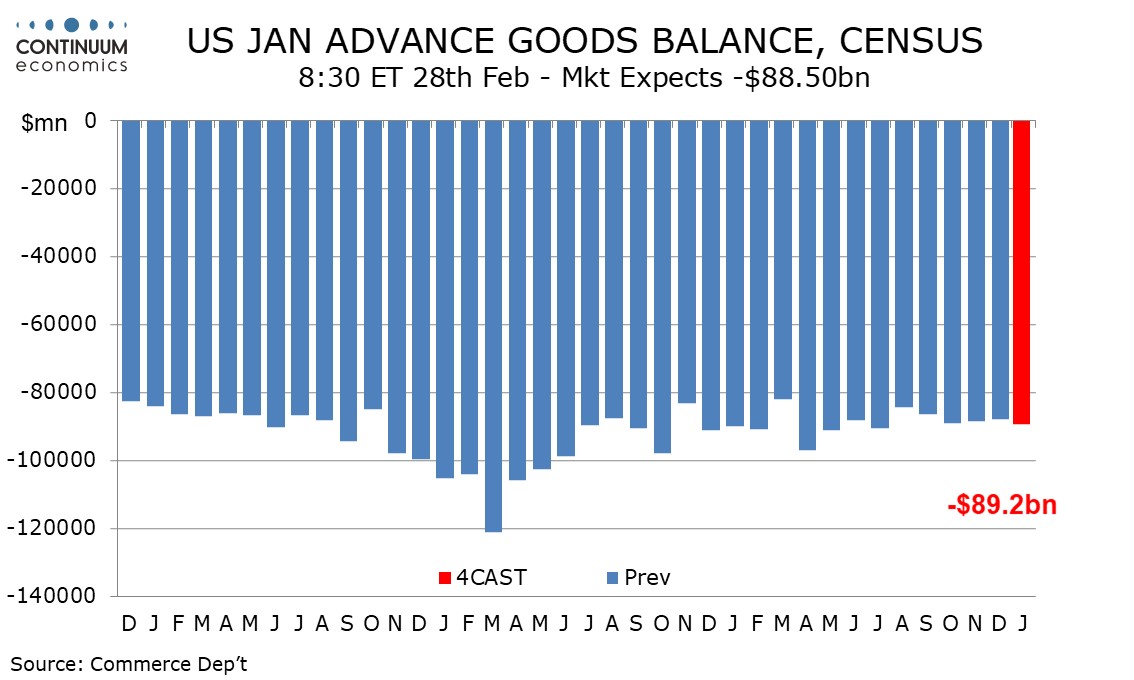

Preview: Due February 28 - U.S. January Advance Goods Trade Balance - Deficit to correct higher, trend neutral

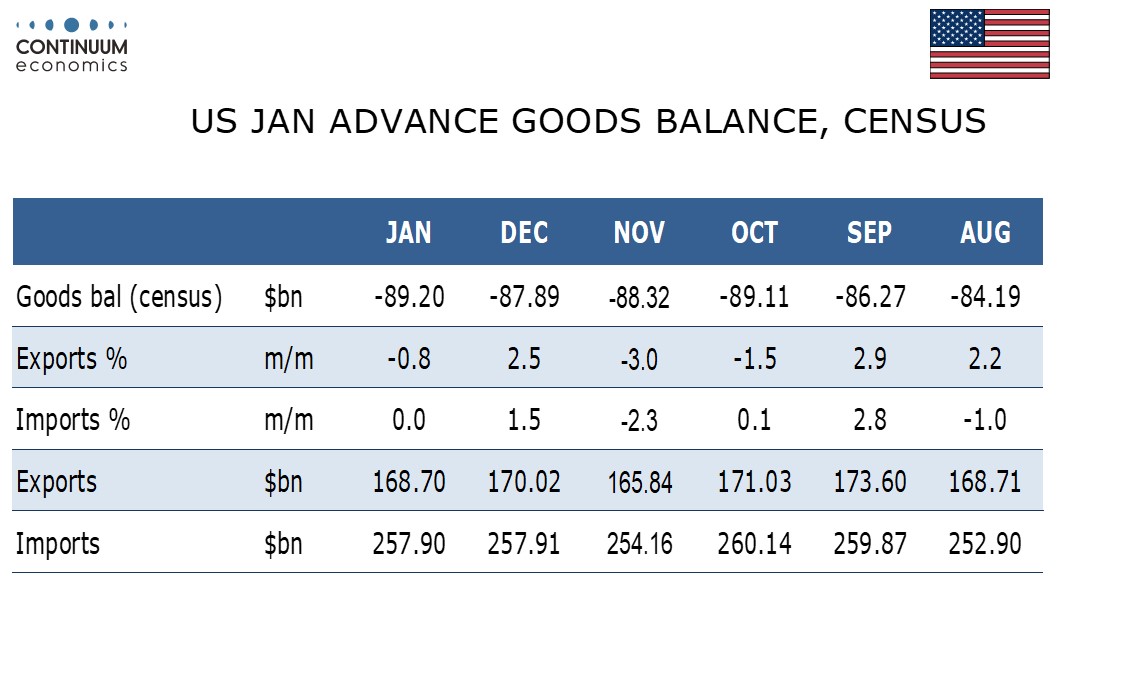

We expect January’s advance trade deficit to increase to $89.2bn from $87.9bn, a correction from two straight narrowings and the widest deficit since July, though trend will continue to lack a clear direction.

We expect exports to fall by 0.8% and imports to be unchanged. Export and import prices both rose by 0.8% in January so that implies declines in volumes in both series, though more sharply for exports.

Both series will be showing volumes correcting from increases in December, where exports showed the larger gain and may have more scope to correct. That manufacturing output slipped in January, partly on weather, and that Boeing exports fell, both imply downside risks to January exports. Durable goods orders data was consistent with that.