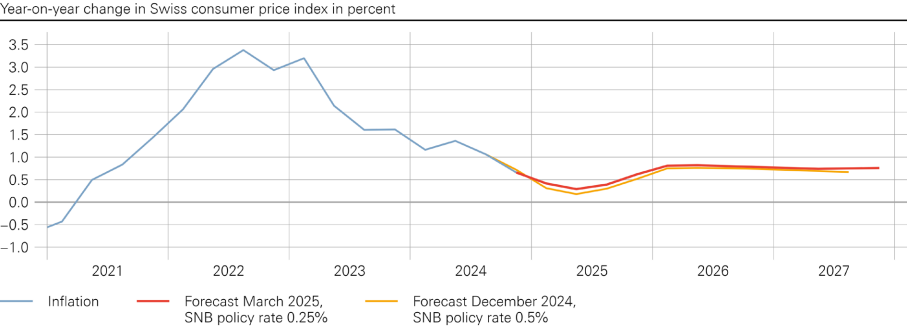

Figure: SNB CPI Inflation Projections

Bottom Line: With inflation forecasts stable, and given a reasonable economic outlook, it would be a good time to pause or stop the SNB easing cycle. However, if the U.S. trade tariffs have a bigger adverse effect than expected or the CHF surges, then the SNB may want the option to ease again later in the year. Thus SNB communications will likely leave the door open to further easing, but in reality we see this as probably the end to the easing cycle.

The SNB cut the policy rate by 25 bp to 0.25% as widely expected. In the policy assessment, the forecasts for inflation hardly changed, in contrast to the downward revisions in previous quarters. Additionally, the SNB noted that the forecast (i.e. for CPI) is within the range of price stability (the SNB inflation target is purely for the rate to be below 2%) over the entire forecast horizon - no hurry then for more easing but not ruling them out!

On the real sector side, the SNB sticks with 1.0-1.5% for 2025 and is now forecasting 1.5% for 2026. Though U.S. tariffs could have an adverse effect on Switzerland, the SNB note that increased defence spending in Europe could provide a medium to long-term boost. Domestically the lagged effect of monetary easing, plus positive real wage growth should support domestic demand. Though the SNB notes higher uncertainty over the global growth picture, it’s baseline of reasonable growth has some supportive arguments.

This leaves the SNB with a dilemma going forward. With inflation forecasts stable, and given the economic outlook, it would be a good time to pause or stop the easing cycle. However, if the U.S. trade tariffs have a bigger adverse effect than expected, then the SNB may want the option to ease again later in the year. Additionally, the SNB will leave open the option of cutting to negative rates, just in case the Swiss Franc surges. The option of negative rates in itself meanwhile acts as a restraint from the FX market getting too bullish on the CHF. Thus SNB communications will likely leave the door open to further easing, but in reality we see this as probably the end to the easing cycle.