Brazil: Cautious 25bps Cut

BCB gave no detailed forward guidance, but they did hint at flexibility and did not lock themselves into only 25bps steps in future meetings. We do feel that policy is very tight and that a further cut will be evident at April 29 meeting. This could be either 25bps or 50bps depending on the length of the Iran war, but for now we would pencil in a 25bps cut. However, our baseline remains for a 4-6 week Iran war and that should mean that BCB is more confident by June and we pencil in a 50bps cut. We look for a further 150bps in H2 down to 12.50%

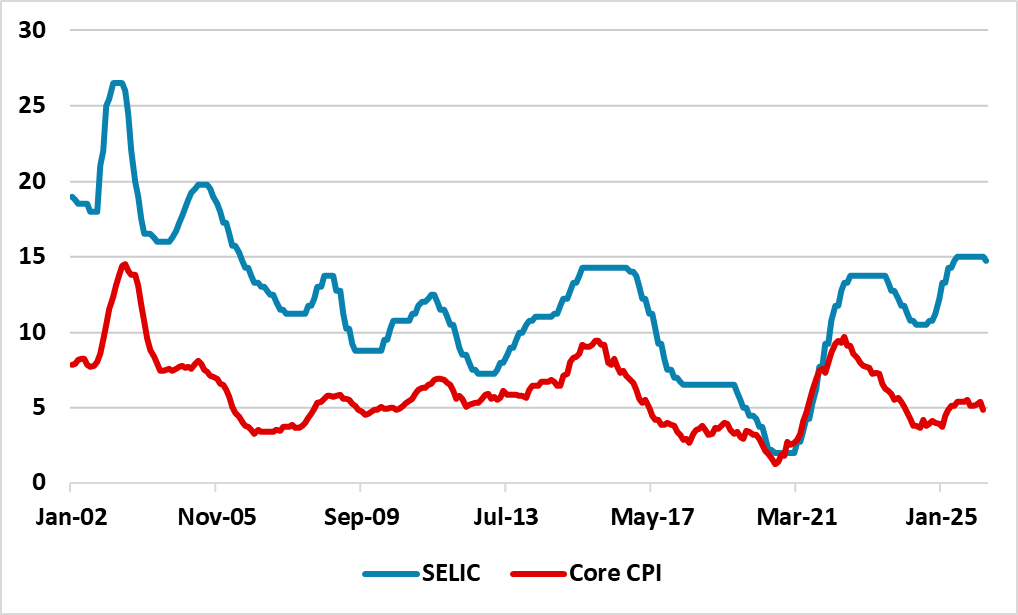

Figure 1: Brazil Core CPI and SELIC Policy Rate (%)

Source: Datastream/Continuum Economics

Key points from the March BCB meeting include

• 25bps cut and No forward guidance. The BCB decided on a cautious 1st step to the anticipated easing cycle with a 25bps cut in the SELIC to 14.75%. This contrasts with widespread expectations in February of a 50bps cut before the Iran war, as inflation had shown a softer trend and GDP had remained weak due to the lagged effects of super restrictive policy. BCB know that the super high level of real policy rates will squeeze the economy and needed to start the easing cycle, but the uncertainty over the duration of the Iran war and high energy prices means it has to be a cautious start.

• Cloudy forward guidance. BCB gave no detailed forward guidance, as they indicated that they want to assess the situation in the coming months. Nevertheless, they did hint at flexibility and did not lock themselves into only 25bps steps in future meetings. This could mean that a 50bps step is seen in the future if the Iran war ends and energy prices start to come back down. This would then allow BCB to look through the 1st round effects and place emphasis on the big picture trajectory. We do feel that policy is very tight and that a further cut will be evident at April 29 meeting. This could be either 25bps or 50bps depending on the length of the Iran war, but for now we would pencil in a 25bps cut. However, our baseline remains for a 4-6 week Iran war and that should mean that BCB is more confident by June and we pencil in a 50bps cut. H2 should see a further 150bps to take the SELIC down to 12.50%, which is 50bps higher than we previous thought. In 2027 the BCB easing is likely to be moderate rather than aggressive and will be data dependent and we see a further 300bps to 9.5%. This would still be mildly restrictive policy rate level, with the market viewing 8% as being around nominal neutral policy rates, with the BCB having estimated a 5% neutral real policy rate in the past (here).