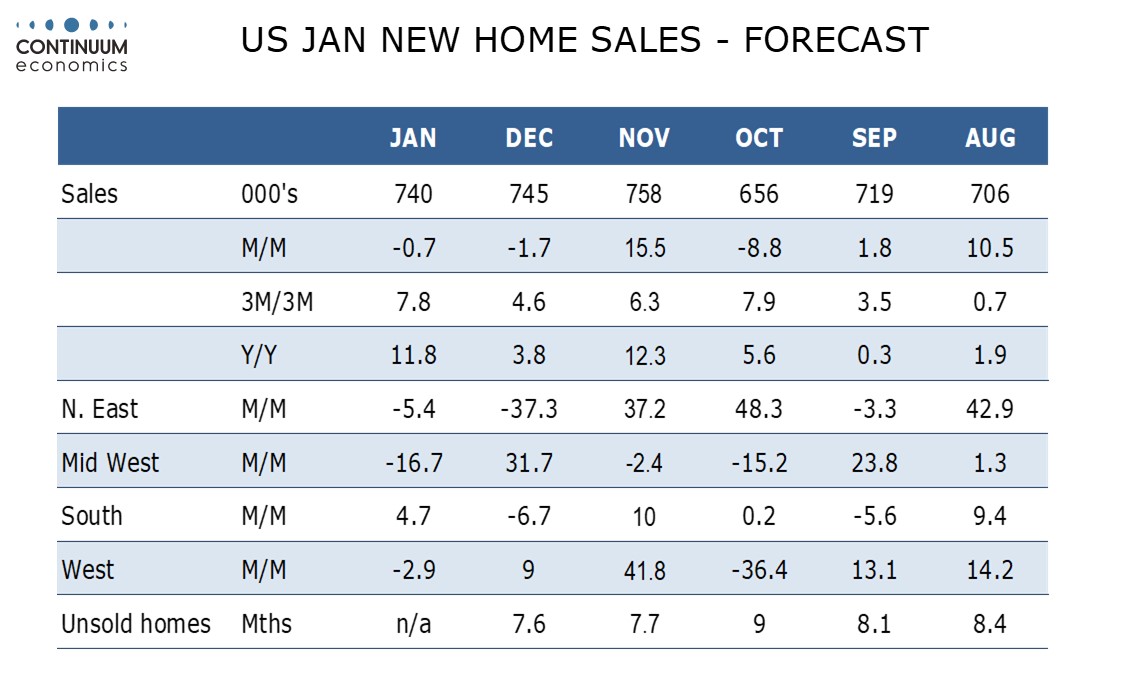

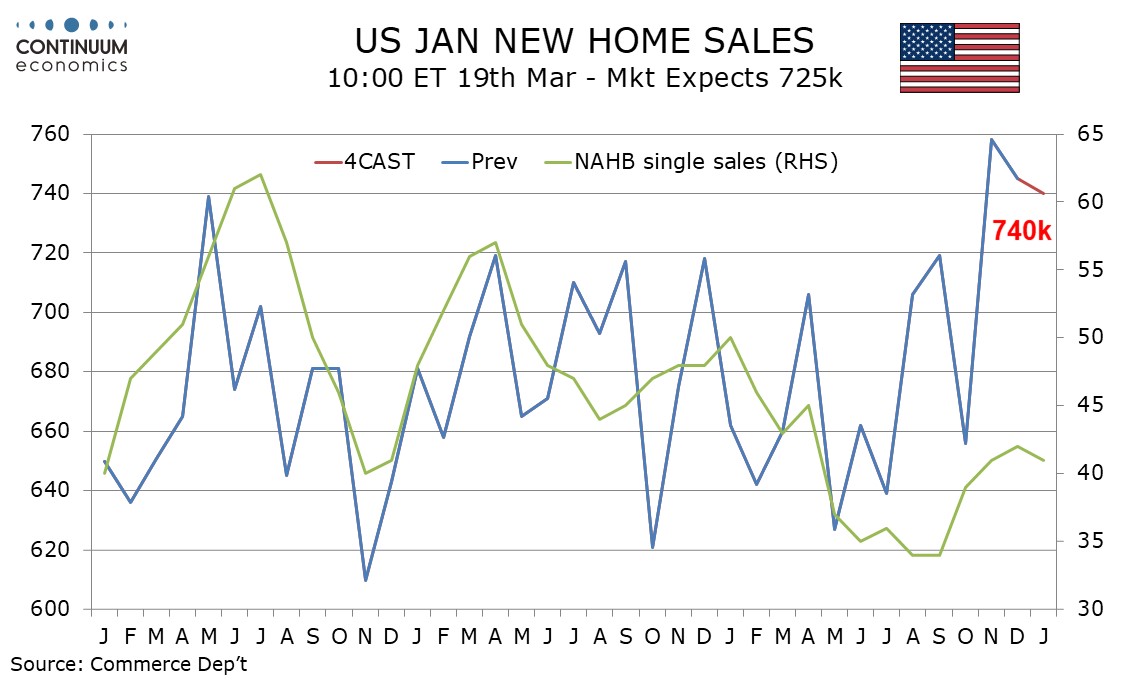

Preview: Due March 19 - U.S. January New Home Sales - Edging further off November's high

We expect a modest 0.7% decline in January new home sales to 740k, a second straight loss after a 1.7% decline in December. This would still leave most of November’s 15.5% increase, which took sales to their highest level since February 2022, intact.

Survey evidence is mixed with the NAHB homebuilders’ index edging lower in January though the MBA house purchase index held up in January before slipping in February. Pending home sales, designed to predict existing home sales, extended a sharp December decline in January. Existing home sales slipped in January, but corrected higher in February. On balance there are signs of a modest loss of momentum in housing demand after a recent boost assisted by the resumption of Fed easing.

Weather may be a factor restraining sales in late January. We expect sales to fall in three of the four regions, the exception being the South. We expect both the median and average price to correct lower in the month from December gains, by 1.0%. This would see yr/yr growth increasingly negative, at -4.5% from -2.0%, for the median, and less positive, at 1.8% from 4.7%, for the average.