Published: 2025-03-17T19:25:24.000Z

Preview: Due March 27 - U.S. Final (Third) Estimate Q4 GDP - No revision overall, but consumer spending may look slower

7

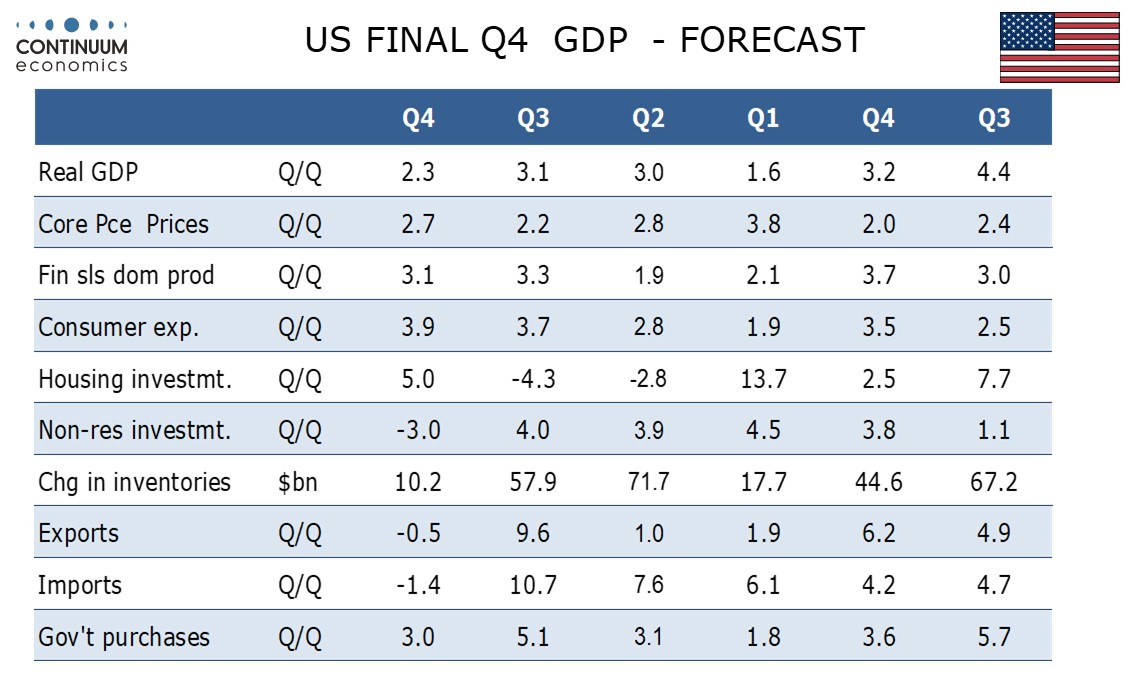

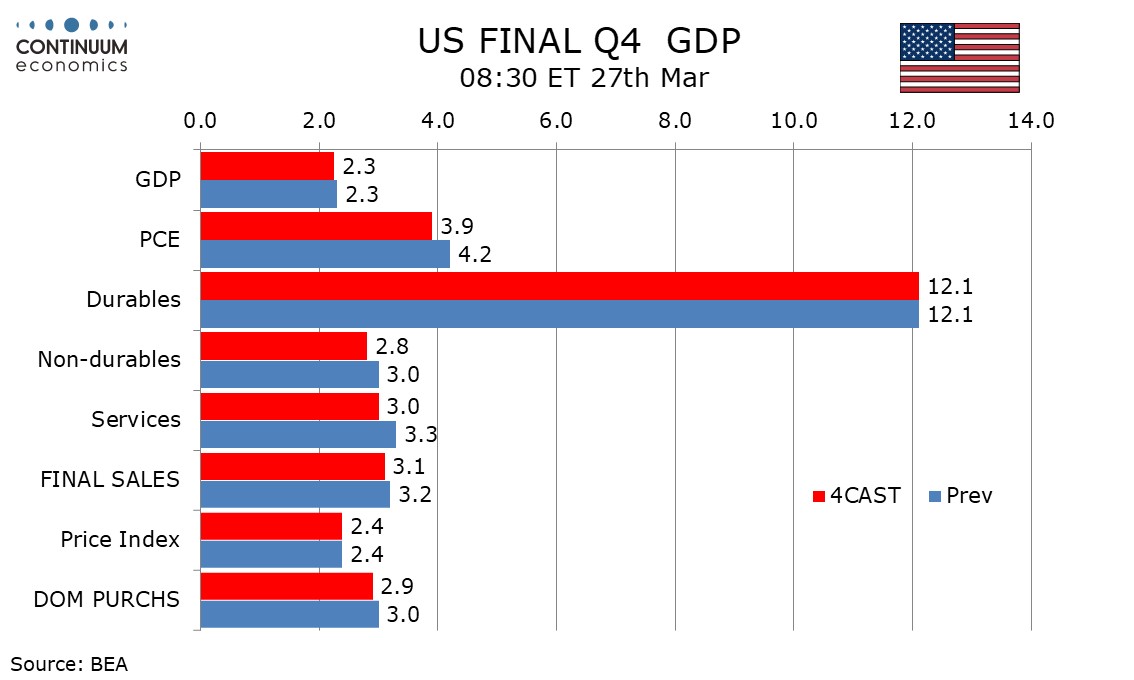

We expect the final (third) estimate of Q4 GDP to be unrevised from the preliminary (second) estimate of 2.3%, though in USD terms the revisions will be marginally negative.

The main negative we expect is a downward revision to service consumption to 3.0% from 3.3% reducing consumer spending to 3.9% from 4.2%.

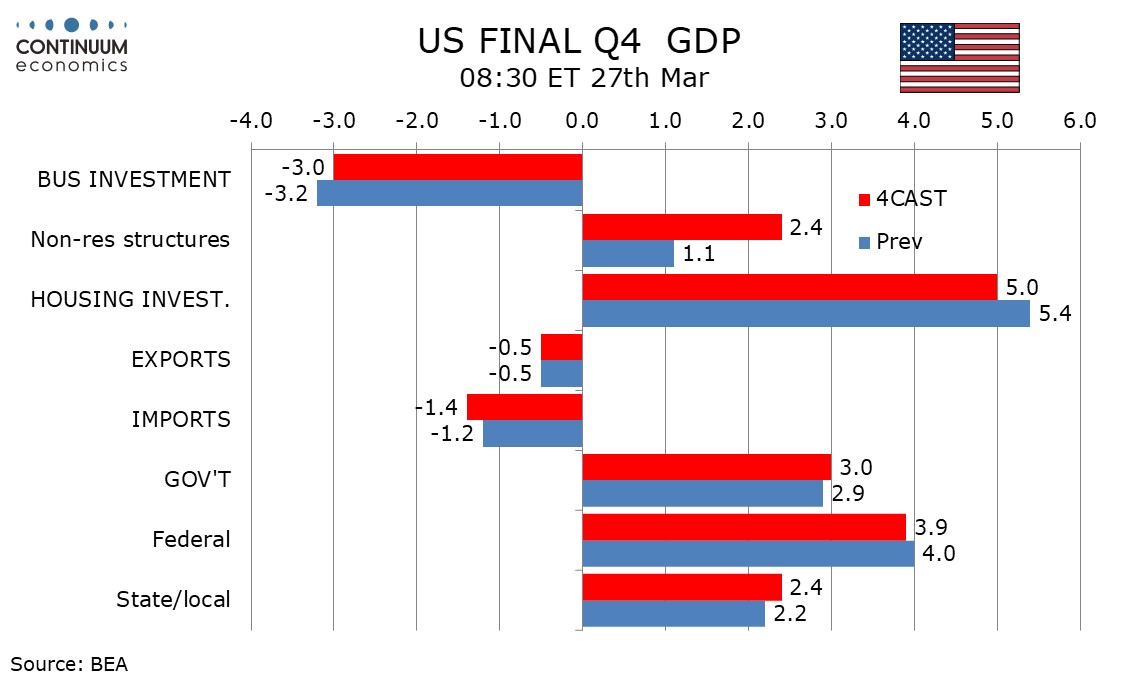

Partial offsets to this will come from construction (with upward revisions to private non-residential and public outweighing a downward revision to housing) and a downward revision to service imports lifting net exports.

We do not expect any revisions to the price indices, of 2.4% for GDP, 2.4% for PCE prices and 2.7% for the core PCE price index.